Shares of cybersecurity firm CrowdStrike (NASDAQ: CRWD) have risen 11.7% year-to-date and have outperformed the broader market.

Maximize Your Portfolio with Data Driven Insights:

- Leverage the power of TipRanks' Smart Score, a data-driven tool to help you uncover top performing stocks and make informed investment decisions.

- Monitor your stock picks and compare them to top Wall Street Analysts' recommendations with Your Smart Portfolio

Through its cloud-native Falcon platform, CrowdStrike offers products and solutions for the protection of endpoints, cloud workloads, identity, and data.

CrowdStrike is growing rapidly backed by the huge demand for cybersecurity amid an increase in ransomware and other cyber attacks. Also, concerns over the hacking of government organizations and large corporations have increased amid the ongoing Russia-Ukraine conflict.

Impressive Growth

CrowdStrike’s FY22 (ended January 31, 2022) revenue increased 66% to $1.45 billion, with subscription revenue rising 69%. Annual recurring revenue (ARR) rose 65% to $1.73 billion, and the company ended FY22 with 16,325 subscription customers (also up 65%). Adjusted EPS surged 148% to $0.67 in FY22.

Further, the company is experiencing higher acceptance of its products among customers. As of FY22 end, the proportion of subscription customers who adopted four or more modules grew to 69% from 63% at FY21 end.

Looking ahead, CrowdStrike expects FY23 revenue between $2.133 billion-$2.163 billion and adjusted EPS in the range of $1.03-$1.13.

Wall Street’s Take

In a research note to investors, Goldman Sachs analyst Brian Essex highlighted that with its strong execution, CrowdStrike has delivered continued improvements to its fundamentals amid an unprecedented demand backdrop.

Essex feels that the company is “well positioned in the sweet spot of demand ahead of accelerating deterioration of the threat environment with Endpoint expected to remain a top CIO priority within Security.”

Essex upgraded CrowdStrike to a Buy from a Hold, citing a compelling valuation, solid secular demand trends, and a robust outlook. Essex raised the price target for CRWD stock to $285 from $241.

This week, Jefferies analyst Joseph Gallo initiated coverage of CrowdStrike with a Buy rating and a price target of $275.

Gallo believes that the company is a “category winner” given its high enterprise renewal rates, solid gross margin, and an addressable market capable of sustaining hypergrowth for years.

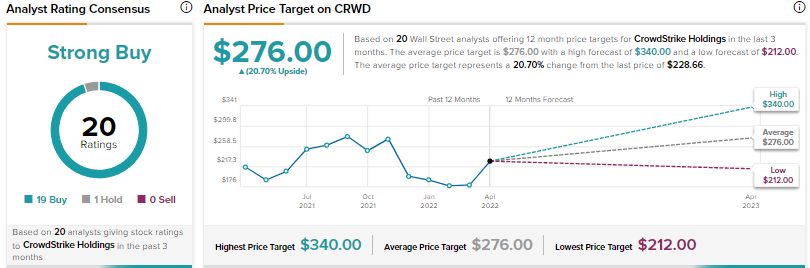

Overall, CrowdStrike scores a Strong Buy consensus rating based on 19 Buys and one Hold. The average CrowdStrike price target of $276 implies 20.70% upside potential from current levels.

Conclusion

CrowdStrike’s strong execution will help it capture additional business in the cybersecurity space. The company now sees a potential total addressable market of $116 billion by 2025 as more companies are embracing digital transformation, and the risks of cyber attacks are increasing at an alarming pace.

Further, TipRanks data shows that financial blogger opinions are 87% Bullish on CrowdStrike, compared to a sector average of 68%.

Discover new investment ideas with data you can trust.

Read full Disclaimer & Disclosure.