ARK Invest founder and Chief Investment Officer Cathie Wood believes Roku’s (ROKU) stock price could surge as much as 700% by 2026. Wood’s base case is that the company’s dominant market share will result in exponential revenue growth worth approximately 39% per year. Furthermore, ARK’s team identified 33 independent variables that could affect the stock’s price, consolidating its view from a holistic vantage point.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Although ARK’s base case does form a reasonable basis, it ignores a few critical variables that could cause Roku’s stock to retreat. As such, I’m bearish on Roku; here’s why.

Operational Analysis

Roku generates its revenues from two segments — Platform and Player. During its previous financial quarter, Roku’s Platform segment raked in revenue worth $646.9 million (+39% year-over-year), and its Player segment generated revenue of $86.8 million (-19% year-over-year).

Furthermore, Roku’s active accounts rose 14% year-over-year, showing signs of sustaining its growth trajectory, even during turbulent economic times.

Although Roku’s top line metrics continue to impress, its other line items are suffering as the company struggles to curb costs. For example, Roku’s EBITDA (earnings before interest, tax, depreciation, and amortization) has receded 54% year-over-year. Moreover, the company guides a break-even EBITDA for its second quarter, suggesting that the firm’s income statement efficiency might continue to deteriorate.

Following Roku’s previous financial quarter, Morgan Stanley’s (MS) Benjamin Swinburne cut his $115 Roku price target to a more modest $105. According to Swinburne, industry maturity and new market entrants will “likely remain key factors weighing on the growth outlook ahead.”

Swinburne’s argument provides an interesting juxtaposition to Cathie Wood’s as the prior recognizes the industry maturity cycle and its effect on Roku’s growth rate, whereas the latter’s analysis doesn’t.

Lastly, quantitative metrics imply that Roku’s ROIC (return on invested capital) of -7.81% conveys the fact that industry competition has already heated up and the company could soon struggle with pricing power.

Market Headwinds

Basic statistics help explain Roku’s prospects in the current market. Firstly, Roku’s a high-beta (1.93) asset, causing it to experience excess sensitivity to the broader market. Thus, if 2022’s bear market sustains itself, Roku will likely be one of the major losers.

Furthermore, Roku is classified as a growth stock, meaning that its stock profile is contra to contractionary economic policies. Rising interest rates guide investors into value and low-volatility stocks, which Roku clearly isn’t.

A recent Bank of America (BAC) research report substantiates the market’s current anti-growth rhetoric. According to the banking giant, technology stocks earnings won’t exhibit defensive characteristics during an economic downturn, despite increased technology reliance in recent years.

Valuation

Another primary concern about Roku is that it’s significantly overvalued. The stock’s price-to-earnings ratio of 89.3 spells trouble, especially as its PEG ratio (5.84x) suggests that the market overscores Roku’s earnings-per-share growth.

Furthermore, Roku stock’s trading at 3.99x the company’s sales and 50.55x its cash flow, hinting that the stock is overvalued on both a cash and an accrual basis.

Insider Trading Activity

TipRanks’ insider trading tracker gauges that Roku’s internal management is seemingly bearish on the stock. During the previous quarter, the firm’s corporate insiders sold $245.2K worth of stock.

Insider trading isn’t a metric that should be used in isolation when analyzing a stock. Nonetheless, it provides an indication of management’s expectations of the company’s financial results, which often come to fruition.

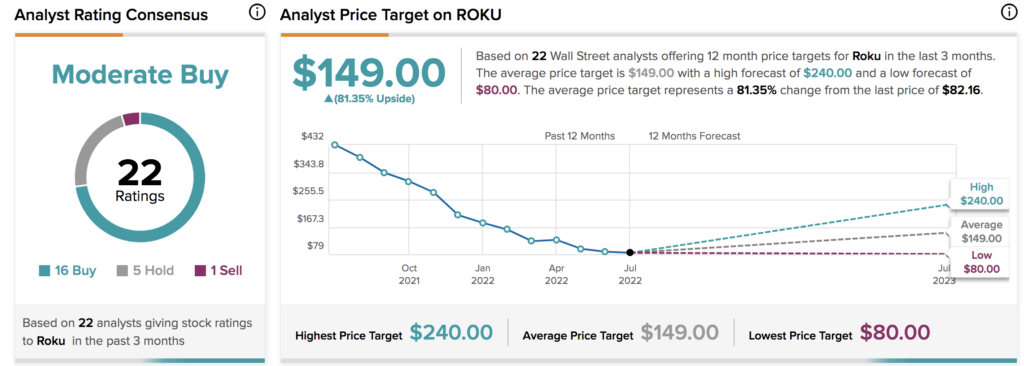

Wall Street’s Take on ROKU

Turning to Wall Street, Roku earns a Moderate Buy consensus rating based on 16 Buys, five Holds, and one Sell. ROKU’s average price target of $149 implies 81.35% upside potential.

Concluding Thoughts

Cathie Wood’s ARK Invest has once more made a brave call by claiming that Roku stock could proliferate by as much as seven times its current value. Nevertheless, most of TipRanks’ key metrics, a deconstruction of the firm’s financial statements, and qualitative theory imply that Roku could be set for further drawdowns.

Read full Disclosure