Ford (F) stock may not be the market’s star performer lately, but there’s something undeniable about a dependable automaker offering a 7.6% dividend yield in today’s speculative environment. With yields tightening marketwide, Ford’s robust performance warrants a closer look at this legacy automaker. The stock has been hovering under $10 for quite some time, with a potential investment opportunity now on the cards for both value and growth investors. The good news is that Ford’s hefty dividend payout could finally be supplemented by significant price gains in 2025.

Given the confluence of market and internal factors, Ford stock is an intriguing option for investors seeking a blend of income and potential growth.

A Sluggish Stock That Pays While You Wait

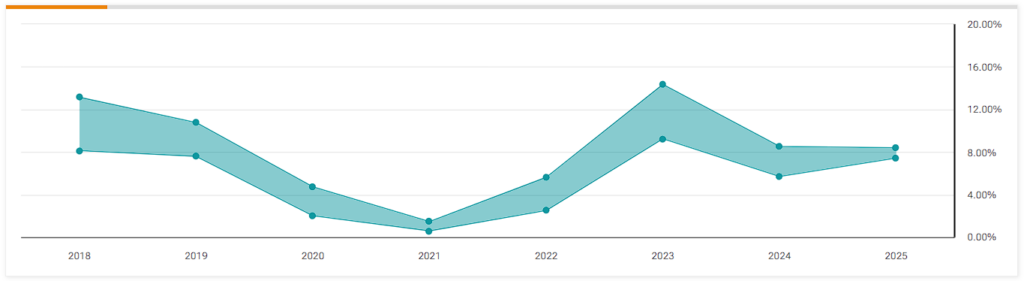

Ford’s stock price performance has been overshadowed by its dividend package. Ford’s 7.6% dividend yield follows several years of lackluster share performance. Since 2022, Ford stock is down 24% and down 12% since March 2024. However, the stock has found some support and is trading 3% higher so far this year.

Even with analysts expecting EPS to fall by about 25% to ~$1.37 this year, primarily due to industry-wide cost pressures and Ford’s restructuring plans, the dividend run rate of $0.75 looks well-covered. So, unless the company’s outlook drastically changes, there’s little reason to fear a dividend cut, considering how stable Ford’s dividend payments have been in the post-pandemic era. Ford declared a regular dividend of $0.15 per share and a supplemental dividend of $0.15 per share in its Q4 earnings call.

As investors may already be aware, the auto industry is suffering. Manufacturers are struggling with the ongoing transition to EVs while still contending with chip shortages, inflationary forces, and supply chain hiccups that reared their heads in 2020. In this turmoil, Ford’s strategy to simplify operations, lean into its strengths, and diversify its powertrain offerings stands out as more balanced than some of its peers.

Quiet Successes Go Overlooked

Between the headlines on Ford’s share price swings and the broader debate over its pivot to electric vehicles, it’s too easy to get lost in the noise. Yet beneath that noisy surface, Ford is quietly ticking some important boxes.

First, leadership has been working hard on cutting costs. The recent layoffs in Europe are part of a bigger effort to tighten up operations worldwide. Sure, job cuts are never great, but if we are honest, they show Ford is serious about keeping its margins strong and ensuring the core business stays solid.

Equally noteworthy is Ford Pro, the company’s commercial vehicle segment, which many analysts see as a hidden gem. In 2024, Ford Pro revenue climbed 15% to $67 billion, a solid figure in a landscape where many still question how traditional automakers will adapt. The real plus here is the software subscription component, a rare in the automotive space, which provides recurring revenue, smoothing out some of the cyclical bumps the industry typically faces. In total, Ford achieved revenue of $185 billion in 2024, marking the fourth consecutive year of top-line growth.

Meanwhile, on the EV front, I like how Ford isn’t sprinting to catch Tesla at all costs. Instead, it’s focusing on a multi-powertrain strategy that includes hybrids, EVs, and traditional ICE cars. Some find this conservative approach rather boring compared to the all-in fervor of EV startups, but I think it leaves Ford less exposed to demand shocks for EVs in the near term while still setting the stage for growth as the EV market develops.

Analysts Expect a Brighter Future for Ford

Ford’s earnings will likely decline this year. However, looking further ahead, the consensus on Wall Street points to an upswing. Analysts now predict EPS to rise to $1.65 in 2026 and $1.82 in 2027, reversing any temporary dips. With an implied P/E ratio of around 6x, Ford trades at a notable discount to historical averages and to its peers in the auto sector.

