Building up a strong portfolio requires a sharp eye for bargains. Investors have to know how to find the right stocks, at the right price – i.e. shares that are priced relatively low, but have sound prospects for sustained growth. In other words, to learn how to shop effectively at the discount racks of the equity world.

Indeed, there are wide range of reasons that share prices can be down, ranging from simple bad luck to fundamental issues with the company. It’s okay to buy a stock that has simply taken a beating due to market conditions – but it’s best to avoid stocks that have earned their low prices. The trick is learning to spot the difference.

Identifying stocks that feature both low share prices and solid fundamentals relies on both reliable data and sound judgement. Using the TipRanks platform, we’ve found two of these stocks, each down more than 60% this year, that are worth a closer look. A number of Wall Street analysts say that we should expect them to rebound in 2025 – let’s give them a closer look to find out why.

Quanterix (QTRX)

We’ll start in the field of life sciences with Quanterix. The company is working to digitize biomarker analysis, with a stated objective of improving the “science of precision health.” Quanterix publicizes that its technology can support “earlier disease detection, better prognosis and precise treatment methods.” The company works in the fields of oncology, neurology, cardiology, inflammation and infectious diseases.

Using its proprietary Simoa technology, Quanterix has created a commercial brand, Lucent Diagnostics, that is designed to support the earlier detection of cognitive diseases. This class of disease is difficult to diagnose, especially early, but early diagnosis is imperative, as treatments are also difficult – and are more effective when started earlier.

Earlier this month, Quanterix announced that it will acquire Emission, a smaller peer in the field of immunoassay testing. The transaction is expected to close in January of 2025, and will cost Quanterix as much as $70 million. Of that total, $10 million will be paid up front, $10 million on ‘completion of certain technical milestones,’ and as much as $50 million will be contingent on meeting certain performance milestones. The deal is expected to be accretive to revenues starting in 2026. Quanterix is said to be using cash on hand for the initial payments.

Turning to financial results, we find that Quanterix had a loss of -$11.2 million in Q3 2024. The company registered this net loss even as revenues marked the sixth quarter in a row of double-digit growth. The company’s top line in 3Q24 came to $35.7 million, up 13% year-over-year and a cool $1.5 million above forecasts. And yet, this didn’t provide much of a bump, and in fact share prices have sunk lower in the month and a half since the Q3 print. All told, Quanterix is down 61.5% this year.

Covering this stock for Canaccord Genuity, analyst Kyle Mikson describes the shares as undervalued. Looking ahead, he sees the company’s continued development of new products, and its expansion of the Lucent brand, as accretive, and writes, “We continue to view the stock as undervalued following the company’s consistent execution in 3Q24, recognizing the financial contribution from diagnostics may be immaterial in the relative near term… The company remains on track to launch 20 new assays in 2024, and Quanterix appears poised to announce a new higher multiplex protein detection platform in 2025. The company’s LucentAD Complete multi-analyte test for Alzheimer’s Disease (AD) detection appears promising as well. Although capital constraints could impact QTRX’s near-term performance, we believe the company should benefit from multiple factors that should drive double-digit revenue growth and help boost the shares over time.”

This translates to a Buy rating for the stock, and Mikson’s $20 price target implies a one-year upside potential of 90%. (To watch Mikson’s track record, click here)

While there are only 4 recent analyst reviews for this stock, with 3 Buys and 1 Hold, QTRX enjoys a Strong Buy consensus rating. The stock is currently trading for $10.52 and the average price target, $22.25 – even more bullish than Mikson’s – would translate into gains of 111.5% next year. (See QTRX stock forecast)

Green Plains, Inc. (GPRE)

The second company we’ll look at, Green Plains, works in bio-refining, as a developer and producer of biofuels. This is a low-carbon alternative to fossil fuels, used to power existing transportation technologies—meaning it’s added to vehicle fuel mixtures—while bringing the advantage of reduced pollutant emissions. Green Plains is a major producer of low-carbon biofuels. By the numbers, the company has 10 biorefinery facilities in the US, processing 300 million bushels of corn annually and boasting a capacity to produce one billion gallons of biofuel every year, along with 290 million pounds of renewable corn oil and 2.5 million tons of distillers grains.

