Sometimes, a single new data point can break up the most complacent of outlooks. After 10 months of markets trending down, inflation rising, and the Federal Reserve hiking interest rates, it was only natural to assume that the rest of the year held more of the same. And then October’s inflation print broke that mold.

It came in at 7.7% annualized, significantly less than the 8% expected. While still near 40-year highs, and still up 0.4% month-over-month, the October number indicates that the rate of increase may be slowing down. It’s not the end of inflation, but it has given investors a ray of hope. The S&P 500 jumped 5.54%, and the NASDAQ skyrocketed 7.35%, in the aftermath of the inflation data release.

So traders and investors are in optimistic moods, and it has them looking to buy. But a smart investor keeps sight of the underlying facts – and those facts are still tough. Inflation remains high; the Fed is still more likely than not going to raise rates again next month; investors will need a defensive stance to protect their portfolio.

And that’s going to draw us to the high-yield dividend stocks, the market’s classic defensive play. We’ve used the TipRanks data to look up two dividend payers that offer yields that beat the current inflation rate. And even better, they both have a ‘Strong Buy’ consensus rating from the wider analyst community. Let’s take a closer look.

Arbor Realty Trust (ABR)

If you’re looking into champion dividend stocks, we’ll have to look into a real estate investment trust. The companies, REITs, acquire, own, manage, and lease real properties of all sorts, residential and commercial, along with mortgages and mortgage-backed securities, and they are well-known for returning profits to shareholders through high dividends.

Arbor Realty Trust is a commercial REIT, focused on working with developers and funding multifamily residential projects – apartment complexes. Arbor also funds various commercial properties, and works with Fannie Mae and Freddie Mac on loan funding.

2022 has been a difficult year all around, so far, but Arbor has produced consistently strong quarterly financial performances. For the past several years, the company has shown top line revenues that are growing year-over-year – and bottom line earnings that are consistently beating the forecasts. In the most recent quarter, 3Q22, Arbor’s interest income came to $259.8 million, up an impressive 107% from the year-ago quarter.

In a metric of keen interest to dividend investors, the company generated a distributable income of 56 cents per diluted share. This was up 9.8% y/y, but more importantly, the distributable income supports the dividend – and that’s where this stock shines.

On November 4, Arbor declared its Q4 dividend at 40 cents per common share, or $1.60 annualized. This gives a powerful yield of 10.7%, about 5x the average yield found among div stocks in the broader markets. Just as important, Arbor has been raising its dividend for the past 4 years – an enviable record that includes 10 consecutive q/q increases leading up to the current declaration. The 40-cent dividend will be paid out on November 30.

In the eyes of Raymond James analyst Stephen Laws, who holds a 5-star ranking from TipRanks, all of this adds up to a company in a very solid position.

“We expect portfolio performance to remain strong given the multifamily focus with portfolio returns benefiting from higher interest rates, and the agency business and servicing portfolio provides better visibility into future cash flows than most peers. We are reiterating our Outperform rating given the strong 3Q results, our expectation of continued strong portfolio performance, benefits of increasing interest rates, the recent dividend increases, and the strong dividend coverage,” Laws opined.

Laws’ Outperform (i.e. Buy) rating comes with a $18.50 price target, suggesting a one-year upside potential of 24%. Based on the current dividend yield and the expected price appreciation, the stock has ~35% potential total return profile. (To watch Laws’ track record, click here)

Overall, this ‘Strong Buy’ dividend stock has received 5 recent analyst reviews, which include 4 Buys and 1 Hold. The shares are selling for $14.92 and the $16.50 average price target suggests a gain of ~11% in the year ahead. (See ABR stock forecast on TipRanks)

OneMain Holdings (OMF)

From REITs we’ll shift gears and check out a financial firm, OneMain. This company focuses mainly on consumer finance, and offers a wide range of financial services to a sub-prime clientele that would not likely be able to access credit with larger establishment banks. OneMain has built itself into a leader in this niche; its services include consumer finance and credit, affordable loans, and insurance products. While OneMain’s target audience may not always be credit-worthy, the company screens them carefully and, by using equal care in designing its financial products, the company is able to keep the customer default rate to an acceptable level.

