For investors seeking a sign, some clear signal that indicates a stock to buy, there’s nothing better than a confluence of multiple factors. One piece of data may be suggestive; two may indicate something good; but when as many as three data points come together, investors should take notice.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

We’ll look at two stocks that, according to the TipRanks database, are showing just that combination of strong indicators. First, each of these is trading at a discounted price. They peaked last year, and have fallen sharply since – but a low price doesn’t necessarily mean fundamental unsoundness.

Second, these stocks have both gotten plenty of love from the Wall Street analysts. Each has a ‘Strong Buy’ consensus rating – and a potential upside, based on analyst price targets, of more than 200%.

And finally, well-placed insiders have been buying up these shares in large amounts. The insiders are corporate officers, in positions of both knowledge and responsibility, and answerable to Boards and shareholders. They don’t trade their own company’s shares lightly, so investors should pay attention when they make informative buys.

We’ll take a look ‘under the hood’ of these two stocks, to find out just why their combination of positive indicators may make them compelling purchase ideas. Here are the details.

Inotiv (NOTV)

We’ll start with a company in the biomedical field – but one with a difference. Where most biomed firms tend to work in drug research, Inotiv takes a different tack in this field. The company is a leading provider of drug discovery and development services, along with analytical instruments critical to the drug development and research efforts of the biotech and pharmaceutical industries. In short, Inotiv in an outsource company, speeding up its customers’ capabilities in scientific research and analytics.

Inotiv has been hit hard by the market’s downturn in recent weeks. The stock was riding high as late as this past November, when it peaked above $57; since then, the shares are down ~60%.

Even as the stock has been dropping, Inotiv has been working to expand its footprint and its services. In November, the company completed its acquisition of Envigo, a global provider of research models and services. The acquisition is expected to enhance Inotiv’s ability to research new drugs and medical devices in the discovery and preclinical phases. Inotiv paid approximately $217 million in cash to make this merger happen.

In February, Inotiv reported its Q1 results for fiscal 2022. The key point here was the surge in quarterly revenue. The total of $84.2 million was up 179% sequentially, and an even more impressive 370% year-over-year. It is important to note that that fiscal Q1, which ended on December 31, 2021, included partial revenue results from the Envigo acquisition.

Turning to the insiders, sentiment here is strongly positive. There have been numerous buys from company officers in the past month, most for $250,000 or less. However, one buy stands out for size – COO James Harkness bought 38,968 shares, reporting a total purchase price of $765,584 for the stock.

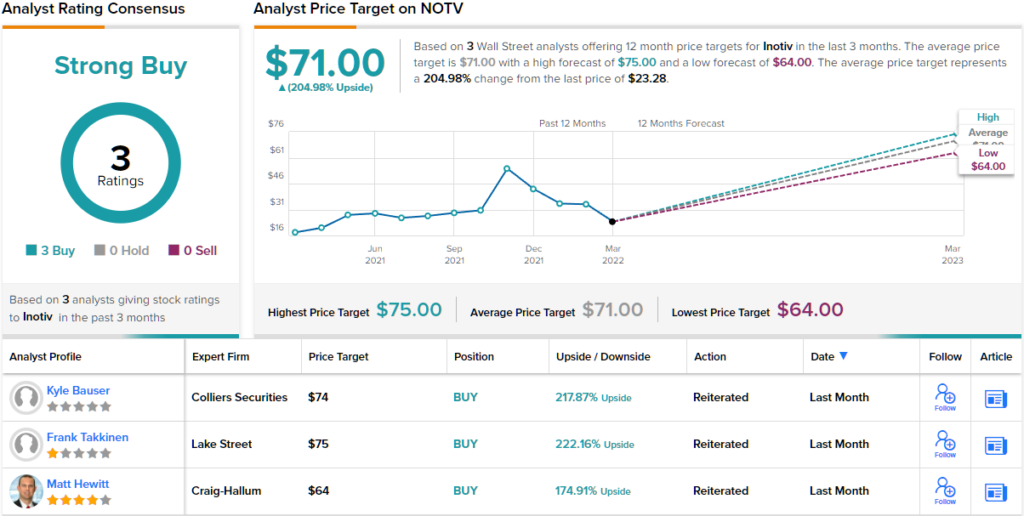

Inotiv has its fans among Wall Street analysts as well. Covering this stock for Colliers, analyst Kyle Bauser likes what he sees in the company’s prospects for continued growth.

