Intel (INTC) shares are close to hitting another multi-year low this week as U.S. equity markets inch closer to a technical bear market. While shares have traded lower towards the low $40s, I am neutral on the stock.

Invest with Confidence:

- Follow TipRanks' Top Wall Street Analysts to uncover their success rate and average return.

- Join thousands of data-driven investors – Build your Smart Portfolio for personalized insights.

Intel’s Q1 results weren’t bad with small beats on earnings and revenue, however investors were disappointed to hear weaker guidance for Q2. Additionally, this week, China reported a sharp decline in retail sales and industrial output as the CCP refuses to deviate from its zero-COVID policy. China accounts for over 25% of Intel’s total revenue, which could lead to further downward revisions in the coming quarters.

In recent years, Intel has struggled to compete effectively with top semiconductor players. TSMC (TSM) in particular has outperformed Intel, as the company faced delayed product releases and slow chip development.

Management is now guiding large CapEx spending in the years ahead to build out product development efforts, and expand manufacturing across the globe. Wall Street is guiding for $2.5 billion in free cash flow in FY22, and $4.3 billion in FY23. Management is actually guiding negative free cash flow in FY22 between $1 billion and $2 billion.

This decrease in free cash flow is a result of large CapEx spending in the years ahead. Management expects CapEx to be around 35% of revenue over the coming years, with a target of lowering that figure to around 25% in the long term.

Intel also has a target of reaching 20% FCF margin by 2026, which should yield FCF of $19 billion from 2026 onwards. Luckily, Intel has the financial resources available to attempt a turnaround. While Intel has long-term debt of $37.24 billion, it has enough cash ($38.7 billion) and operating income to maintain a dividend while also running an historically large CapEx budget.

Insiders appear to be convinced of Intel’s plan as they have purchased roughly $6 million worth of shares in the past year. In May alone, CEO Patrick Gelsinger and new CFO David Zinsner purchased over $500,000 worth of Intel stock.

Investing for a Turnaround

Increased CapEx spending is what investors want to see, however other semiconductor manufacturers are also adding to their CapEx budgets in the years ahead. TSMC is guiding a CapEx budget of $40 billion to $44 billion. This is a massive increase from its $30 billion CapEx spend in 2021.

By the time Intel catches up, they (Intel’s competitors) will also have made process development leaps. While the market for semiconductors is tight with higher margins and large backlogs, Intel is at risk of overspending if it does not meet its goals.

Management claims Intel will surpass the manufacturing capabilities of TSMC by 2025. However, Intel has disappointed previously with product releases and manufacturing delays. Therefore Intel has an uphill battle to restore credibility with investors.

It’s likely a turnaround to some degree will be occur, however investors need to determine if they’re willing to wait several years for a turnaround just for their average return to be similar to that of an index.

Management has 24 concurrent construction projects across the globe and an ambitious target of developing five nodes over four years. Under previous management, significantly less ambitious targets were missed at a time when Intel was loosing market share.

However, I would argue today Intel has better equipment and partnerships to support its goals, particularly its continued partnership with ASML. Intel ordered its first TWINSCAN EXE:5200 EUV (lithography machine) from ASML in January, which will have a 200 wafer per hour capacity.

Across its segments, Intel expects total revenue to grow in the mid-high single digits over the next few years followed by double digit growth from 2025 onwards.

At Intel’s investor meeting in February, Zinsner outlined his expectations for margin growth over the coming years. He guided gross margins to grow from 51%-53% in FY22-24 to 54%-58% from FY25 onwards.

Valuation

Intel has is valued at $177.6 billion. NTM EV/EBITDA is guided to be 6x, suggesting investor sentiment has diminished. While this seems like a cheap valuation, Intel’s free cash flow is expected to vanish for several years.

From a cyclical perspective, semiconductor delivery times are still high and it’s expected that semiconductor manufacturers will see decent margins over the next few quarters as we are still mid-cycle.

An increasingly hawkish Fed is the main short-term risk to Intel, as the Fed might abandon any expectation of a soft landing as it raises rates. If this happens demand for chips will slowly contract leaving Intel to delay it’s free cashflow targets.

At the current valuation, Intel yields a dividend of 3.3%, which is likely to be a supporting factor preventing from Intel from a complete valuation collapse if the current equity market sell-off accelerates.

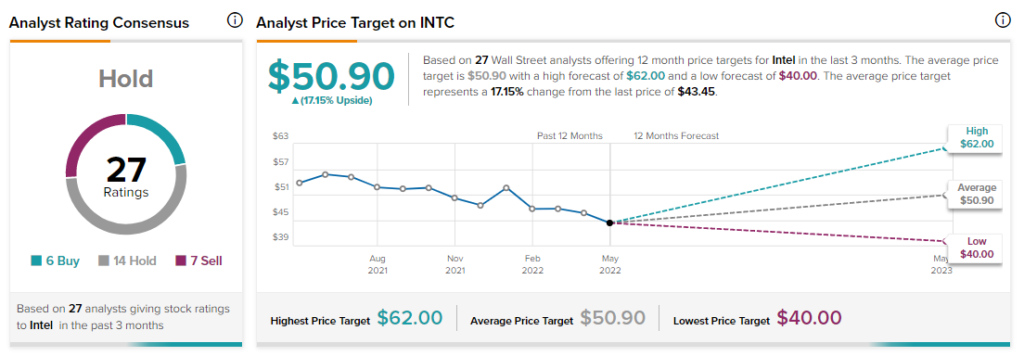

Intel has received six Buy ratings, 14 Hold ratings, and seven Sell ratings over the past three months. The average Intel price target of $50.90 suggests 17.2% upside potential.

Conclusion

I believe Intel will continue to see a slow sell-off. followed by sideways consolidation over the coming years while investors wait on key milestones.

Discover new investment ideas with data you can trust.

Read full Disclaimer & Disclosure