The company’s revenues have been consistent over the past couple of years, ranging between $1.2 billion and $1.29 billion. Earnings, however, have been more volatile. The Q3 result of $1.51 per diluted share was down sharply from the $2.37 reported in the year-ago quarter. OneMain finished the third quarter with $536 million in cash and other liquid assets.

This allowed OneMain to support a solid dividend. The company declared its Q4 dividend back in October at 95 cents per common, for payment on November 14. At the current rate, the dividend annualizes to $3.80 and brings a yield of 9.26%. This dividend is fully covered by earnings, compares favorably to the market-average yield of approximately 2%.

Also in Q3, OneMain spent $42 million on the repurchase of 1.2 million shares. With the dividend, this demonstrates the company’s significant commitment to maintaining capital returns to shareholders.

All in all, this stock presents a sound picture for return-minded dividend investors, according to Credit Suisse’s 5-star analyst Moshe Orenbuch.

The analyst says of OMF’s current standing, “Overall, we view the [recent third] quarter as positive. While OMF has significantly tightened credit, they have also taken pricing actions, which should allow yields to improve in 2023. OMF continues to benefit from competitors pulling back given its strong balance sheet that has room for secured funding and staggered debt maturities over the coming years. OMF should continue to generate significant capital, pay high dividend yield and repurchase shares.”

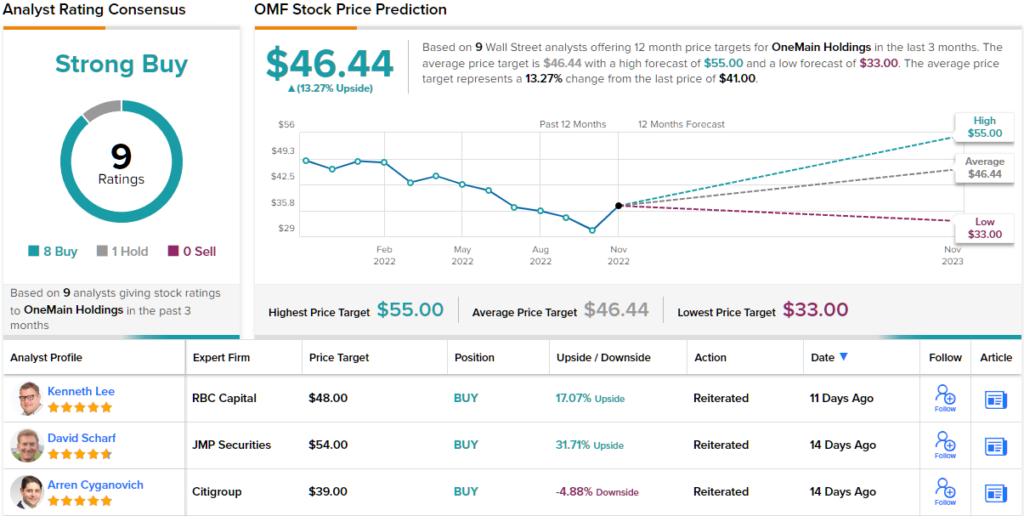

This top analyst doesn’t stop with an upbeat comment; he also gives the shares an Outperform (i.e. Buy) rating and a target price of $47 to indicates potential for ~15% share gains in the year ahead. (To watch Orenbuch’s track record, click here)

This non-traditional financial company attracted 9 analyst reviews recently, a total that includes 8 Buys against a single Hold to support a Strong Buy consensus rating. OMF stock is priced at $41 per share and its $46.44 average price target implies a one-year gain of ~13%. (See OMF stock forecast at TipRanks)

To find good ideas for dividend stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.