ChargePoint Holdings, Inc. (CHPT), an emerging electric vehicle (EV) charging network provider, is scheduled to release its fourth-quarter and full-year 2022 earnings results and guidance early next month on March 02, 2022. CHPT stock has declined 30% so far this year but Wall Street analysts remain bullish with a consensus Moderate Buy rating on the stock. Investors are looking forward to the upcoming earnings report to lift shares, but can the company deliver?

ChargePoint is building a vast network of smart, advanced EV charging stations across the United States, Canada, and Europe. A growing subscriber base boosts its recurring Software-as-a-Service (SaaS) revenue. The company targets fleets of all types and sizes and has a huge growth opportunity ahead of it.

That said, I remain neutral on the stock as it is still in its pre-profit period and there are significant execution risks.

ChargePoint Quarterly Earnings Projections

Last quarter, ChargePoint released market-beating results, seeing its revenue increase by 79% year-over-year to $65 million. Sales came in at the upper range of management’s guidance. The company then provided higher revenue guidance for the fourth quarter of $73-$78 million, representing a potential increase of 78% year-over-year at the midpoint, and a sequential quarterly increase of over 16%.

The company increased its revenue guidance for the Fiscal Year 2022 from $225-$235 million to $235-$240 million in December. The latest guidance represents a 62% increase year-over-year. The numbers will be aided by recent acquisitions, but organic growth remains strong to support ChargePoint’s status as a growth stock.

During the third-quarter earnings presentation, Rex Jackson, the company’s Chief Financial Officer (CFO) said, “We are very pleased with this performance despite a number of supply chain challenges and demand in the quarter we could not meet has given us a good start on Q4.”

Wall Street analysts project a 79.3% growth in ChargePoint’s fourth-quarter revenue to $76 million. They also expect full-year sales to hit $237.7 million, representing a 63.2% annual growth from the previous year. The consensus earnings per share (EPS) estimate for the fourth quarter is a negative $0.16 per diluted share, a significant improvement from the previous year’s $1.718 loss per share.

However, it should be noted that ChargePoint has missed analysts’ EPS forecasts in three of the last four reported quarterly earnings results.

Key Revenue Growth Drivers

There are three revenue growth drivers investors should watch for ChargePoint going forward. The company is a fast-growing EV stock with strong organic growth. Moreover, periodic acquisitions and strategic partnerships remain important revenue growth drivers for CHPT.

Fourth-quarter sales should accelerate after the integration of recent acquisitions of mobility and charging solutions firms has-to-be and ViriCiti. A new partnership with Mercedes-Benz USA for a “me Charge” charging solution in 2022 could add some growth opportunities as well.

The company recently entered into another partnership in France with charging station company Sonepar to deploy more infrastructure across the European country.

How the above factors combine to power ChargePoint stock to a strong growth status follows a simple analogy.

ChargePoint’s revenue is grouped into three segments, namely Network Charging Systems, Subscriptions, and Other revenue. Network charging systems represent hardware that is all sold with the company’s cloud services solutions. During the last quarter, this segment accounted for 73% of quarterly sales.

Subscriptions for cloud services could grow significantly in the near-term after a recent acquisition of ViriCiti, a leading eBus and commercial vehicle management provider. Meanwhile, the Subscriptions segment comprised 21% of last quarter’s total sales.

The company closed its third-quarter with approximately 163,000 network ports under management. ChargePoint is investing in more charging ports as electric vehicle purchases continue to surge in Europe and North America.

Most noteworthy, a politically supported transition to electric vehicles in major global markets should continue to strongly support a growth thesis on ChargePoint stock throughout 2022 and beyond.

Supportive Government Policy Supercharges ChargePoint Stock

The company is set to benefit from the U.S. Infrastructure Investment and Jobs Act, which proposes up to $7.5 billion to be channeled towards accelerating the build-out of charging ports along highways and in communities. The company has been working with policymakers at the Federal and State levels to shape this development.

“While other state and utility programs are in place now, this new stimulus will likely benefit significantly beginning in 2023,” said Pasquale Romano, ChargePoint’s Chief Executive Officer (CEO), during the third-quarter earnings presentation.

Most noteworthy is the company’s addition of former U.S. Secretary of Transportation and Labor, Elaine Chao, to its Board of Directors. “Her appointment brings depth from both public and private sectors and further strengthens the Board composition,” said Romano.

It’s fair to assume that the new board member could help the company engage fruitfully with government stakeholders on key policies that affect its industry.

Wall Street’s Take

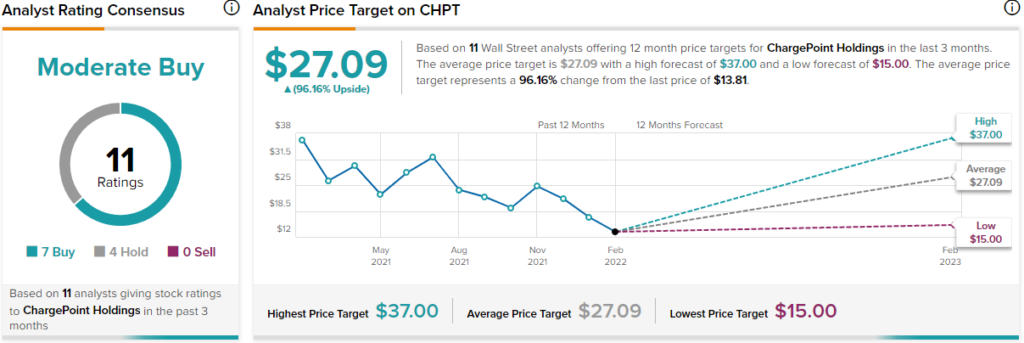

CHPT has an analyst rating consensus of Moderate Buy based on seven Buy and four Hold ratings. The average ChargePoint price target of $27.09 represents 96.16% upside potential over the next 12 months.

Investor Takeaway

ChargePoint’s valuation has continued to go down despite improving fundamentals over the past three quarters. Shares currently trade near 52-week lows as spooked investors exit high-risk growth stocks with lofty multiples, negative cash flows, and operating losses.

While it’s every investor’s hope that upcoming earnings might set the stage for a strong lift, it’s important to note that the company is still in its pre-profit period. Profits might still be far off, and significant execution risks still remain.

Download the TipRanks mobile app now

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Read full Disclaimer & Disclosure