Investors weren’t too pleased with Global Payments’ (GPN) latest quarterly statement, sending shares down by 9% in the subsequent session. But is the sell-off justified?

Don't Miss Our New Year's Offers:

- Discover the latest stocks recommended by top Wall Street analysts, all in one place with Analyst Top Stocks

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

Despite getting out of Russia – the result of which will be ~$20 million impact and additional negative FX headwinds – the company maintained its 2022 outlook. Specifically, revenue is still expected to come in between $8.42 billion and $8.5 billion in 2022, amounting to 9% to 10% growth. Adj. EPS is also expected to climb 16% to 19% higher and reach between $9.45 and $9.67.

There was also a bottom-line beat in the first quarter with adj. EPS hitting $2.07, just above Wall Street’s $2.04 expectation. However, GPN slightly missed on the top-line figure, as revenue rose by 7.7% year-over-year to $1.95 billion, just below the $1.96 billion consensus estimate.

Raymond James’ John Davis calls the Q1 print “mixed,” highlighting that operating profit dollars also “narrowly missed” Street expectations and coming in at $803 million compared to the $805 million forecast. And even though operating margin rose by 50 bps year-over-year, the Street expected a ~10 bps expansion.

That said, with merchant volumes showing a healthy 18% year-over-year uptick, the stage is set for “accelerated growth in the 2H and into FY23/FY24.” There’s also the prospective sale of consumer debit card business Netspend to look forward too, which could “pave the way for further capital deployment.”

But more than anything, for Davis, following the recent sell-off, the stock’s valuation is “simply too attractive.”

“GPN offers one of the more compelling risk/rewards within our coverage, in our view,” the analyst said. “Consider, the stock trades at just 11x our FY23 estimates, despite sustainable high teens EPS growth. Said differently, GPN is trading at one of the lowest PEGs within large cap payments (0.6x).”

As such, Davis maintains an Outperform (i.e. Buy) rating, along with a $190 price target. Therefore, the analyst expects the stock to change hands for 48% premium over the next 12 months. (To watch Davis’ track record, click here)

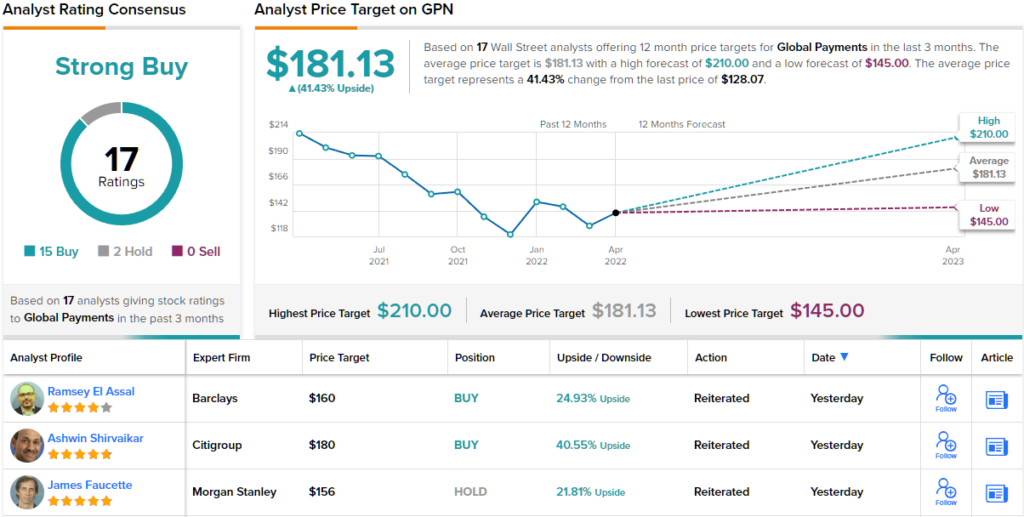

Most of Davis’ colleagues concur; barring two skeptics, all 15 other recent reviews are to Buy, making the consensus rating here a Strong Buy. The forecast calls for 12-month gains of 41%, considering the average price target stands at $181.13. (See GPN stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.