Following an unprecedented rise in 2020, U.S. e-commerce sales growth decelerated in 2021 as physical retail stores reopened their doors to customers.

Per the U.S. Department of Commerce, e-commerce sales increased 14.2% to $870.8 billion in 2021, compared to a growth rate of 31.8% in 2020. (E-commerce still accounted for 13.2% of overall U.S. retail sales in 2021, compared to 13.6% in 2020.)

Etsy (NASDAQ: ETSY) and Wayfair (NYSE: W) featured among the numerous e-commerce players that benefited from the accelerated shift to online shopping triggered by the COVID-19 pandemic.

However, these two stocks have significantly dropped from their 52-week highs, reflecting expectations of normalized growth rates in the business and a shift in investors’ focus to value stocks from growth stocks amid heightened stock market volatility.

Using the TipRanks stock comparison tool, we can stack Etsy up against Wayfair, and discuss what Wall Street analysts think about the prospects of these two e-commerce stocks.

Etsy

Online marketplace Etsy connects sellers of handmade and unique products with interested buyers. Aside, from Etsy.com, the company also operates Depop (fashion resale marketplace), Reverb (musical instrument marketplace), and Elo7 (Brazil-based handmade goods marketplace).

Etsy witnessed a phenomenal revenue growth rate of 111% in 2020, thanks to favorable pandemic-induced trends. As expected, the company’s growth rate slowed down in 2021, but was still impressive given the tough comparisons with the prior year. Revenue grew 35% to $2.33 billion in 2021, while EPS surged 26.4% to $3.40.

A strong holiday season helped Etsy crush analysts’ estimates for the fourth quarter of 2021. Fourth-quarter revenue grew 16.2% year-over-year to $717.1 million and EPS rose 2.8% to $1.11. Analysts predicted EPS of $0.78 on revenue of $684.66 million.

Stifel analyst Scott Devitt felt that Etsy’s Q4 results capped “an impressive year against a difficult comparison.”

However, the analyst noted that the company issued a subdued outlook for the first-quarter GMS (gross merchandise sales) and revenue due to headwinds following the reopening of the economy, fading e-commerce tailwinds, and tough comparisons.

Devitt also highlighted that the company continues to drive robust new buyer growth, and retain a healthy number of buyers gained during the pandemic.

Devitt reaffirmed a Buy rating on Etsy stock but slashed the price target to $200 (38.6% upside potential) from $230 to reflect his lowered growth estimates based on a slower start to this year.

Etsy announced a hike in its seller transaction fees from 5% to 6.5%, effective April 11. The company intends to invest most of the incremental revenue from this fee on marketing, seller tools, and enhancing customer experiences. It will be interesting to see how sellers respond to this hike over the upcoming quarters.

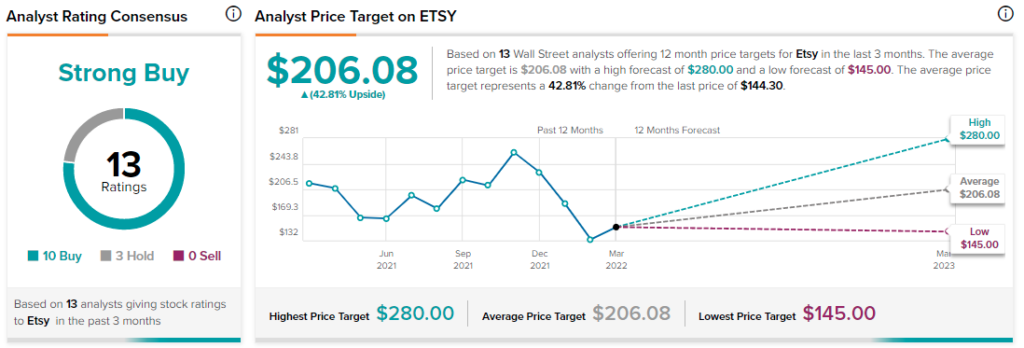

Overall, the Street’s sentiment on Etsy stock is bullish, with a Strong Buy consensus rating based on 10 Buys and three Holds. The average ETSY price target of $206.08 suggests 42.8% upside potential from current levels.

Wayfair

Online retailer Wayfair offers an extensive selection of furniture, decor, and home improvement products sourced from over 23,000 suppliers. It operates sites under the names Wayfair, Joss & Main, AllModern, Birch Lane, and Perigold, with each of these sites catering to a different target audience.

The surge in demand for home goods during the pandemic drove an impressive 55% jump in Wayfair’s 2020 revenue to $14.1 billion. However, after posting its first year of annual profits as a public company in 2020, the company swung back to losses last year, with revenue declining 3.1%.

Even the key holiday shopping season in the last quarter failed to drive Wayfair’s business, with the company reporting a wider-than-expected adjusted loss of $0.92 per share in the fourth quarter of 2021, compared to analysts’ forecast of a loss per share of $0.71. Wayfair had posted an adjusted EPS of $1.24 in the prior-year quarter.

Revenue plunged 11.4% to $3.25 billion, due to a decline in the number of customers as well as orders per customer.

On the positive side, Wayfair stated that the net revenue per active customer over the last 12 months increased 10.6% to $501.

Following the Q4 print, Wells Fargo analyst Zachary Fadem stated that he currently sees Wayfair as a “wrong stock in the wrong tape” amidst an increasingly challenging macro environment.

Fadem feels that inflation, supply chain woes, and difficult comparisons to pandemic-fueled numbers would limit near-term visibility.

While the analyst believes that Wayfair will inevitably return to growth and visibility would likely improve in the second half of the year, he finds the stock “increasing difficult to own amidst a ‘pandemic winner’ narrative that is poised to ‘give back’ over $1.5B in combined FY20/21 EBITDA.”

Consequently, Fadem lowered his price target to $110 (10.8% downside potential) from $195 and reiterated a Hold rating.

Wayfair is taking several initiatives, including continued investments in its logistics network, to capture additional business. The company is gearing up to open three brick-and-mortar retail stores this year in Massachusetts under its specialty brands, and a flagship Wayfair brand store in 2023.

Overall, analysts on the Street are sidelined on the stock, with a Hold consensus rating based on eight Buys, 11 Holds, and three Sells. The average Wayfair price target of $161.50 implies upside potential of 30.9% from current levels.

Conclusion

Etsy has fared better than Wayfair both in terms of sales and profitability growth even as the pandemic-fueled demand faded over recent quarters.

Given its strong execution and the Street’s bullish stance, Etsy seems to be a better e-commerce pick than Wayfair.

Download the TipRanks mobile app now.

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Read full Disclaimer & Disclosure