For investors seeking a solid return few strategies beat the classic ‘buy the dip’ approach. The idea is simple: spot a stock with a temporarily depressed price but solid potential to rebound, and scoop it up while it’s still a bargain. It’s the golden rule of investing – buy low, sell high.

Identifying stocks that have taken a hit is easy; the real challenge lies in distinguishing the ones set for a comeback. Not every stock that dips is a bargain – some are in a downward spiral with no recovery in sight. The key is finding companies with strong fundamentals that are experiencing only a temporary setback rather than a long-term decline.

Enter Piper Sandler’s Stephen Scouten, who sees a buying opportunity in two Southeast bank stocks that have recently dipped. The Southeast has been a major driver of US economic growth in recent years, with such powerhouse states as Tennessee and Florida – which make the region a likely home for strong stocks.

To get the full picture, we turned to the TipRanks database to see what the rest of Wall Street thinks about Scouten’s picks. Let’s dive in.

FB Financial Corporation (FBK)

The first stock we’ll look at, FB Financial, is a Tennessee-based bank holding company, operating through its subsidiary, First Bank. From its headquarters in Nashville, capital of one of the most dynamic state economies, FB Financial oversees a network of bank branches across Tennessee, Kentucky, Alabama, and Northern Georgia, and operates mortgage offices across the Southeast region. The company serves individuals, families, and businesses, and takes a ‘local first’ approach to banking business.

The company offers a full range of banking services. Individuals can access personal checking and savings, take out loans, acquire debit and credit cards, and even set up overdraft protection. On the business side, FB offers, again, checking and savings accounts, as well as business loans, credit services, and treasury management. Customers can access their accounts in person at branch locations, as well as online via desktop and mobile devices. The banking company also offers investment and trust services, as well as mortgage lending.

In its last quarterly earnings release, for 4Q24, FB Financial reported a top line of $130.37 million, up from $116.42 million in 4Q23. At the bottom line, the company’s 85-cent non-GAAP EPS was 2 cents better than had been expected.

The company also pays out a dividend, which was raised to 19 cents per common share in the last declaration, made on January 29. This translated to a 12% increase in the dividend payment, which now annualizes to 76 cents per common share and gives a modest forward yield of 1.66%. The dividend was paid out on February 25.

We should note that the stock has slipped year-to-date but analyst Scouten bases his upbeat outlook on the stock’s sound base and the likelihood that the current pullback is only temporary.

“Shares are down [~ 11.5%] YTD and [~16.5%] since February 6th, presenting attractive entry point for a strong and expanding franchise, with low-double digit growth likely on the horizon. Upside potential comes from strategic hiring, geographic expansion, and a more aggressive M&A approach. Credit remains solid, with a 1.58% LLR and minimal NCOs. Efficiency gains further strengthen the investment case, with the core efficiency ratio improving ~750 bps y/y. Our $58 PT remains ~13x our 2026E + $/$ credit for excess capital – justifiable for a projected 1.4% ROA and ~11% ROE,” Scouten noted.

These comments support his Overweight rating on the shares, and his stated $58 price target implies a one-year upside potential of 28%. (To watch Scouten’s track record, click here)

Only one other analyst has recently waded in with an FBK review and their Hold rating makes the consensus view here a Moderate Buy. The $58 average target matches Scouten’s objective. (See FBK stock forecast)

BankUnited (BKU)

Next on our list of Southeastern bank stocks is BankUnited, a Florida-based independent savings bank – and one of the largest such independent operators based in that fast-growing state. BankUnited has over $35 billion in assets, and operates banking centers in Florida and New York, as well as in Dallas, Texas.

BankUnited, like most of its peers, offers a full range of services in the consumer and commercial banking sectors. The company addresses a broad customer base, serving private individuals, small businesses, mid-market firms, and even larger corporations and institutional customers. Services include checking and savings accounts, CD accounts, credit cards and credit lines, small business lending, commercial banking and lending, and corporate treasury solutions.

Turning to the company’s results, we find that BankUnited generated $264.5 million in revenues during its last reported quarter, 4Q24. This was up 13% year-over-year and came in $2.75 million higher than had been anticipated. The company’s EPS figure, at 91 cents, was 21 cents per share better than the estimates – and marked a hefty increase from the 27-cent EPS reported in 4Q23.