While biofuels may be the most prominent part of Green Plains’ product line-up, it is still only part of the whole. The company also produces proteins and ingredients found in pet foods; renewable corn oils as feedstock for biofuel refining; and a range of glucose and dextrose syrups for use in fermentation and catalytic conversion. The company also operates a comprehensive transportation and logistics segment, which includes storage for grain and biofuels, fuel terminal facilities, and fuel transport services. The company has 32 storage facilities capable of holding approximately 32 million gallons of biofuel and is equipped to load both railcars and tanker trucks. The company leases a railcar fleet with a capacity to move 75 million gallons in aggregate.

Green Plains is based out of Omaha, Nebraska, in the heart of North America’s richest corn-growing region. The company’s 10 biofuel refining facilities are located in Indiana, Illinois, Iowa, Minnesota, Nebraska, Tennessee, and Texas.

The company’s financial results in the last reported quarter, 3Q24, showed a swing and a miss on revenue even as earnings beat expectations. The company’s top-line, $658.7 million, was down 26% year-over-year and came in $8.2 million below the forecast; the bottom-line earnings, at 69 cents per share, were 57 cents per share better than expected. We should note here that GPRE shares are down 63% so far this year.

Truist analyst Jordan Levy covers this stock, and in his view, the company is beginning an acceleration toward stronger performance. Levy writes of GPRE, “Following some operational hurdles earlier this year, GPRE began to hit its stride in 3Q amidst a much improved quarterly crush spread environment as seen by solid plant utilization & product yields. While we expect EBITDA to step down in 4Q as crush spreads have recently contracted, the most important factors for GPRE shares at this point in the story are demonstrating consistent operations & showing progress on Sequence sales, CST ramp, and (perhaps most importantly near-term) Nebraska CCUS.”

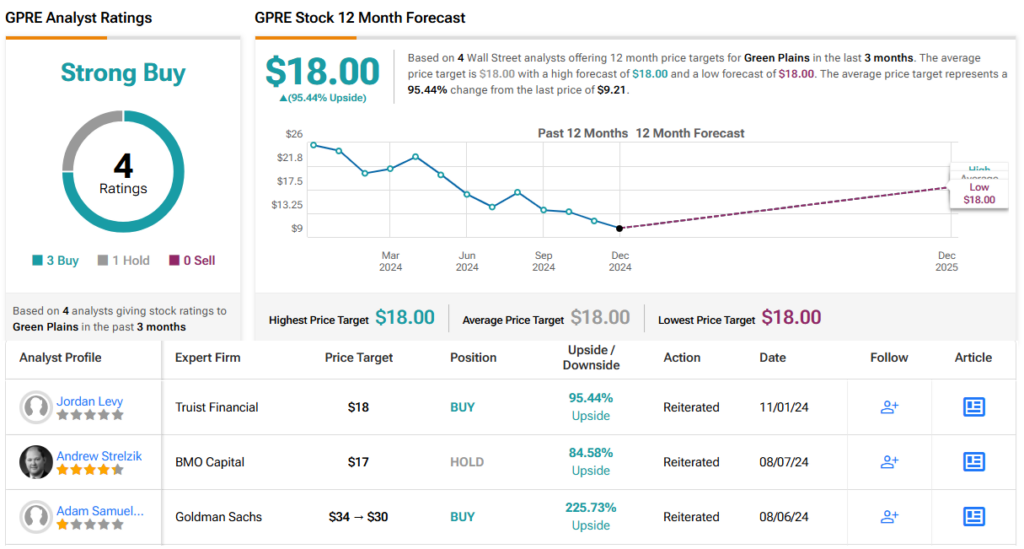

These comments support Levy’s Buy rating on Green Plains, while his $18 price target indicates his belief in a 95% upside for the coming year. (To watch Levy’s track record, click here)

This is another stock with 4 recent analyst reviews, also with 3 Buys and 1 Hold. GPRE has an average 12-month price target of $18, matching the Truist view, which would be good for gains of 95%. (See GPRE stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.