With just two months left in 2024, the big question for investors is, where will the markets go? Year-to-date, the trend has been strongly upward, and even last Friday’s lukewarm October jobs report (only 12,000 net new positions reported) didn’t derail the day’s trading. In fact, the poor jobs numbers have market watchers more certain than ever that the Fed will cut rates again this month, and possibly in December, too – which will be supportive of equities.

Invest with Confidence:

- Follow TipRanks' Top Wall Street Analysts to uncover their success rate and average return.

- Join thousands of data-driven investors – Build your Smart Portfolio for personalized insights.

Watching these conflicting currents, the team at Goldman Sachs sees reason to stay in the stock market, and to diversify holdings. Move beyond the mega-cap tech firms, and look for strength in the fundamental sectors: industry, finance, building, and energy.

The bank sums it up in the ‘conviction list’ for November 2024, writing, “Our strategists are calling for a broadening of the market beyond mega-cap Tech as the post-pandemic echo-boom matures amidst a rate cutting cycle… Looking at the top 10 stocks in the S&P 500 for October we find a very diverse group of companies from a wide range of sectors from industrials to consumer, financials and more… This outperformance highlights just how much alpha is still sitting out there in a market trading at a 2025 P/E of 21.7X… A solid (albeit not spectacular) 3Q earnings season, so far, is contributing to the diverse stock performance and the broader uptick in equities…”

Goldman Sachs analysts are turning this stance into specific stock picks, naming some interesting choices on the firm’s Conviction List – choices that could outperform the S&P 500 going forward. Using the TipRanks database, we’ve looked up the details on two of their favorites. Let’s dive in.

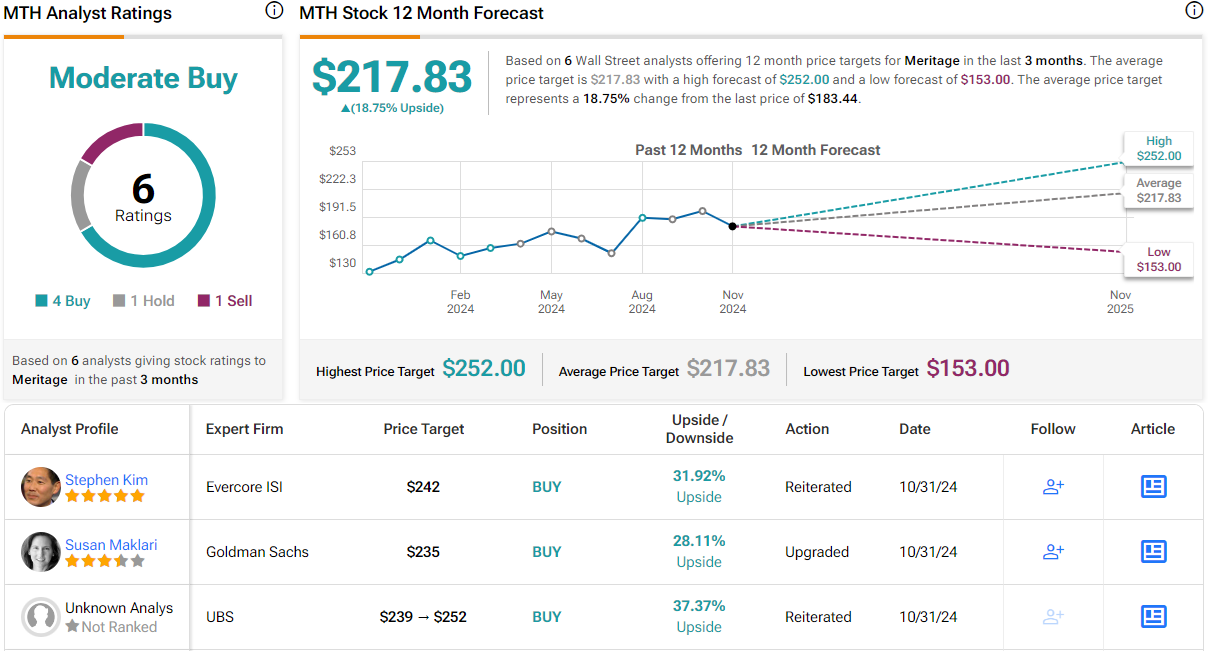

Meritage Homes Corporation (MTH)

The first stock we’ll look at, Meritage Homes, comes from the construction industry, where it is ranked among the top five homebuilders in the US market. Meritage has been in business since 1985, and from its base in Scottsdale, Arizona, oversees operations in Arizona, California, Colorado, Florida, Georgia, North Carolina, South Carolina, Tennessee, Texas, and Utah. The company specializes in affordable homes, both entry-level targeted at first-time buyers and first move-up homes for homeowners looking to expand. The company has a solid reputation for building energy-efficient homes, with distinctive styling and quality construction. Since its founding, Meritage has delivered over 190,000 completed homes to its customers.

