Right now, we’re at the cusp of a world-changing shift in the green energy economy, as both social and political will have come together to promote a switch from traditional fossil fuels to sustainable and environmentally friendly energy sources. For investors, this shift can open up new vistas of opportunity.

Morgan Stanley’s Andrew Percoco believes that the opportunity in clean energy is substantial. The analyst maintains a ‘constructive’ view of energy renewables, and picked out two stocks that show potential for 100% upside or better. Percoco is not alone in his bullish stance on these stocks —according to the analyst consensus, both are also rated as Strong Buys.

For risk-tolerant investors seeking to double their money, these stocks may warrant further consideration.

Stem, Inc. (STEM)

The first Morgan Stanley pick we’ll look at is Stem, an interesting clean energy play that combines renewable power and energy storage with artificial intelligence. Stem offers a product line of smart battery systems and an AI-powered platform to optimize the connections between on-site power generation, grid power, and stored power. The company’s customers can leverage the system and potentially save between 10% and 30% on their energy utility bills.

Stem’s Athena platform is billed as the most utilized system in its class. The AI has been ‘trained’ through tens of millions of runtime hours, making it the most effective software of its kind. Stem’s platform is available around the world, and the company’s footprint extends across 75 jurisdictions globally, and Athena is in use with more than 200,000 solar sites, managing over 25 gigawatts of solar assets. Stem estimates that its addressable market can grow to $1.2 trillion by 2050.

Stem is already showing strong growth, and in 2022 the company recorded a total of $363 million in revenue, up 186% year-over-year and a company record. At the quarterly level, the company’s $156 million top line was up 194% y/y. However, the market analysts had predicted $166 million in revenues for the quarter, and the 2023 full-year guidance, set at $550 million to $650 million, was below the consensus forecast of $647 million at the mid-point.

Shares of Stem are down 51% over the last 12 months, but that hasn’t discouraged Morgan Stanley’s Andrew Percoco who writes: “We continue to see STEM’s software-focused strategy as a favorable way to play the energy storage market and as a long-term growth driver that is greatly underappreciated in the stock’s current 20% discount to energy storage peers… We view STEM as a key beneficiary of an improving battery supply chain and see an attractive cross-sell opportunity between its legacy storage business and solar monitoring business…”

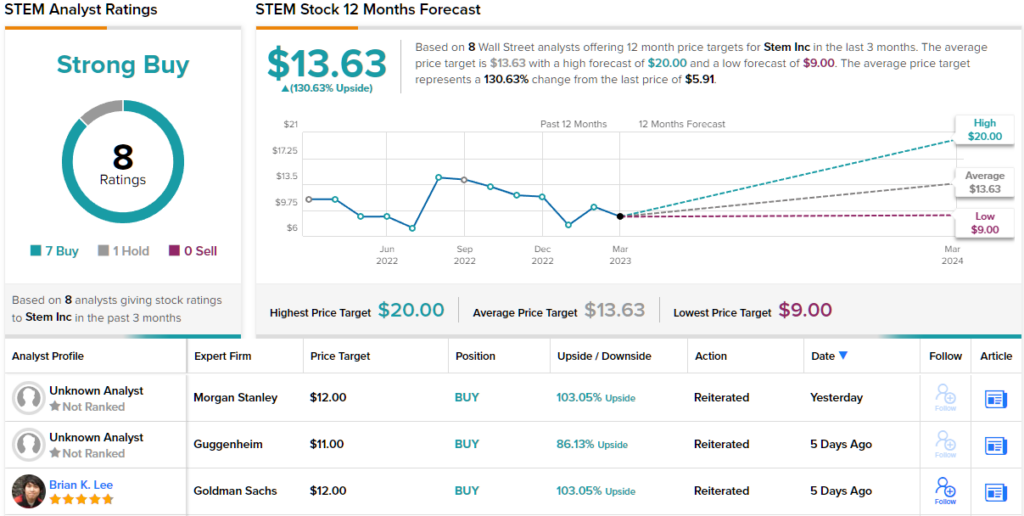

These comments back up Percoco’s Overweight (i.e. Buy) rating on Stem shares, and his $12 price target implies a robust 103% one-year upside potential.

The Morgan Stanley view is hardly the only positive take on Stem. The company has 8 recent reviews from the Street’s analysts, including 7 Buys and 1 Hold, for a Strong Buy consensus rating. Overall, the $5.91 current trading price and the $13.63 average price target indicate ~131% upside for the stock in the next 12 months. (See STEM stock forecast)

Sunnova Energy International (NOVA)

The second Morgan Stanley choice is Sunnova Energy, one of the leaders in the solar power field. Sunnova’s operations include every aspect of the solar installation process, starting with the rooftop panel installations to the home power system connections to the power storage batteries. The company also provides full back-up services to its products, offering repairs, modifications, and parts replacement as needed. Sunnova even provides financing assistance and insurance for its customers.

Sunnova’s footprint encompasses 40 US states, and the company has more than 279,400 active customers on the books. The company serves its customers through a wide network of dealers, sub-dealers, and builders, currently totaling more than 1,100 providers. In the final quarter of 2022, Sunnova added 33,000 new customers, capping a whole-year gain of 87,000. Sunnova expects to continue adding customers in 2023, and has projected between 115,000 and 125,000 adds for this year.

Getting to the 4Q22 and full-year financial results, Sunnova reported strong year-over-year quarterly growth. Revenues expanded from $65 million to $195.6 million, a gain of 200% – and even that may understate the revenue strength, as the top line beat expectations by more than $55 million. Quarterly EPS came in at a net loss, of 18 cents, but that net loss was 26 cents better than the forecast 44-cent EPS loss.

Morgan Stanley analyst Andrew Percoco likes the risk/reward that Sunnova shares currently offer, despite acknowledging their potential for volatility

“We like NOVA’s exposure to a vastly under-penetrated market (4% of US homes), with strong long-term growth prospects. Several near-term risks are present, including a potential prolonged slowdown in demand from policy changes in California, and its exposure to a potentially volatile financing environment, which may put pressure on the stock. That being said, we see this as an attractive buying opportunity for those willing to accept near-term volatility, as the stock is trading below the value of its existing assets,” Percoco opined.

To this end, Percoco gives NOVA shares an Overweight (i.e. Buy) rating and a $35 price target to imply a 126% potential upside for the coming year.

Overall, clean energy has become a go-to investment sector and Sunnova’s 12 recent analyst reviews, favoring Buys over Holds by 10 to 2, reflect that. The ‘Strong Buy’ stock has an average price target of $33.08, suggesting ~114% potential gain from the current trading price of $15.48. (See Sunnova stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

Questions or Comments about the article? Write to editor@tipranks.com