It has not been a vintage year for Constellation Brands (STZ). The shares might be on course to see out the year 6% into the green, but those returns pale in comparison to the S&P 500’s impressive 24% gain.

Don't Miss Our Christmas Offers:

- Discover the latest stocks recommended by top Wall Street analysts, all in one place with Analyst Top Stocks

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

Yet, heading into the drinks giant’s third quarter of fiscal 2024 results (January 5), Goldman Sachs’ Bonnie Herzog thinks the report could come in stronger-than-expected. “We see a positive risk/reward ahead of 3FQ24 results given good visibility on the quarter based on comments by STZ’s CFO at a recent conference,” the analyst explained. “We see a good chance for an FQ3 EPS beat given relatively low buyside expectations, especially on beer shipments due to a timing factor that should broadly get sorted in FQ4.”

Given the above, Herzog has been making some tweaks to her estimates. While FQ3 beer shipment/depletion expectations are lowered from the prior 5.1%/6.5% to 3.5%/6.0% (vs. consensus at 4.0%/6.1%), the FQ4 forecast is raised to 6.0%/6.5% compared to 4.4%/6.0% beforehand. The Street has 6.4%/6.8%.

There’s also a slight reduction to top-line expectations, with Herzog calling for net sales growth of 5.8% (vs 7.0% previously, yet still better than Visible Alpha Consensus Data at 4.7%). It’s a similar story for the bottom-line, with the FQ3 EPS estimate lowered by $0.03 to $3.10 (ex Canopy), but again still above the consensus forecast of $3.07.

As for the FY24 outlook, Herzog anticipates the company will stick to its FY24 beer guide, which factors in net sales growth of 8-9%, right toward the “higher end of their long-term algorithm and 1-2% pricing.”

The analyst also sees management keeping its beer operating margin guide at roughly 38%. While that accounts for continued “inflationary pressures & higher depreciation,” and is a little below the company’s medium-term range of 39-40%, compared to the wider industry, the margin is still “best-in-class.”

In fact, looking at the wider picture, Herzog remains fully convinced in the Constellation story and thinks investors should take advantage of a clear opportunity at play here. “We continue to see enough momentum in STZ’s business to deliver attractive growth driven by its core beer brands led by Modelo based on our state-by-state distribution analysis,” Herzog said. “With the stock trading at an 8% discount to the market vs its 5-year historical 8.5% premium based on a CY24 P/E multiple of 18.0x on consensus estimates, we continue to see an attractive entry point for investors especially considering its top-tier volume driven topline growth and best-in-class beer op margins with a clear path to 39-40% (including meaningful progress on margin expansion next year).”

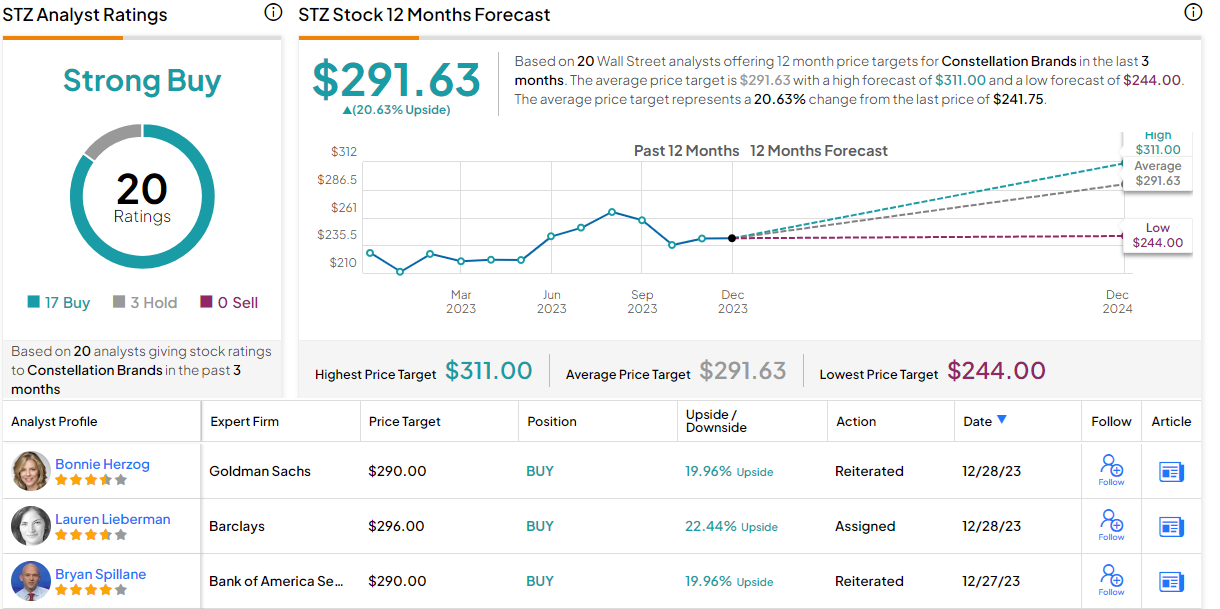

Accordingly, STZ remains one of Herzog’s “top stock picks,” with the analyst reiterating a Buy rating backed by a $290 price target. There’s potential upside of 20% from current levels. (To watch Herzog’s track record, click here)

Most analysts agree with that assessment. The stock claims a Strong Buy consensus rating, based on a mix of 17 Buys and 3 Holds. The $291.63 average target is only slightly higher than Herzog’s objective. (See Constellation Brands stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.