The bank company’s dividend is also attractive. Last declared on December 26 for 29 cents per common share, the dividend annualizes to $1.16 per share and gives an inflation-beating forward yield of 3.5%. The dividend was last paid out on the last day of January.

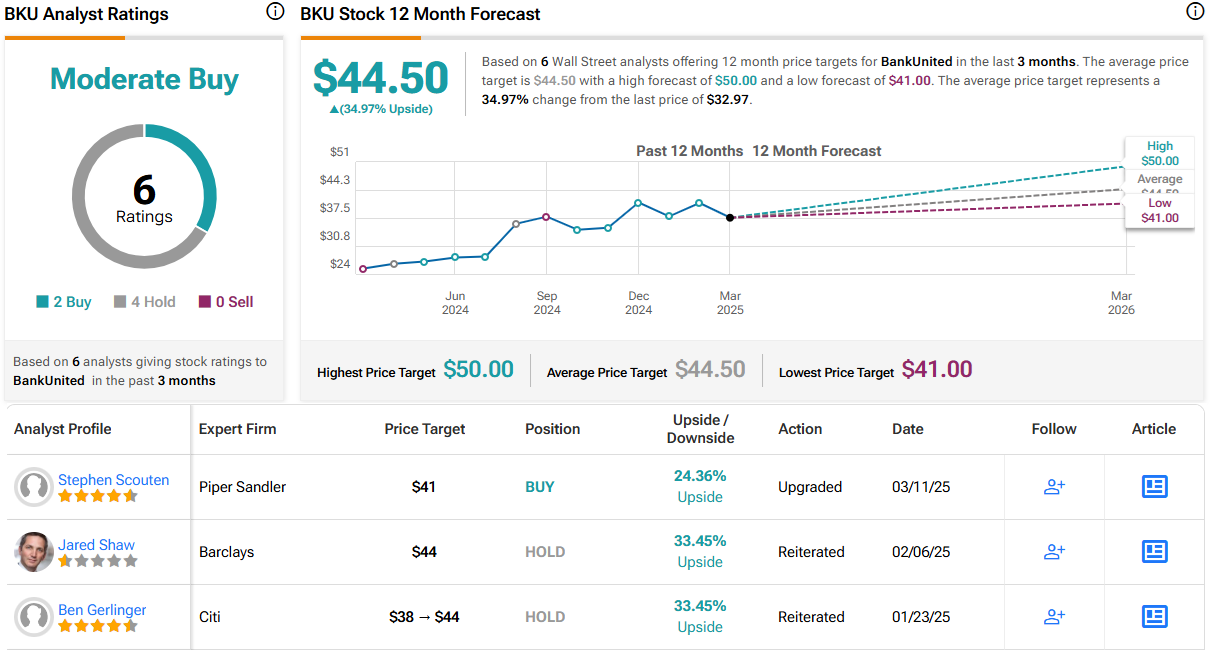

BKU shares have also been on the backfoot recently, but checking in again with Piper Sandler’s Scouten, we find the analyst taking a bullish outlook, noting that the bank has sound fundamentals and strong prospects.

Laying out this position, Scouten writes, “BKU currently trades at ~86% of TBVPS, down [~13%] YTD and [~20%] from February 6th. While BKU continues to deliver below peer returns – with its projected ROA/ROEs of 0.70% and 8.2% respectively in 2026 – we do see directional improvement continuing. BKU is one of the few names where we are currently building the LLR % through 2026 as the bank shifts further away from resi RE, so concerns about elevated LLPs should not be a risk here. On a core basis, the bank’s deposit base and NIM have been improving y/y. Additionally, while the share repurchase has been on pause since 1Q23, we think that it could become more attractive at these levels and fuel greater upside in the shares.”

Scouten sets an Overweight (i.e., Buy) rating on BKU shares, with a $41 price target that suggests the stock will appreciate by 24% in the next 12 months.

BKU stock has 6 recent analyst reviews, and the 4 to 2 split favors Hold over Buy for a Moderate Buy consensus rating. The $32.97 trading price and $44.50 average target price combine to suggest a 35% increase for BKU in the year ahead. (See BKU stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

Questions or Comments about the article? Write to editor@tipranks.com