Is anything going to get in the way of the stock market’s rally? Even as the U.S. is expected to report a serious quarterly drop in GDP and unemployment rates remain at elevated levels, the market’s leap forward hasn’t been derailed, with the S&P 500 up 45% since hitting a low point on March 23.

Maximize Your Portfolio with Data Driven Insights:

- Leverage the power of TipRanks' Smart Score, a data-driven tool to help you uncover top performing stocks and make informed investment decisions.

- Monitor your stock picks and compare them to top Wall Street Analysts' recommendations with Your Smart Portfolio

At the same time, the rate of new COVID-19 cases is climbing at a record-breaking pace, making it clear that the virus will be with us for some time. Given this alarming disconnect, it has become even more challenging to predict where the market might be heading.

That’s not to say there aren’t any compelling plays out there. Against this backdrop, the pros from investment firm Goldman Sachs argue that a select few actually stand to gain, pointing to two stocks in particular that represent exciting opportunities.

While the firm’s analysts believe both are poised to surge at least 30% in the year ahead, we wanted to get the rest of the Street’s opinion. After using TipRanks’ database, we learned that each ticker has scored Buy ratings from other members of the analyst community as well.

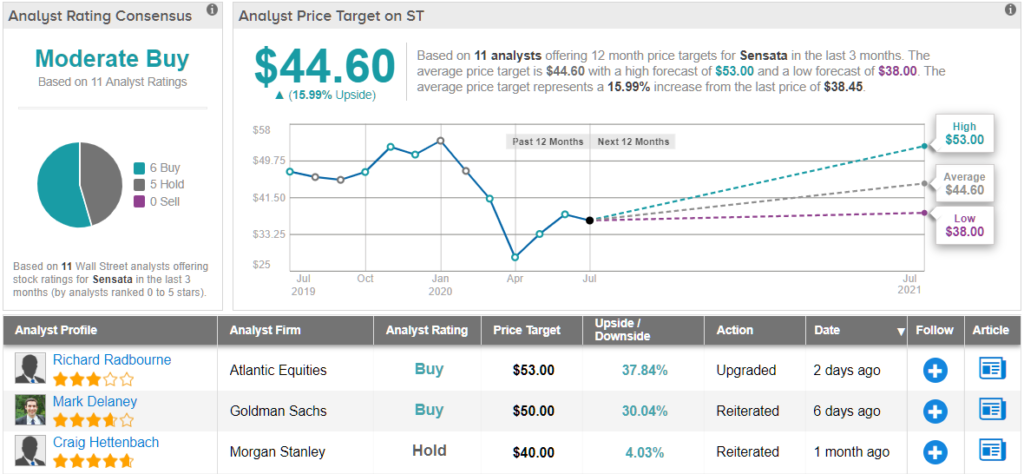

Sensata Technologies Holding (ST)

First up we have Sensata Technologies, which offers mission-critical sensors and controls designed to provide cleaner, safer and more efficient solutions. Recently earning a place on Goldman Sachs’ Conviction List, the firm believes that big things could be on tap.

Representing the firm, analyst Mark Delaney tells clients that multiple factors are driving his bullish thesis. First and foremost, thanks to both the GIGAVAC acquisition (for electrical contractor products) and momentum related to products in thermal management, batteries and e-motors, the company’s content per vehicle (CPV) in EVs is almost $50 in developed markets and is above traditional ICE vehicles at roughly $40.

“We believe that Sensata is now more clearly a winner from the transition to EVs (as its EV content was previously in line with or below an ICE vehicle) and positions the company well as electrified powertrains take share from ICE vehicles,” the analyst commented.

In addition, Delaney argues that there have been improvements within the cyclical space. To back this claim up, he cites the fact that end demand in autos and industrials is trending higher. Looking more closely at the data, U.S. auto sales hit 13.1 million in June, up from 12.2 million in May and 8.6 million in April. Not to mention auto sales in China have also started to bounce back.

It doesn’t hurt that “shares trade at a discount to peers including TEL, APH and APTV on P/E,” with ST’s strong positioning potentially causing this discount to narrow.

While Delaney’s estimates for Q2 remain the same, he stated, “The timing for our Conviction List (CL) addition is to reflect the continued improved end demand signals (e.g. better June U.S. auto sales and PMI data) that haven’t materially impacted Sensata shares but give us more confidence about Sensata’s fundamentals in 2H20 and in 2021.”

Everything that ST has going for it keeps Delaney standing squarely with the bulls. To this end, he left a Buy rating and $50 price target on the stock. Should the target be met, a twelve-month gain of 30% could be in store. (To watch Delaney’s track record, click here)

Turning now to the rest of the Street, opinions are split almost evenly. 6 Buys and 5 Holds add up to a Moderate Buy consensus rating. At $44.60, the average price target brings the upside potential to 19%. (See Sensata stock analysis on TipRanks)

Ally Financial (ALLY)

As for the second stock on our list, Ally Financial helps its customers address their banking, auto and investing needs. While this name has underperformed the broader market in 2020, Goldman Sachs thinks that better days are on the horizon.

Analyst Ryan Nash acknowledges that the rate environment for financials is “challenging,” but he sees ALLY as a “rare secular margin expansion story.” He explained, “Given the unique nature of ALLY’s loan book (retail auto loans coming on well above backbook yields in recent years, LIBOR floors hedging much of the corporate finance business from further pressure) and its ongoing success in optimizing its funding strategy through the growth (and gradually decreasing price sensitivity) of its online funding base, we expect ALLY to be one of few net interest margin expansion stories in the space over the next 18 months.” This tangible margin expansion could come at the beginning of 2H20, in Nash’s opinion.

Adding to the good news, due to stable longer-term retail auto yields as well as tailwinds from funding optimization through debt roll-off and its expanding deposit base, the company could see its post-COVID returns land in the double-digits.

It should also be noted that during the last few years, ALLY has leveraged its digital banking platform to shift the funding mix away from short-term borrowing and other higher cost funding sources towards its online deposit franchise. According to Nash, this helped the company reach its goal of 75% deposit funding in Q4 2019.

Expounding on this, Nash said, “While in earlier years growth was driven primarily by its CD offerings, suggesting a price sensitive customer base, the mix of growth has shifted toward greater success with its online savings account (OSA) product over time, and ALLY managed to move quickly in repricing both products while continuing to grow. As result, we model deposit costs declining nearly 30 basis points on an average quarter-over-quarter basis in Q2 2020, with the tailwind persisting through 2020 and (to a lesser degree) into 2021.”

Some investors have expressed concern regarding its high deferral rates in commercial and retail auto, which land at approximately 0.6x TBV. However, Nash believes this has already been built into the share price, with the conservative reserve levels suggesting “tangible book value stable to expanding beyond Q2 2020.”

“While multiples are unlikely to expand fully back to pre-COVID levels for some time, we expect to see ALLY outperform and regain a portion of its current discount as margin expands into 2021 and the market gets greater clarity on the manageability of losses over time,” Nash added.

Based on all of the above, Nash gave ALLY a thumbs up, rating it a Buy. Along with the call, a $28 price target is attached to the stock. This figure implies ALLY could surge 35% in the next year. (To watch Nash’s track record, click here)

Judging by the consensus rating, the bulls have it on this one. Out of 14 total reviews published in the last three months, 11 analysts rated the stock a Buy, while 2 said Hold and 1 said Sell. As a result, ALLY gets a Moderate Buy consensus rating. Given the $26.08 average price target, shares could rise 29% in the next twelve months. (See ALLY stock-price forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.