“NOTV remains a top pick of ours given the compelling share price, growth trajectory, impressive management team, and pricing power in the marketplace currently… Management continues to target 20% EBITDA margins by executing accretive acquisitions, scaling existing operations, and eliminating redundancies. Given the Company’s growth and margin trajectory, we believe the stock should be trading at least above 4x EV/CY22 sales (2.5x currently),” Bauser opined.

In line with his bullish comments, Bauser gives NOTV stock a Buy rating, and a $74 price target that implies a one-year upside potential of ~218%. (To watch Bauser’s track record, click here)

While Wall Street’s analysts have only put up 3 reviews of this stock, they are all in agreement about its quality, rating it a Buy. This makes the Strong Buy consensus view unanimous, while the $71 average price target suggests an upside of ~205% for the coming year. (See NOTV stock forecast on TipRanks)

Humanigen (HGEN)

Next up in Humanigen, a $250 million dollar biopharmaceutical research company, whose leading drug candidate, lenzilumab, is under investigation in three late-stage clinical trials. Lenzilumab is a potential cancer treatment; two of its trials are evaluating it against acute GvHD and chronic myelomonocytic leukemia, while the third, the SHIELD study, will test lenzilumab as a preventative treatment for CAR-T-related toxicities.

Most importantly, however, Humanigen is moving forward with the ACTIV-5/BET-B study, a clinical trial of lenzilumab as a treatment for COVID-19. The company announced earlier this year that it has achieved target enrollment in the ACTIV-5/BET-B study, which is a follow up to last year’s LIVE-AIR Phase 3 study.

The NIH is sponsoring the ACTIV-5/BET-B follow-on, and has advanced the study from a Phase 2 exploratory to a Phase 2/3 treatment investigation. That modification of the study will enable Humanigen to use it as a confirmatory study in a push forward with a Biologics License Application for lenzilumab as a COVID treatment. Top line data is expected in the next quarter.

Investors should note that company management – and some of Wall Street’s biopharma experts – are sanguine about lenzilumab’s ability to treat COVID, regardless of the variants. Management noted in a recent conference that a patient’s risk of going on a ventilator or dying from the virus was not impacted by which variant caused infection. This is an important finding, that can support lenzilumab as a COVID treatment.

Turning to Humanigen’s other clinical projects, the SHIELD study is on schedule and getting started in the first half of this year. The company has announced that it is in alignment with the FDA on the registration phase of the trial. Initial data is expected for release in December of this year.

Two other trials, the Phase 2/3 RATinG and the Phase 2 PREACH-M, are also getting underway in the first part of this year. The company is in the enrollment stage of RATinG, a clinical trial of lenzilumab against acute GvHD. It has begun dosing patients in the PREACH-M trial against Chronic myelomonocytic leukemia. Both of these trials are expected to reach later stages before the end of 2022.

Humanigen shares have been falling steadily for the past 12 months; the stock is down 80% in that period. However, while the shares are down, CSO and Board member Dale Chappell made a stir and swung the sentiment deep into the positive range with his recent purchase of 1 million shares for a total of $3 million.

This stock has also caught the attention of Oppenheimer’s 5-star analyst Kevin DeGeeter who sees Humanigen positioning itself for future gains.

“HGEN reiterated top-line data readout from ACTIV-5/BET-B study of lenzilumab in COVID-19 in late 1Q22 or early 2Q22. Management considers >20% reduction on the risk of patients progressing to mechanical ventilation or death as clinically differentiated from competitor compounds. Regulatory filings for lenzilumab in treating hospitalized COVID-19 patients are on track pending ACTIV-5 readout. Separately, we view Phase III development of lenzilumab on prophylaxis of CAR-T neurotoxicity as intriguing…. We view the top-line readout from ACTIV-5/BET-B study in late 1Q22/early 2Q22 as the most important upcoming milestone for HGEN,” DeGeeter noted.

DeGeeter is bullish here, and gives the shares an Outperform (i.e. Buy) rating. His $16 price target suggests an upside of 337% for the year ahead. (To watch DeGeeter’s track record, click here)

All in all, Humanigen boasts a unanimous Strong Buy analyst consensus rating, based on 3 recent stock reviews. The shares are selling for $3.66 and their $23.67 average price target indicates an upside of 547% from that level. (See HGEN stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.