Adobe (NASDAQ:ADBE) turned in its earnings report earlier today, and the news was hardly good. Analysts expected Adobe to post earnings per share of $3.35. Adobe actually turned in earnings of $3.40, which was a narrow win for the company. Revenue, however, was a different story. Adobe posted revenue of $4.43 billion, but a FactSet consensus looked for Adobe to post $4.44 billion instead. The guidance also missed as Adobe projected revenue of $4.52 billion versus expectations of $4.6 billion.

Adobe shares have been on a downward slide for most of the year. This time last year, a share of Adobe went for a shade over $665. A series of ups and downs followed, ultimately bringing Adobe shares down to around the low $300 per share level. That’s a loss of over half its value in the space of a year.

Disappointments on several fronts won’t help Adobe recover those year-ago prices, and I’m staying neutral on Adobe in the meantime. Improvements are afoot, certainly, but it’s unclear if they’re enough to drive up share prices significantly.

Investor Sentiment Looks Surprisingly Bright for Adobe Stock

Granted, Adobe’s latest results don’t look all that great. Their future projections are already suggesting disappointment in the making. Despite this, there’s a clear enthusiasm behind Adobe. Adobe currently has a Smart Score of 7 out of 10 on TipRanks. That’s the highest level of “neutral,” which suggests a somewhat better than even chance Adobe will ultimately do better than the broader market.

Meanwhile, Adobe insiders don’t seem daunted by the disappointing earnings or near-term projections. Insider trading at Adobe displays a clear eagerness to buy. While there haven’t been many informative buys or informative sells of late, the aggregate offers a worthwhile perspective.

In the last three months, insiders staged 12 buy transactions but just six sell transactions. A two-to-one ratio of buyers to sellers carries some weight. Looking back at the last 12 months, things get even better for Adobe bulls. Insiders staged 49 buy transactions to 36 sell transactions.

Granted, buyers aren’t quite as enthusiastic looking at the last year. However, the ratio shows there has been buying interest right along. Plus, it’s also clear that the buying interest has only increased, despite the less-than-stellar results produced in the latest earnings report.

Adobe’s Huge Spending and Disappointing Results Don’t Bode Well

Just going by the numbers, things don’t look well at Adobe as things sit. Narrow wins in earnings, misses in revenue, and disappointing projections aren’t buying signals for most investors. Things only get worse when considering Adobe’s spending habits. Adobe announced plans to proceed with the acquisition of Figma, a collaborative design platform. The deal carries a value of $20 billion. Half of that will be paid in cash, and the other half, roughly, in stock.

Adobe is expecting big things out of the Figma acquisition. Picking up Figma, according to a Thursday press release, will “…usher in a new era of collaborative creativity.”. Adobe also expects its new purchase to “reimagine the future of creativity and productivity,” among other things.

It’s unclear, immediately, whether Adobe can fundamentally change the nature of creativity as its press releases suggest. In fact, it’s probably more likely that Adobe’s move won’t have near this kind of reach, despite dropping an 11-figure sum on the deal.

Worse yet, it almost looks like Adobe is preparing a fantastic solution for a problem now largely passed. Most would have welcomed a web-facing collaborative creativity tool when everyone was required to remain in their homes as much as possible by government mandate. The rise of “return to the office” movements will limit the value of remote-ready collaborative tools.

Just to top it off, it’s a brand new collaborative creativity tool launching into some of the worst macroeconomic conditions we’ve seen since 2008. Adobe will have its work cut out for it, pitching such a tool to its current user base in this environment.

As impressive a tool as it will no doubt be, many companies will likely choose to stand pat on current software loadouts rather than add a new, potentially expensive tool to the roster.

Adobe might be able to make a case for its value as a marketing tool. Businesses, after all, will need to market their products particularly hard to get what revenue can be had in this down economy. However, without solid numbers behind it—and it can’t have those numbers given how new the tool would be—it will be a much harder sell.

Is Adobe an Overpriced Stock?

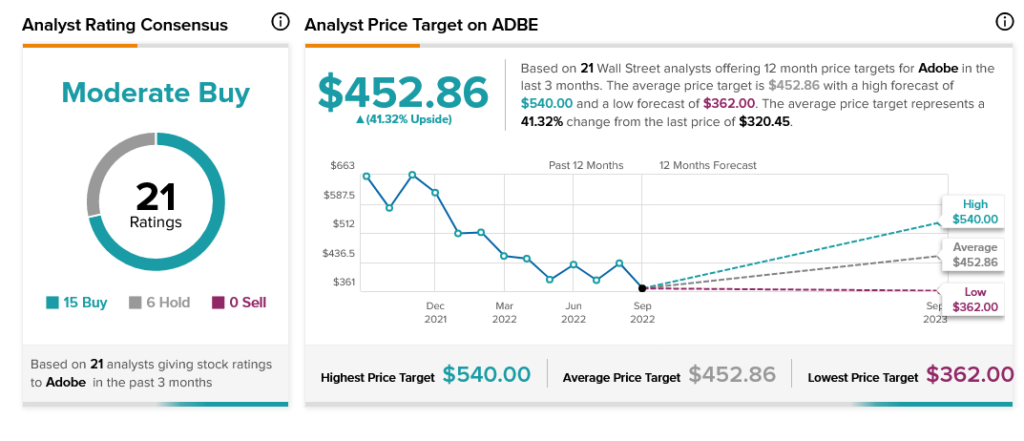

Turning to Wall Street, Adobe has a Moderate Buy consensus rating. That’s based on 15 Buys and six Holds assigned in the past three months. The average Adobe stock price target of $452.86 implies 41.32% upside potential. Analyst price targets range from a low of $362 per share to a high of $540 per share.

Conclusion: Adobe Stock Has an Uncertain Path to Victory

Adobe has a long history of victories behind it, and it certainly doesn’t hurt matters that Adobe is a bargain right now. This morning’s losses have pushed it down to pre-pandemic pricing. However, there are clear problems for Adobe as well. The mixed earnings report, the disappointing future projections going into a period of relatively high demand, and a massive expense laid out for a product of dubious value doesn’t exactly bode well.

This is especially true in the short term, where inflation is driving prices through the roof and most people—not to mention plenty of businesses—are carefully watching their own spending.

That’s why I’m neutral on Adobe. There is a path to victory here, but it requires a lot of circumstances to precisely line up and produce a positive outcome. The sheer unlikelihood of such an outcome is enough to keep me back.