Fortinet (FTNT) is a cybersecurity company with operations around the globe. The company is expected to grow fast and is an industry leader.

Stay Ahead of the Market:

- Discover outperforming stocks and invest smarter with Top Smart Score Stocks

- Filter, analyze, and streamline your search for investment opportunities using Tipranks' Stock Screener

However, we estimate that the stock price is slightly above its fair value under current market conditions. As a result, we are neutral on the stock.

Growth Catalysts

Fortinet operates in the cybersecurity industry, which was valued at $156 billion in 2020. The industry is expected to grow at a compound annual growth rate of 14.5% between 2021-26, equating to a future value of $352 billion.

The industry growth is driven by an increasing reliance on technology, which inevitably leaves people and businesses more vulnerable to cyber threats. In fact, the Federal Reserve views cyberattacks as one of the most serious threats to the wider financial system.

Thus, it’s no coincidence that cyberattacks have been increasing each year. In 2017, the number of organizations compromised by at least one successful cyberattack was 77%. In 2021, this number had increased to 86%.

As a result, these industry tailwinds alone should provide Fortinet with strong growth catalysts. However, there might be an opportunity for the company to grow through acquisitions because it is one of the larger players in a very fragmented industry.

Risks

Like any high-tech, fast-growing industry, there is always the risk that a competitor might develop some breakthrough technology that renders the existing technology obsolete.

If Fortinet were unable to successfully adapt to new technologies, it could quickly begin to lose market share. As mentioned earlier, Fortinet could use acquisitions to mitigate such risks or to increase market share.

However, acquisitions pose risks of their own. To begin with, the premium above the market value that would need to be paid for companies in a fast-growing industry would be substantial. That’s on top of the already high valuations most cybersecurity companies have relative to fundamentals.

Therefore, the risk of overpaying for an acquisition would need to be considered as that would not create value for shareholders. Furthermore, there are integration risks where the acquired company might not fit as well as expected. In such a situation, the acquisition would fail to create any synergies.

Valuation

To value Fortinet, we will use the H-Model, which is similar to a three-stage DCF model. The H-Model assumes that growth will decelerate linearly over a specified period of time. We believe this is a reasonable assumption as companies gradually slow down as they mature.

The formula is as follows:

Stock Value = (CF(1+tg))/(r-tg) + (CFH(hg-tg))/(r-tg)

Where:

CF = cash flow per share

tg = terminal growth rate

hg = high growth rate

r = discount rate

H = half-life of the forecast period

For Fortinet, we used the following assumptions:

CF = $6.81 per share (we used the Fiscal Year 2021 estimates for FCF)

tg = 2.079%

hg = 25.0%

r = 6.808%

H = five years (we are assuming it will take 10 years to reach terminal growth)

As a result, we estimate that the fair value of Fortinet is approximately $312.04 under current market conditions.

Wall Street’s Take

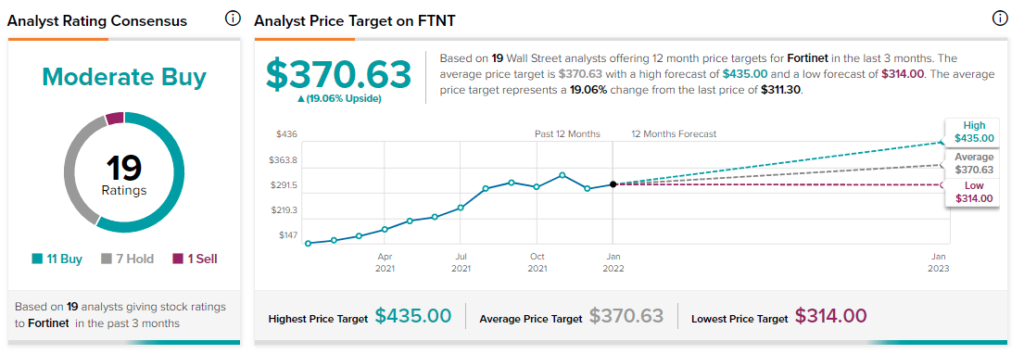

Turning to Wall Street, Fortinet has a Moderate Buy consensus rating, based on 11 Buys, seven Holds, and one Sell assigned in the past three months. The average Fortinet price target of $370.63 implies 19.1% upside potential.

Final Thoughts

Fortinet is a major player in a fast-growing industry. It is highly profitable and has many growth catalysts.

That said, it appears that the valuation might be a little stretched at the moment, if we assume it will reach its terminal growth rate in 10 years and if interest rates remain low. Since we expect rates to rise, we remain neutral on the stock.

Download the TipRanks mobile app now

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Read full Disclaimer & Disclosure