Since the onset of 2022, companies in the U.S. airline industry have been facing headwinds from high fuel prices, the Ukraine-Russia war, and the economic slowdown in the country. However, not everything looks gloomy, as they are benefiting from healthy demand for leisure and business traveling. In this article, we will talk about three airline companies that have healthy prospects. These companies are: Delta Airlines, Inc. (NYSE:DAL), United Airlines Holdings, Inc. (NASDAQ:UAL), and Southwest Airlines Co. (NYSE:LUV).

Using the TipRanks Stock comparison tool, we have designed a consolidated chart of the abovementioned industry players. This chart would help us understand which among the three chosen players could be a better buy option for prospective investors.

Delta Airlines, Inc. (NYSE:DAL)

Georgia-based Delta Airlines engages in the air transportation of cargo and passengers. The $21.4-billion company operates from >275 destinations across six continents. Its global and domestic networks, efforts to boost customers’ loyalty, constant evaluation of its fleet, and growth in traveling demand are a boon.

In July, the company’s President, Glen Hauenstein, said, “With sustained strength in bookings, we expect September quarter revenue to be up 1 to 5 percent compared to 2019 with total unit revenue growth improving sequentially.”

In addition to the revenue growth, the company forecasts operating margin to be within the 11%-13% range. Fuel price is expected to range from $3.45 to $3.60 per gallon. By 2024, Delta Airlines forecasts total revenues (adjusted) to be >$50 billion, earnings per share (adjusted) to be >$7, and free cash flow to exceed $4 billion.

Is Delta Airlines a Buy, Sell or Hold?

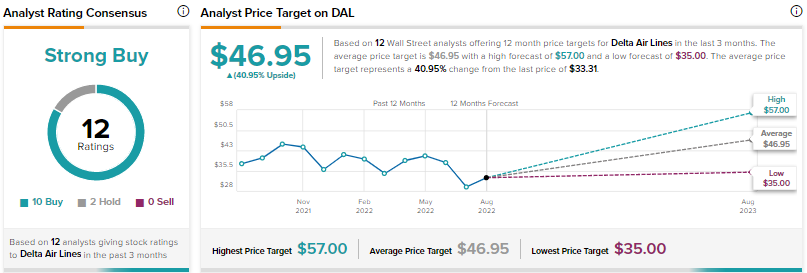

On TipRanks, analysts are unanimously optimistic about the prospects of Delta Airlines, which commands a Strong Buy consensus rating based on 10 Buys and two Holds. Also, DAL’s average price forecast of $46.95 suggests 40.95% upside from the current level. Year-to-date, shares of Delta Airlines have declined 17.3%.

In addition to this, financial bloggers are 79% Bullish on DAL stock versus the sector average of 67%. Further, hedge funds are Very Positive about the stock, evident from the increase in their holdings by 4.7 million shares in the last quarter.

United Airlines Holdings, Inc. (NASDAQ:UAL)

The $12.2-billion company is another important air transportation service provider in the United States and internationally, including Africa, the Middle East, and the Pacific. The company is well-positioned to benefit from its national advertising campaigns, diversified geographical reach, improved international networks (especially in transpacific destinations), and partnerships.

However, the company is exposed to headwinds prevalent in the industry. In July, the company’s CEO, Scott Kirby, said, “…we must confront three risks that could grow over the next 6-18 months. Industry-wide operational challenges that limit the system’s capacity, record fuel prices and the increasing possibility of a global recession are each real challenges that we are already addressing.”

For the third quarter of 2022, the Illinois-based company forecasts revenues to grow by 11% from the comparable period in 2019. Also, the company expects the pre-tax margin (adjusted) to be 9% in 2023.

Is United Airlines a Good Stock to Buy?

As of now, analysts have mixed feelings about UAL stock. Based on five Buys, five holds, and one Sell, the stock carries a Moderate Buy consensus rating, as per TipRanks. UAL’s average price target of $47.60 mirrors upside potential of 27.31% from the current level. Shares of the company have declined 17.8% since the beginning of 2022.

Meanwhile, financial bloggers are 85% Bullish on UAL versus the sector average of 67%. However, sentiments of hedge funds are Very Negative about UAL. They have disposed nearly 2.5 million shares of United Airlines in the last quarter.

Southwest Airlines Co. (NYSE:LUV)

The Texas-based passenger airlines service provider operates in 11 countries and from 121 airports globally. Expansion of its network worldwide, further improvement in services to boost customers, and fleet modernization are the company’s strategic priorities. Its hedging program against a hike in fuel prices is a boon for this $22.4-billion company.

In July, the company’s CEO, Bob Jordan, opined that “inflationary pressures and headwinds from operating at suboptimal productivity levels” will “continue in second half 2022”. However, the CEO believes that fuel hedges will provide “significant protection against higher jet fuel prices” in the quarters ahead.

“…we expect to be solidly profitable for the remaining two quarters of this year, and for full year 2022,” Jordan added.

For the third quarter of 2022, the company anticipates revenues to grow 8%-12% versus the 2019 levels. Fuel cost is predicted to be within the $3.25-$3.35 per gallon range.

Is Southwest Airlines Stock a Buy or Sell?

Considering the company’s growth prospects, South Airlines appears to be a good stock to Buy. Its story is underpinned by analysts’ optimism about the prospects of Southwest Airlines. They have a Strong Buy consensus rating on LUV stock, which is based on 11 Buys and three Holds.

LUV’s average price forecast of $51.23 represents upside potential of 35.53% from the current level. Year-to-date, shares of LUV have declined 14.1%.

Financial bloggers are 91% Bullish on LUV versus the sector average of 67%. However, hedge funds have a Negative stance on the stock. In the last quarter, they lowered their holdings in LUV by 418.5 thousand shares.

Concluding Remarks

According to the Federal Aviation Administration, growth in domestic passengers to U.S. airlines is expected to be 4.9% annually from 2021 to 2041. Based on strong industry fundamentals and their strategic initiatives, the long-term prospects of the companies mentioned above appear solid. Also, each company is trying to overcome the near-term industry hurdles in its own way.

By comparing analysts’ consensus ratings and hedge fund signals, DAL and LUV appear to be better investment options than UAL at present. Finally, by comparing the hedge fund signal, Smart Score ratings, and price target upside of DAL and LUV, Delta Airlines appears to be a better Buy.

Read full Disclosure