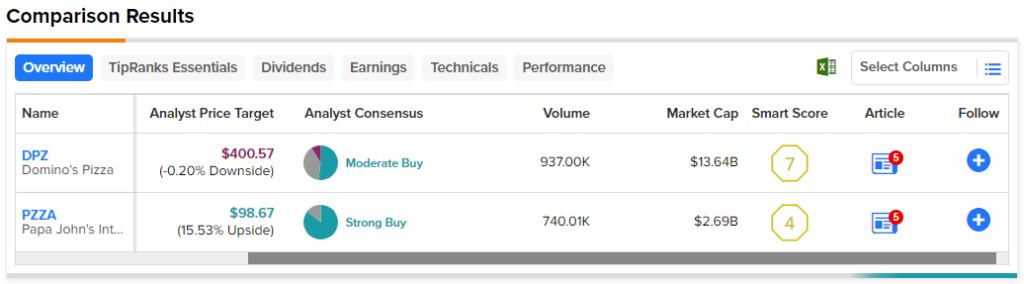

In this piece, I evaluated two pizza delivery stocks, Domino’s Pizza (NYSE:DPZ) and Papa John’s (NASDAQ:PZZA), using TipRanks’ comparison tool to determine which is better. Domino’s Pizza was founded in 1960 and now touts itself as “the largest pizza company in the world,” while Papa John’s was founded in 1984 and now operates over 5,000 locations in 45 countries and territories globally.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Despite their similarities, the stock-price action in these two pizza delivery chains is like night and day. Domino’s shares have rallied 14% year-to-date, and they’re up 4.1% over the last year. On the other hand, Papa John’s stock is flat year-to-date and down 0.8% over the last year.

The U.S. restaurant industry is trading at a price-to-earnings (P/E) multiple of 70.8 versus its three-year average of 33.8. The industry is also trading around its three-year average price-to-sales (P/S) ratio of 2.2. With that in mind, let’s analyze both stocks.

Domino’s Pizza (NYSE:DPZ)

At a P/E of 29.7 and a P/S of three, Domino’s valuation looks mixed — just like its latest earnings report. For comparison, the pizza delivery chain’s five-year mean P/E is 32, while its five-year mean P/S is 3.4. On the one hand, Domino’s sales and profit trends and long-term stock momentum are solid, but on the other, it has saddled itself with a massive debt load. Thus, a neutral view and a wait-and-see approach seem appropriate.

Domino’s has been somewhat volatile over the last few trading sessions following mixed earnings results. Earnings came in at $3.08 per share on $1.02 billion in sales for the second quarter versus the consensus of $3.05 per share on $1.07 billion in revenue. As the pizza chain’s per-share profits rose 9.2% year-over-year, its revenues tumbled 3.8%.

While Global Retail sales rose 5.8% in the quarter, U.S. same-store sales only rose 0.1%. The pizza chain did open a net 197 new stores globally, including 27 in the U.S. Unfortunately, delivery sales at U.S. locations open at least one year tumbled 3.5% year-over-year.

To combat driver shortages and other issues, the company recently announced a deal with Uber Eats. However, management is more interested in hiring more drivers directly in order to control the delivery experience.

Overall, Domino’s revenue and profit trends are solid despite the delivery issues, but a major concern is the $5.1 billion in net debt on its balance sheet. Only $556.4 million are current liabilities, but the situation is worth watching.

Finally, Domino’s pays a dividend yield of 1.2%, which isn’t spectacular but could make it worth holding for the long term as the investment story develops.

What is the Price Target for DPZ Stock?

Domino’s Pizza has a Moderate Buy consensus rating based on 13 Buys, nine Holds, and two Sell ratings assigned over the last three months. At $384.70, the average Domino’s Pizza stock price target implies downside potential of 4.15%.

Papa John’s (NASDAQ:PZZA)

Coming in with a P/E of 36.5 and a P/S of 1.3, Papa John’s is barely profitable, with ultra-thin net income margins ranging from 3% to 5% over the last few years despite its solid revenue trends. Additionally, Papa John’s net debt has been growing steadily. Thus, a bearish view seems appropriate.

For the first quarter, the company reported flat comparable-store sales in North America and a 3% decline in total revenues to $527 million, although total revenues were up slightly, excluding the impact of the refranchising of 90 restaurants last year.

Also, adjusted diluted earnings per share fell to 68 cents from 95 cents in the year-ago quarter, although Papa John’s also reported record system-wide sales of $1.24 billion. The company’s next earnings report is scheduled for August 3.

Unfortunately, Papa John’s has $969.9 million in net debt from the last 12 months, up from $760.9 million in 2022 and $614.9 million in 2021, signaling growing concerns. In fact, the company’s debt-to-equity ratio is negative, which often signals sizable risk because it means shareholder equity is negative and its liabilities exceed its assets.

Papa John’s does offer a dividend yield of 2.08%, which can be a factor in its negative debt-to-equity ratio. However, a holistic view suggests this company could be a risky bet.

What is the Price Target for PZZA Stock?

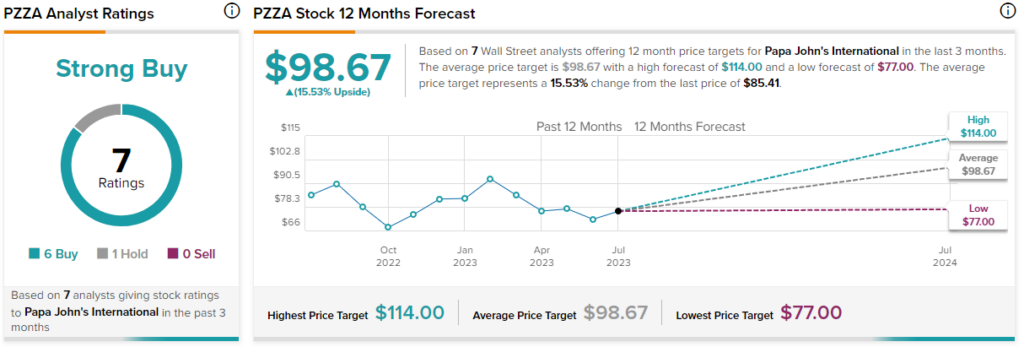

Papa John’s has a Strong Buy consensus rating based on six Buys, one Hold, and zero Sell ratings assigned over the last three months. At $98.67, the average Papa John’s stock price target implies upside potential of 15.5%.

Conclusion: Neutral on DPZ, Bearish on PZZA

Overall, Domino’s and Papa John’s both carry significant amounts of net debt, but Domino’s sales and profit trends are far better than those of the barely-profitable Papa John’s. Thus, Domino’s is the clear winner, although a wait-and-see approach may be best in light of its current valuation.