Cirrus Logic (CRUS) stock has been an under-performer year-to-date. The stock is down 6.4%, while the semiconductor industry is up 12.22%. CRUS’ underperformance is likely due to investors losing patience with the company’s growth plans.

Invest with Confidence:

- Follow TipRanks' Top Wall Street Analysts to uncover their success rate and average return.

- Join thousands of data-driven investors – Build your Smart Portfolio for personalized insights.

CRUS released its Q1 2022 results at the end of July, and its operating profit margin, both GAAP and non-GAAP, had declined year-over-year. On the earnings call, management stated that they expect supply constraints to push their gross margins below the company’s target of 50%.

Thanks to this impatience, CRUS is turning into a value play. With a market cap of 4.5 billion and FY 2021 revenue of 1.37 B, it has a P/S ratio of 3.23 and a P/B ratio of 3.22. (See Cirrus Logic stock charts on TipRanks)

Growth Prospects

Based on the Q1 2022 earnings presentation, CRUS is targeting the High- Performance Mixed-Signal segment for growth. According to company estimates, this segment was a $435 million market in 2020, but by 2025, it is expected to be a $3.5B market.

This market is expected to grow dramatically due to smartphones upgrading to better quality audio. CRUS is in an ideal position to capitalize on this growth, due to having a high market share in supplying semiconductors to the top seven smartphone OEMs (original equipment manufacturers).

As of 2021, 19% of CRUS’s revenue came from the High Performance Mixed-Signal segment. If this market grows as expected and CRUS maintains its market share of 54%, revenues by 2025 could be close to $3 billion.

For this segment to grow from 435 million to 3.5 billion by 2025 means the CAGR will be 51.75%. From a revenue perspective, that means High-Performance Mixed-Signal products should account for 30% or more of revenue in 2022 and by 2024 over 50% of revenue.

Some of these factors, like the growth of the High-Performance Mixed-Signal market, remain out of CRUS’s control and highly depend on smartphone production.

TipRanks’ Analyst Rating

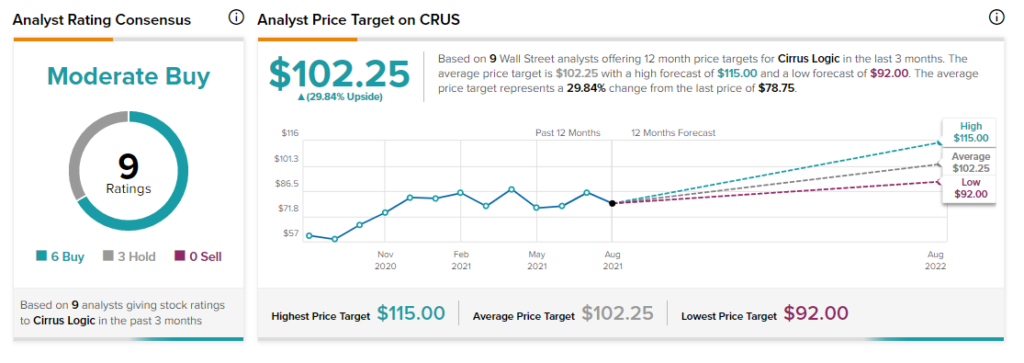

The TipRanks analyst rating has CRUS as a Moderate Buy. 6 analysts give CRUS a Buy rating, and 3 analysts give it a Hold rating. The average Cirrus Logic price target is $102.25, representing a 29.8% upside, based on the last price of $78.75. The lowest price target is $92, which represents an upside of 16.8%.

Among semiconductor competitors in the audio space, CRUS presents the most upside, including when considering the lowest price targets.

Conclusion

The company grew revenue year-over-year by 14% in Q1 2022, and management is forecasting Q2 revenue will grow by 29.7% year-over-year.

On the High-Performance Mixed-Signal side, revenue for the quarter grew 65.8% year-over-year, while revenue from other audio products grew by 5.2%.

It seems CRUS’ strategy of focusing on the High-Performance Mixed-Signal has already begun to bear fruit. Investors will do well to monitor smartphone product from the main OEMs, as their sales will have an enormous influence on how well CRUS does over the coming years.

The potential upside for CRUS for the rest of 2021 and into the future makes it a hard- to-ignore stock. The low valuation it has sunk to after the Q1 earnings results minimizes the downside risk. This may be the best time to weigh getting exposure to CRUS.

Disclosure: Joshua Sorto does not own shares of Cirrus Logic.

Disclaimer: The information contained herein is for informational purposes only. Nothing in this article should be taken as a solicitation to purchase or sell securities.