The company reported Q3 earnings last week. Revenue reached $1.59 billion, a figure that was down 1.2% year-over-year, but met Street expectations. Meritage dialed in EPS of $5.34, an 11% decline vs. the prior year period but 37 cents per share better than had been anticipated. Meritage closed on 3,942 homes during the quarter, and reported 3Q orders for 3,512 homes. Entry-level homes made up 92% of the quarterly sales orders, up from 88% in the prior year period.

Looking forward, Meritage sees solid prospects – the company reported that it had a 145% backlog conversion rate at the end of 3Q24, a company record.

Looking at this homebuilder for Goldman Sachs, analyst Susan Maklari sees the company in a sound position for growth in the coming year. She writes of MTH, “We believe Meritage’s strategy of offering quick close, move-in ready new homes leaves it well-positioned for above average growth as we believe they offer a more compelling alternative to existing units. In our view, this will increase the ROE by ~70bps to 14.8% through 2025 from 14.1% last year, narrowing the gap vs peers by ~70bps, supporting upside potential in the stock… we see the current valuation as an attractive entry point…”

Maklari’s stance supports her upgrade on MTH to a Buy rating (from Neutral), and her price target, raised from $205 to $235, implies an upside of 28% for the coming year. (To watch Maklari’s track record, click here)

Overall, Meritage holds a Moderate Buy consensus rating from the Street’s analysts, based on 6 reviews that include 4 to Buy and 1 Hold and Sell, each. The shares are priced at $183.44 and the average price target of $217.83 suggests a gain of 19% in the next 12 months. (See MTH stock forecast)

Suncor Energy (SU)

The next stock we’ll look at lives in the energy sector. Suncor Energy, operating out of its Calgary headquarters, specializes in working the oil sands of Alberta. The company is known as a major producer of synthetic crude, the product of the upgrade processing of the bitumen and heavy oil extracted from the sands. The company has its hands in all aspects of the oil sands – from extraction and production ops, to upgrading, to refining into usable fuels. Suncor boasts a $48 billion market cap and generated total revenues of $37 billion-plus last year.

Suncor aims to become Canada’s leading energy producer, and the company holds a strong position to that end. The oil sands of northeastern Alberta – where Suncor conducts the majority of its operations – are one of the world’s largest unconventional oil resources, and contain the world’s fourth-largest proven reserves, of approximately 158 billion barrels. Alberta’s oil sands have, over the past decade, made Canada a major player on the global energy scene, and Suncor, which saw upstream production of 771,000 barrels per day in the second quarter of this year, is a large part of that success.

Suncor’s last reported financial results covered 2Q24. The company’s net earnings came to C$1.57 billion and net EPS was reported as C$1.22. The ‘free funds flow,’ or free cash flow, was listed as C$1.35 billion, up almost 30% year-over-year.

Of particular interest to investors, Suncor has a commitment to capital return. During Q2, the company executed C$825 million in share repurchases and paid out C$698 million in stock dividends; the total return came to more than C$1.5 billion.

Goldman’s energy sector expert Neil Mehta likes Suncor’s positioning, and notes both the resources of the oil sands and the firm’s strong potential for generating free cash flow, writing, “SU’s Canadian oil sands assets have a long life with a low decline rate which should drive sustained strong FCF generation and enable a positive inflection in capital returns as the company achieves its leverage target — all complimented by a new management team with a proven track record of turning around assets…”

Getting into specifics, Mehta adds, “We remain constructive on the stock and continue to highlight expectations for continued operational execution across Upstream and Downstream asset base coupled with continued commitment to deleveraging and shareholder returns on path to achievement of the C$8 bn net debt target. On capital returns specifically, we expect the company to return ~C$5.3/~C$7.0 bn to shareholders in 2024/2025, representing ~8%/~10% yield (respectively).”

Mehta’s ‘constructive’ stance backs up his Buy rating here, while his US$45 price target implies that SU will gain 20% in the year ahead. (To watch Mehta’s track record, click here)

Suncor has 11 recent analyst reviews on record, including 7 to Buy and 4 to Hold, for a Moderate Buy consensus rating. The shares are trading for $37.59 and their $42.62 average price target suggests that they will appreciate by 13% on the one-year horizon. (See SU stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.