GasLog Partners LP (GLOP) is a growth-oriented MLP focused on acquiring, managing, and employing LNG carriers utilized in LNG transportation through multi-year charters.

The partnership has expanded its fleet significantly since it first went public in 2014. Specifically, the partnership has gone from three vessels to 14 as of today, with nine of them running with modern TFDE propulsion technology. The other five are conventional steam vessels.

I am neutral on the stock.

Why Did Units Collapse?

Unfortunately, the partnership’s fleet development from its IPO up until recently came in at a great cost, despite fulfilling GLOP’s growth targets. In particular, for GLOP to fund the purchase of these vessels, a significant chunk of common units, preferred shares, and long-term debt was issued, thus deteriorating unitholders’ capital.

For example, GLOP’s publicly traded preferred shares were issued with initial yields stretching from 8% to 8.63%. Thus bottom-line margins were compressed, while GLOP’s balance sheet became overburdening on the liabilities side. With the unit price crumpling from its IPO levels, GLOP’s cost of equity became even more expensive over time when it came to future unit issuances to fund vessel acquisitions, creating a downwards spiral in unitholders’ equity value.

You can see the effects these issuances had on the common units over the past several years, with the stock trading at a fraction of its past levels. You may wonder why would the partnership make such disastrous investments. In short, charter rates were expected to improve over the years, and that didn’t meaningfully materialize in time.

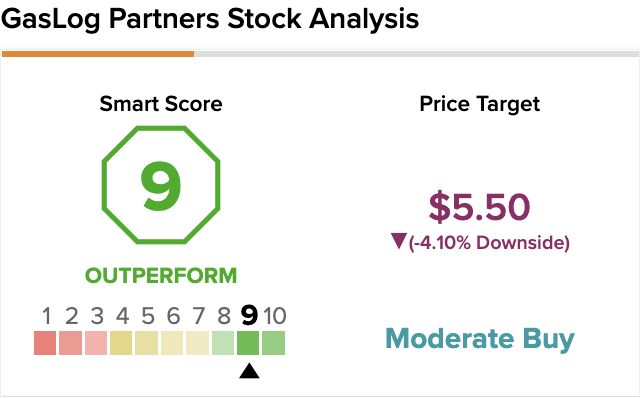

On TipRanks, GLOP scores a 9 out of 10 on the Smart Score spectrum. This indicates a potential for the stock to outperform the broader market.

Improvement Prospects

Following Russia’s invasion of Ukraine, the market dynamics have completely shifted. The West has been concentrating its efforts on achieving energy independence. Therefore, the demand for LNG carriers has increased dramatically, which should result in higher charter rates, and thus improved profitability for companies in the space.

This is illustrated in GLOP’s stock price, which has rallied by nearly 70% over the past year. Investors likely expect enhanced profitability prospects will allow the partnership to improve its balance sheet and get it to a healthier state.

Such efforts have taken place lately, with the most noteworthy development being the continuous reduction of long-term debt. Since pausing its fleet expansion, the partnership has been allocating the cash flows from the vessels’ charters to decrease its long-term debt. Specifically, long-term debt has declined from $1.29 billion in mid-2019 to $953.2 million, as of its latest quarterly earnings.

To further ease the balance sheet, GLOP has also been buying back its preferred shares in the open market. Similar to the coupons on debt, though distinct in some respects, preferred dividends can be deemed as compulsory “interest payments” for the partnership. By buying back roughly $18.4 million worth of preferred shares during Fiscal 2021, the company achieved around $1.5 million worth of preferred dividend savings per annum.

In Q1 2022, the company repurchased an additional $10 million worth of preferred shares, extending its annual savings on preferred dividends to $2.4 million per annum.

Further, it’s worth noting that GLOP’s series C preferred stock has a fixed-to-floating structure that kicks in after the Series’ call date in 2024. This implies that either GLOP will call this Series by 2024, lowering its overall preferred obligations substantially, or it won’t.

In that case, the dividend rate on Series C will decline from its current 8.5% rate to LIBOR plus a spread of 5.317%. Assuming LIBOR remains under 2-3%, the company will achieve some sort of savings, even if it doesn’t call/repurchase all of its Series C preferred stock.

Overall, by reducing its liabilities, GLOP’s balance sheet should continue improving over the medium term. With higher rates potentially leading to improved charters moving forward, GLOP’s profitability has finally the potential to improve meaningfully moving forward.

Can Distributions Resume?

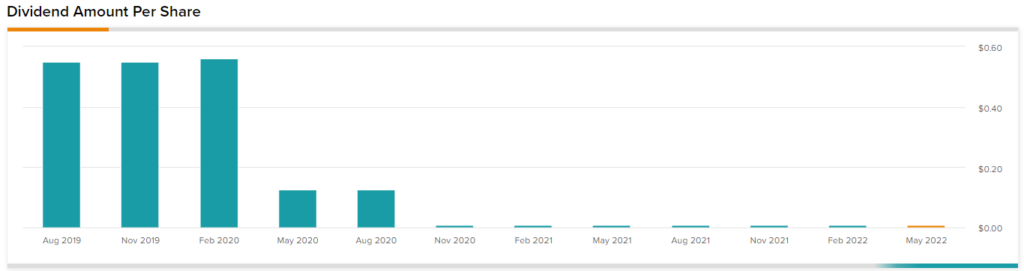

Due to its MLP structure, GLOP is set up to distribute most of its net income to unitholders. Nevertheless, as a result of the challenges described earlier, the partnership has cut its distributions per share more than once. The most recent distribution cut practically discontinued payouts altogether, with the ongoing quarterly rate at a tiny $0.01.

On the positive side, since GLOP’s balance sheet has been improving lately and the ongoing macroeconomic developments should benefit its medium to long-term earnings, distributions could resume strongly.

The partnership is anticipated to post earnings per share close to $1.50 in fiscal 2022. Supposing GLOP were to commence paying out just $0.50 per annum, that would attach a yield close to 8.7% at GLOP’s current price levels. Still, the timing of such a resumption is ultimately speculative.

Wall Street’s Take

Turning to Wall Street, GasLog Partners has a Moderate Buy consensus rating based on one Buy and two Holds assigned in the past three months. At $5.50, the average GasLog Partners price target implies 4.10% downside potential.

Takeaway

GLOP is currently trading at just 3.8 times this year’s projected earnings, though units appear rather cheap for a reason. While the ongoing macroeconomic environment could be a tailwind to the company’s future earnings prospects, the partnership is more than likely to continue improving the balance sheet before any meaningful distributions occur. After all, GLOP’s total debt is around 1.8 times the value of its common equity.

By the time the balance sheet has been improved adequately, who knows if the macro environment will be favorable or hostile for GLOP? Therefore, there is undoubtedly a lot of uncertainty and speculation regarding GLOP’s investment case. Investors must be wary of the underlying risks before allocating capital to the stock.

Questions or Comments about the article? Write to editor@tipranks.com