Britain’s housing market has remained robust through the pandemic and into 2022 – so we have compared two leading British builders Persimmon (GB:PSN) and Redrow (GB:RDW) that are currently surfing a wave of high house prices (although facing challenges relating to supply).

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

We have used the TipRanks’ Comparison tool to compare these two stocks on different parameters. This tool helps investors to make informed decisions by comparing different stocks in various aspects.

Persimmon’s share prices are not in good shape and are trading down by 28% in the last year – by comparison Redrow’s shares are down by just 6.5% in the last year.

Both companies have dividend yields higher than the sector average of 1.65%.

Let’s look at the stocks in detail.

Persimmon

Persimmon builds houses in the UK under the brand’s Persimmon, Charles Church, and Westbury Partnerships. The Persimmon brand contributes the most to the group’s revenue, and it focuses on traditional housing at affordable prices.

The company recently posted its trading update ahead of its interim results, which are due on August 17, 2022. It completed 6,652 homes in the first half, below expectations mainly due to supply disruptions such as labour and material shortages. Total revenues were also slightly down at £1.69 billion compared to £1.84 billion last year.

The company is currently enjoying higher gross margins as a result of higher home prices. Based on this, the company is expecting its half-year’s profit to be above expectations.

For financial year 2022, the company expects to deliver around 15,000 homes.

The company’s forward sales are solid at £1.87 Billion with around 8,000 homes already booked, a comfortable situation for the company as it is 75% forward-sold for the year.

Laura Hoy from Hargreaves Lansdown said, “The good news is that demand showed no signs of slowing, with the average house price continuing to climb and a strong forward sales position. That should be enough to prop up profits with management guiding for a slight beat at the half year.”

Persimmon’s highlight is its dividend yield of 12.47%. This stock is currently beating Britain’s inflation rate. The company paid a 110p per share dividend in July, which was announced in April 2022.

View from the City

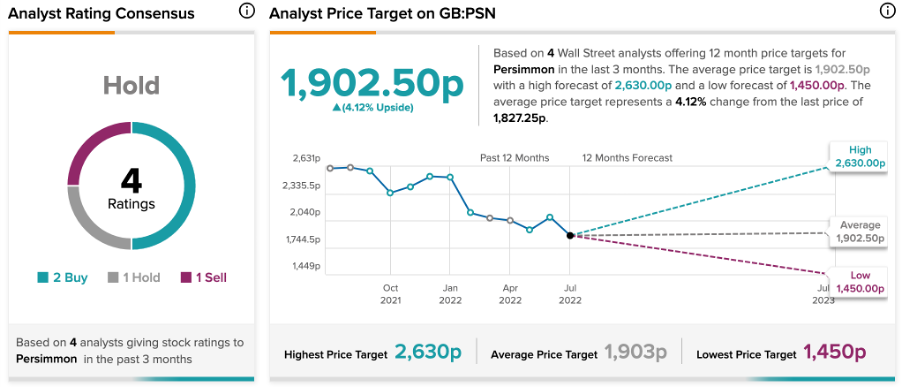

According to TipRanks’ analyst rating consensus, Persimmon stock has a Hold rating based on four analyst ratings. It has two Buy, one Hold, and one sell recommendations.

The average price target is 1902.5p, which is 4.1% higher than the current price. The stock price has a high forecast of 2,630p and a low forecast of 1,450p.

Redrow

Redrow is a residential property builder, delivering high-quality and premium houses across the UK.

In its last interim results announced in February 2022, Redrow posted a profit before tax of £203 Million, which was increased by 17%. This came alongside an operating margin of 19.5%, which is similar to 2019 levels. The company expects to maintain a similar level of margins for the 2022 financial year.

The company also witnessed a strong demand for its houses and posted record revenue of £1 billion. The average selling price increased by 8%.

Last month, the company started a share buyback worth £100 Million at 10.5p per share.

As a result of solid performance, the company paid an interim dividend of 10.0p per share in April 2022, up 67% from the previous year.

Aynsley Lammin, an analyst at Investec said, “The figures exceeded expectations. A good set of interim results, with progress on margins being better than we expected. The group has essentially reached its normalised margins a year early.”

View from the City

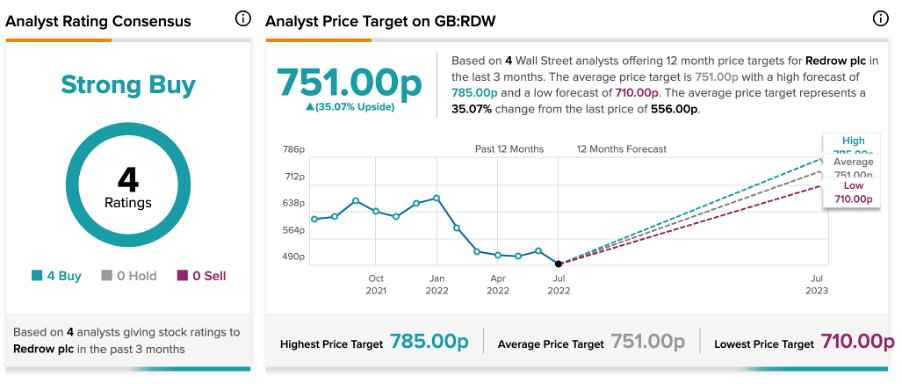

According to TipRanks’ analyst rating consensus, Redrow stock has a Strong Buy rating, based on four Buys.

The average price target is 751.0p, with an upside potential of 35.0%. The high and low forecasts for the price are 785p and 710p, respectively.

Conclusion

The demand for houses across the UK remains strong, with the quality of customers improving along with very low cancellation rates. The long-term prospects of the sector are promising, which makes both these stocks suitable for investment.

Over the coming months, maintaining supply will be a challenge for these companies.