If you’re looking for a large-cap success story from this coronavirus-stained year, look no further than GPU giant Nvidia (NVDA). Driven by two segments – gaming and data center – perfectly suited to the times, investors have rewarded Nvidia with share gains of over 70% year-to-date. So, is now the time to reduce exposure to this impressive performer?

Au contraire, says Rosenblatt analyst Hans Mosesmann, who argues Nvidia’s “data center and gaming tailwinds are just getting started.”

The 5-star noted, “We continue to like the Nvidia story over the long-term, as we see the secular shift to data processing units within the data center, the entrance into new markets (inference, analytics, machine learning), and strategic partnerships (Mercedes-Benz, potentially others) helping to drive strong revenue growth over the coming years.”

Mosesmann doesn’t expect data center momentum to slow down anytime soon. With the recent addition of data specialist Mellanox, the segment now makes up 40% of Nvidia’s overall business. Along with Mellanox, Mosesmann sees additional tailwinds stemming from the A100 Tensor Core GPU – the world’s fastest cloud and data center GPU – and “the secular shift within the data center to the data processing unit (DPU).”

As for gaming, with most games now able to run on different platforms, Nvidia will benefit from users’ ability to purchase new GPUs along with new consoles. Therefore, the launch of new gaming consoles during the holiday season should act as another tailwind for Nvidia “for many quarters.”

Add to the mix Nvidia’s new partnership with Mercedes, in which the two are collaborating on self-driving vehicles using Nvidia’s DRIVE platform – set to hit the market in 2024 – and Mosesmann makes a bold, yet realistic prediction.

“We would not be surprised if this initial partnership between Nvidia and Mercedes leads to a string of additional partnerships for Nvidia, as the Nvidia DRIVE platform is the only other platform outside of Tesla that can bring software and AI capabilities to the car,” the analyst said.

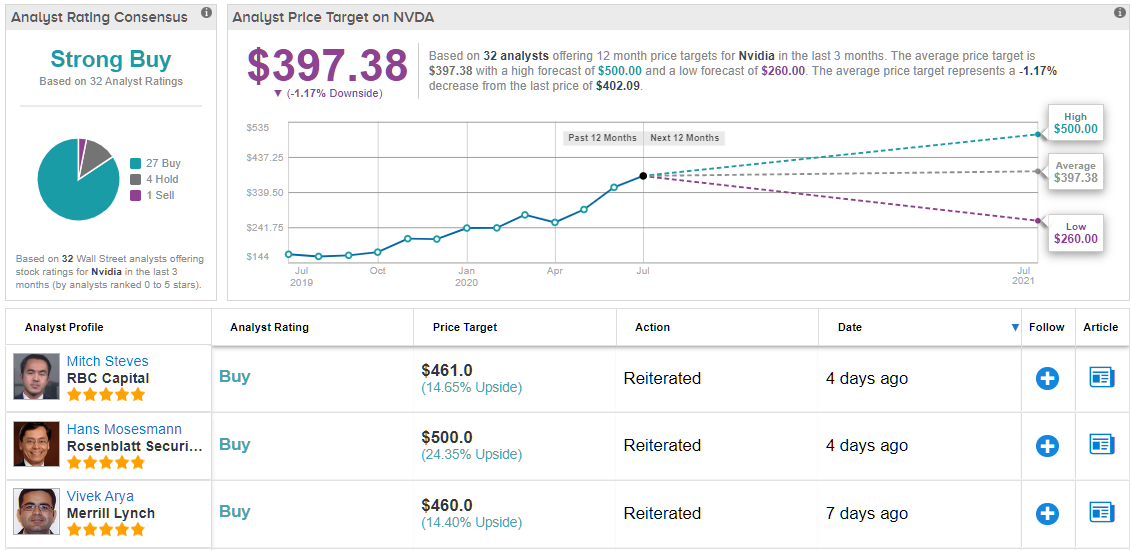

To this end, Mosesmann maintains a Buy recommendation on Nvidia shares and raises the price target from $400 to $500. What’s in it for investors? Upside potential of 19%. (To watch Mosesmann’s track record, click here)

Nvidia has received strong support from Mosesmann’s colleagues, too. Its Strong Buy consensus rating is based on 27 Buys, 4 Holds and 1 Sell. However, given those outsized gains, the $397.38 average price target implies a modest downside. (See Nvidia stock-price forecast on TipRanks)

To find good ideas for tech stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Questions or Comments about the article? Write to editor@tipranks.com