Facebook (FB) is no stranger to controversy. In 2019 alone it faced congressional hearings regarding data breaches, concerns over users’ privacy, regulatory issues concerning its proposed digital currency Libra, and a public outcry for allowing false claims in political ads. It managed to swat all these concerns away and only recently FB stock marched to a new all-time high.

But the movement to boycott ad spend on Facebook has intensified on account of an inadequate response to the use of hateful and misleading information on its platform. With more companies onboarding by the day, has the time of reckoning finally come for the all-conquering Like Generator? In a recent note to clients, Monness analyst Brian White ponders the boycott’s implications.

The 5-star analyst noted, “How long these boycotts last and the number of other companies that will join this movement are unknown. Facebook is a lightning rod for this issue… In our view, the longer this economic downturn lasts, the longer it will take for advertisers to return to Facebook… For the foreseeable future, we anticipate Facebook will struggle with weak digital ad spending trends and remain vulnerable to a deluge of negative media headlines.”

The pullback in ad spend has been a theme since the viral outbreak. Budgets were significantly slashed during the pandemic’s first wave in March. As COVID-19 cases continue to rise, the possibility of a further contraction to the economy amidst a partial shutdown could result in more ad spend reductions.

The combination of both COVID-19 and the boycott’s impact have led White to cut estimates for Facebook in 2020. White now expects revenue of $72.43 billion (down from $75.13 billion) and forecasts EPS of $6.03 instead of the previous $6.80.

However, in the long run, the 5-star analyst remains confident in the Facebook story. “Despite these setbacks,” concluded White, “We believe more people will become entrenched in the Facebook platform and society at large will shift toward more virtual interaction, including consumers, businesses and other organizations.” (To watch White’s track record, click here)

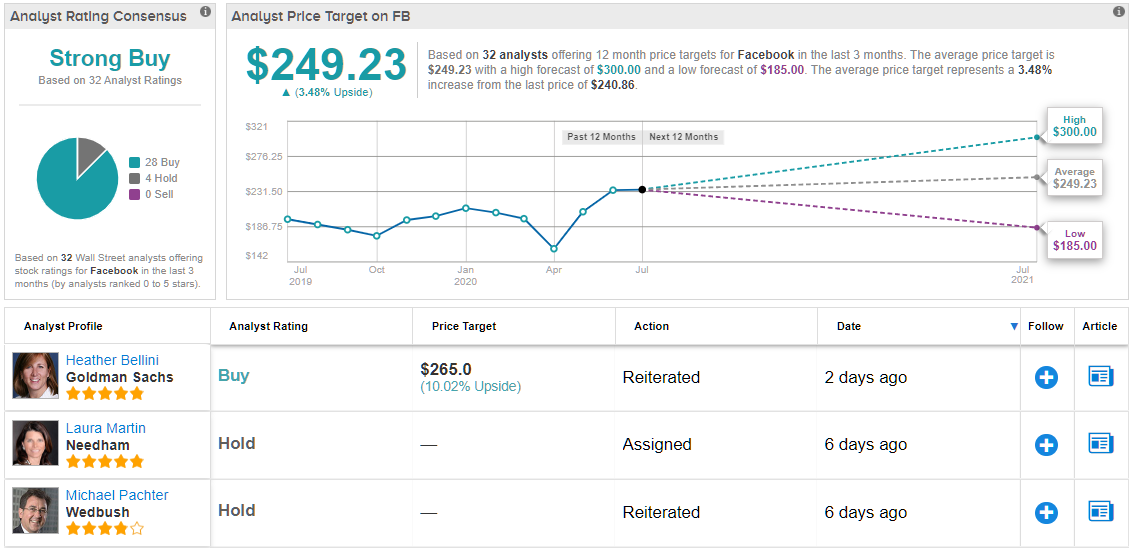

Overall, the rest of the Street still backs Facebook. 32 analysts have posted a review over the past 3 months, of which 3 say Hold, while all the rest recommend to Buy. However, the $249.23 average price target implies a modest upside in the shape of 3.5%. (See Facebook stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.