Stocks started this year with heft gains, edged back last week, and now are rising again. The big tech giants led the moves, with volatility in Apple and Amazon leading the NASDAQ on its gyrations.

Don't Miss Our Christmas Offers:

- Discover the latest stocks recommended by top Wall Street analysts, all in one place with Analyst Top Stocks

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

The strategy team at investment bank Goldman Sachs have taken notice of the market shakeups, and are working out what it means for investors. According to macro strategist Gurpreet Gill, watching bond yields and stock values closely, “The rise in global yields is a reflection of improved growth prospects given encouraging vaccine progress and in the US forthcoming sizeable fiscal stimulus. [It] also signals higher inflation expectations and in turn pulled forward expectations for the timing of monetary policy normalization.”

Monetary policy may be key to calming investor worries – and on that score, Federal Reserve Chair Jerome Powell’s testimony to Congress is seen as positive. In his comments to lawmakers, the head of the central bank indicated that the Fed has no intention to raise interest rates any time soon.

So far, the outlook is in-line with predictions made by Goldman economist Jan Hatzius, who stated his belief earlier this year that the Fed would hold tight on rates and that 2021 will be a good year for long positions on stocks.

So much for the macro outlook. At the micro level, turning to individual stocks, Goldman’s analysts have been busy locating the equities which they believe will gain should current conditions hold for the near- to mid-term. They found two stocks in particular with, in their view, 50% or higher upside potential. Using TipRanks’ database, we found out both tickers also sport a “Strong Buy” consensus rating from the rest of the Street.

Vinci Partners Investments (VINP)

The first Goldman pick we’re looking at is Vinci Partners, an alternative investment and asset management firm based in Brazil. The company offers customers a range of services and funds, including access to hedge funds, real estate and infrastructure investment, private equity, and credit investment. Vinci boasts a global reach and a leading position in Brazil’s wealth management industry.

To start the new year, Vinci went public on the NASDAQ index. VINP shares started trading on January 28, at $17.70, slightly under the company’s initial pricing of $18. The first day’s trading saw 13.87 million shares of VINP go on sale. After some 4 weeks on the public markets, Vinci has a market cap of $910 million.

Covering this stock for Goldman Sachs, analyst Tito Labarta describes Vinci as a well-diversified asset platform with strong growth potential.

“We think Vinci is well positioned to gain share and outpace market growth given strong competitive advantages. Vinci has one of the most diverse product offerings among its alternative asset management peers, with seven different investment strategies and 261 funds. Moreover, Vinci has outperformed its benchmarks in all strategies, having a strong track record and being recognized with awards from relevant institutions, such as Institutional Investor, Morningstar, Exame and InfoMoney. The company has developed strong communication tools to reinforce its brand and institutional presence in the Brazilian marketplace, such as podcasts, seminars, investor days with IFAs, among other participations in events and webinars,” Labarta opined.

In line with his upbeat outlook, Labarta rates VINP a Buy, and his $39 price target implies an impressive 141% upside potential for the year ahead. (To watch Labarta’s track record, click here)

One month on the NASDAQ has brought Vinci positive attention from Wall Street’s analysts, with a 3 to 1 split in the reviews favoring Buys over Holds and giving the stock its Strong Buy analyst consensus rating. The stock is currently selling for $16.15 and its $26.75 average price target suggests it has room for ~66% growth in the next 12 months. (See VINP stock analysis at TipRanks)

Ortho Clinical Diagnostics Holdings (OCDX)

Goldman Sachs analysts have also pointed out Ortho Clinical Diagnostics as a potential winner for investors. This company, a leader in the field of in vitro diagnostics, works with hospitals, clinics, labs, and blood banks around the world to deliver fast, secure, and accurate testing results. Ortho Clinical Diagnostics possesses several important ‘firsts’ in its industry: it was the first company to deliver a diagnostic test for Rh +/- blood typing, for detection of HIV and HEP-C antibodies, and more recently has been working on COVID-19 tests.

Ortho is the world’s largest pure-play in vitro diagnostics company, handling over 1 million tests every day, from more than 800,000 patients around the world.

Like Vinci Partners above, this company went public on January 28. The IPO saw Ortho put 76 million shares on the market, with trading on the first day opening at $15.50, below the $17 initial pricing. Even so, the IPO raised $1.22 billion in gross funds, and the over-allotment option from the underwriters brought in an additional $193 million.

Goldman Sachs analyst Matthew Sykes believes the company’s past growth performance justifies a positive sentiment, and that Ortho is capable of deleveraging its balance sheet.

“The key to the equity story for OCDX is successfully resetting their organic growth rate to a durable 5-7% from an historical pace of roughly flat. Given the level of profitability and potential FCF generation, if OCDX were to reset growth, they could delever the balance sheet and increase their level of inorganic and organic investments to create a durable growth algorithm,” Sykes wrote.

The analyst added, “The key growth driver in our view is the increase in OCDX’s lifetime customer value driven by a transition in the product set of their Clinical Lab business from a stand-alone clinical chemistry instrument to an integrated platform and ultimately to an automated platform. This transition is taking place largely within their own customer base, therefore is not dependent upon displacement, but rather serving the need of increasing throughput of a customer’s diagnostic capabilities.

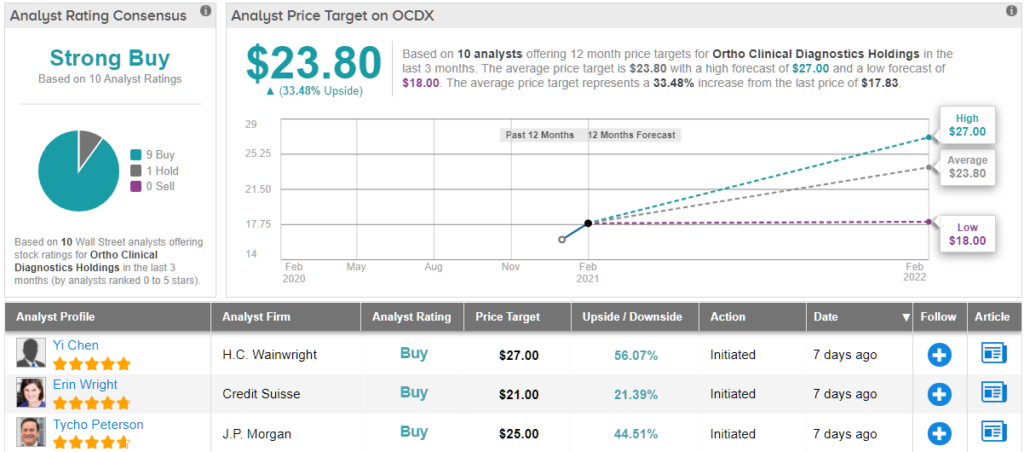

To this end, Sykes rates OCDX a Buy, and sets a $27 price target. At current levels, this implies a one-year upside of 51%. (To watch Sykes’ track record, click here)

Ortho has a long history of delivering results for its customers, and that has Wall Street in a mood to rate the stock well. OCDX shares get a Strong Buy from the analyst consensus, based on 9 Buy reviews set since the IPO – against a just a single Hold. The average price target is $23.80, indicating ~33% upside potential from the current trading price of $17.83. (See OCDX stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Bank Stocks, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.