Arm Holdings (ARM) is one of the lesser-known semiconductor companies powering many of the world’s advanced devices. However, it has a business model that is different from other major chip companies. In fact, it enjoys theoretically indefinite revenue visibility through a royalty model that reduces highly cyclical demand dynamics. Despite having a positive view about its business operations, the stock is heavily overvalued, leading me to a Sell rating on the stock.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

Arm Holdings Has a Unique Model for High-Margin Growth

Although my overall sentiment on the stock is negative, Arm robustly operates a distinct fabless business model, focusing exclusively on designing and licensing semiconductor intellectual property rather than manufacturing physical chips. This has allowed the company to command a gross profit margin of over 95% while earning an upfront fee and collecting ongoing royalties for every chip sold using its designs. Due to the low capital intensity of the business, it is also a consistent free cash flow generator.

Arm is known to dominate the smartphone central processing unit intellectual property market, with a 99% share, but it also serves IoT, automotive, and data center markets. However, it’s worth noting that with 13% of its revenue coming from China, trade tensions could negatively impact sales in the country over the medium term, similar to how Nvidia is currently suffering. Nevertheless, ARM is currently expected to achieve a 22.5% annual revenue growth rate over the next three years.

New Products Are Commanding Higher Royalties

In addition, recent technological developments, such as the Armv9 chip architecture, are commanding double the royalty rates of its predecessor, Armv8. This is largely due to enhanced AI and machine learning capabilities, as well as improved energy efficiency. Such Armv9 chips now constitute approximately 25% of Arm’s royalty revenue, with adoption expanding into more markets like data centers and automotive systems.

Before we get to my comprehensive valuation analysis, which shows a significant overvaluation in the company’s stock price at present, the operational model and company direction deserve acknowledgment of merit. There are few companies like Arm Holdings with such a moat around a high-growth, recurring revenue business model—this is primarily why the market has become irrationally bullish on the stock and priced it unsustainably.

Arm Stock’s Valuation Is Likely Unsustainable

Due to Arm Holdings’ recurring revenue model, it is appropriate to hold its stock for five years or more if the valuation is reasonable. However, as my analysis will show, it is overpriced. Therefore, I am confidently bearish on the stock for now until a better price is offered by the market. To begin the valuation, I will start with the company’s trailing 12-month revenue of $3.535 billion. Currently, it is probable that sales will grow at around a 20% compound annual growth rate over the next five years. Therefore, I forecast that the company will generate $8.79 billion in sales by 2030.

Next, it is worth noting that the company’s net margin has come close to 30%, on an adjusted basis, in the past. As a result, it is not unreasonable for profitability to reach a 35% margin by January 2030 due to economies of scale and a stronger moat. Therefore, my conservative January 2030 net income target for Arm Holdings is $3.08 billion. If the company’s diluted share count increases moderately to 1.1 billion, it will then have a diluted earnings per share value of $2.80.

Finally, I will select a valuation multiple. Companies in the semiconductor space at the cutting edge typically trade at a price-to-earnings ratio of around 50, like Nvidia (NVDA). This is the multiple I will be using in my model, especially as Arm benefits from more recurring revenue opportunities than Nvidia. The result is a January 2030 stock price target of $140. The current stock price is $147.50, so the implied five-year compound annual decline rate is -1%.

What Does Wall Street Say About Arm Stock?

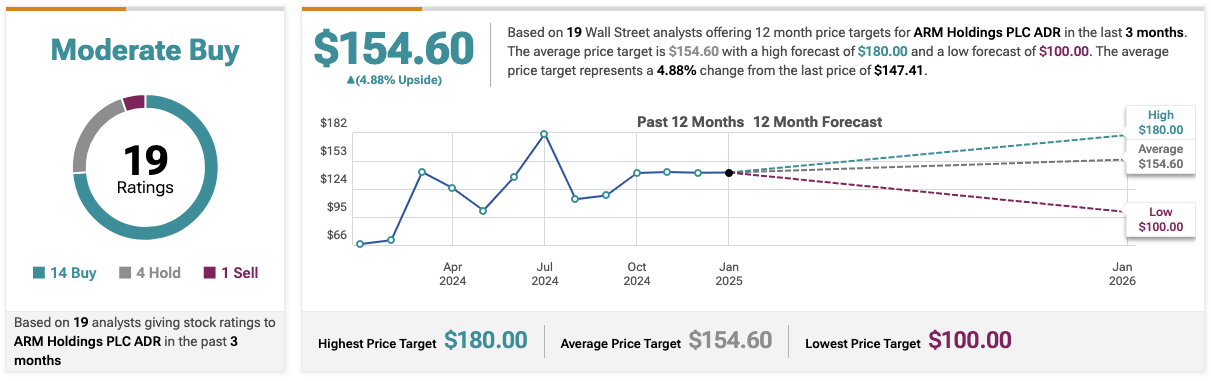

On Wall Street, Arm Holdings has a Moderate Buy consensus rating, but it is clearly viewed as richly valued, given that the average ARM price target of $154.60 indicates only a potential 4.88% upside over the next 12 months. Therefore, I am bearish on Arm stock despite a relatively neutral price target on Wall Street. The Wall Street consensus rating is based on 14 Buys, four Holds, and one Sell.

Conclusion: Arm Stock Carries Too Much Risk

When I look for investments, I want a substantial margin of safety to allow for security in my capital allocation. Unfortunately, Arm stock has the opposite of this, and therefore, I do not consider it a wise long-term or near-term investment at the present valuation. That said, if the stock price were to drop heavily, a buying opportunity could emerge because the company’s business model is distinct, robust, and supported by long-term revenue visibility through recurring sales.