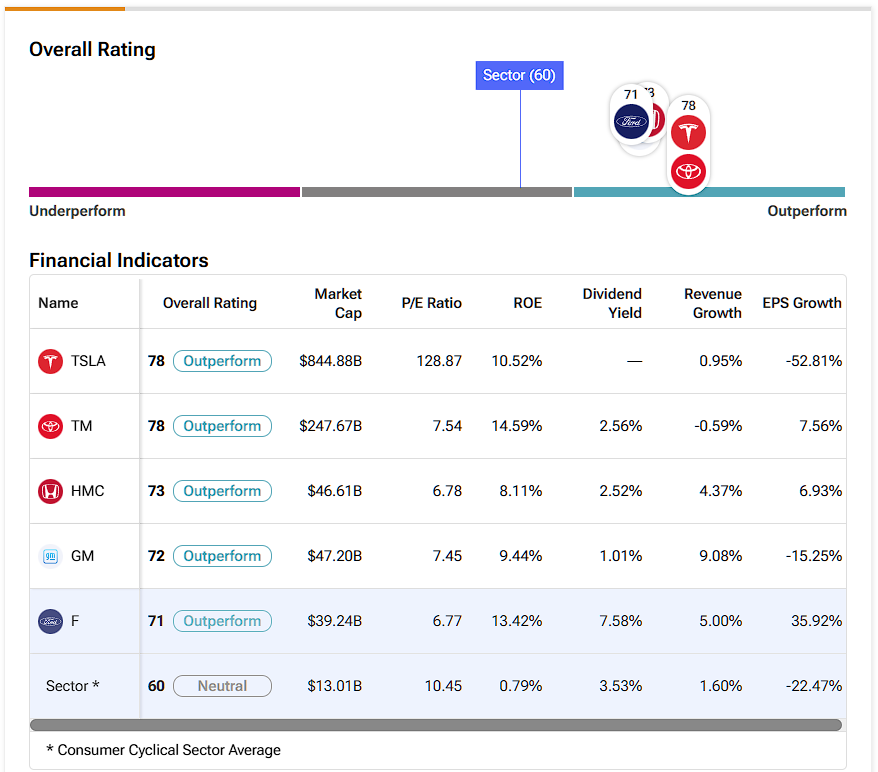

Beyond Ford’s dividend, the upside potential is that this discount could narrow if Ford delivers on its cost-cutting targets, maintains its enviable foothold in pickup trucks and commercial fleets, and continues to adapt in the EV and hybrid spaces. Remember that the auto industry is fiercely competitive, with General Motors (GM) now rolling out its own EV lineup, Tesla (TSLA) dominating in electric vehicles, and other emerging players like Rivian (RIVN) applying further pressure. And yet, Ford’s brand strength, dealer network, and prudent approach to evolution are the weapons for its comeback.

What is Ford’s Price Target?

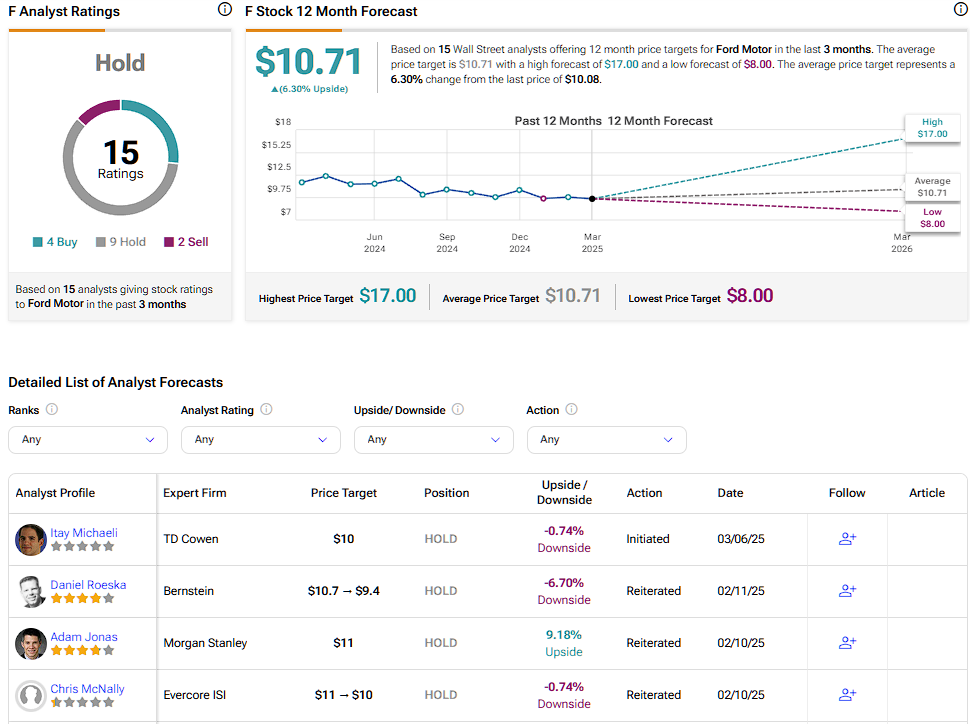

Despite its compelling dividend case, Wall Street remains uncertain about Ford’s stock. As things stand, the stock carries a Hold consensus rating based on four Buy, nine Hold, and two Sell ratings over the past three months. Ford’s average price target of $10.71 per share implies a 6.3% upside potential over the next twelve months.

A Dividend Stock Set for a Bounce

For income-oriented investors, Ford’s 7.6% yield is a standout in a market where high-yield, reliable dividends are scarce. More appealing still is that you’re not stuck holding a stock without growth prospects. Ford is actively retooling its business for the future, keeping a foot in the EV door without abandoning the profitable gas and hybrid segments that pay the bills (and dividends) today. With EVs still a relatively niche market, how long-term EV sales develop is still uncertain. Several EV front-runners could find themselves headed in the wrong direction as industry standards are established for the first time. In hindsight, Ford’s reluctance to jump two-feet-first into EVs could prove to be a masterstroke.