Pharma giant Bristol-Myers Squibb (NYSE: BMY) has seen a fairly poor performance in the past number of years as it’s been outperformed by most of its peers and most indexes.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Investor excitement towards BMY has lagged tremendously over the past five years only gaining around 15%. During the same period, dividend yields ranged between 2-3%.

However this poor performance is largely due to significant overvaluation from 2014-15 rather than reflecting on the company’s actual performance such as EBTIDA growth, pipeline development and revenue growth.

BMY has a portfolio of drugs in different therapeutic classes including oncology, immunology, cardiovascular and fibrosis. BMY has done a great job in growing revenue, which has been largely helped by its acquisition of Celgene in 2019. Oral cancel drug Revlimid, which treats multiple myeloma, came from the Celgene acquisition which makes up 27.59% of BMY’s total revenue.

The main worry for investors is patent losses on a number of key drugs in the portfolio. These include Revlimid (2026 expiry), Eliquis (2026 expiry), Opdivo (2028 expiry) which makes up the majority of BMY’s revenue.

These patent losses need to be more than offset with the development of new drugs. This is no small feat as these drugs currently account for over $28 billion annually in net sales. BMY needs to drive R&D (increasing Capex) to develop new drugs in order to account for the $28 billion in net sales.

New drug development is largely risky and new drugs aren’t always approved by the FDA or show positive results in trials. However the positive is that BMY already has a large pipeline of 50+ compounds in development. Furthermore, BMY has several years to close the gap for when it loses exclusivity on key drugs.

Management is guiding net positive growth over the next eight years, and aims to maintain a 40-45% operating margin through 2025.

Ultimately, management believes it can more than offset the patent losses and still grow. Future targets are very difficult to estimate, but if management is successful, BMY is primed to be one of the best large cap pharmaceutical opportunities of the decade.

BMY Is Cheap

BMY stock is already cheap, with a number of short-term tailwinds to can support higher valuations.

Last year, management announced a 10.2% dividend increase, while also announcing its commitment to buy back $15 billion worth of stock over the coming years.

This comes at a time where BMY stock is already very cheap with NTM EV/EBITDA of 7x and free cash flow per share (consensus) around $8.41 for FY 2022.

This will yield free cash flow of around 13% in 2022, which is attractive for investors especially when you consider buybacks should help slightly boost the 13% yield as the share count is reduced.

DCF

The DCF is built partly using consensus estimates with a mix of conservative assumptions such as a 10% discount rate and 13x EV/EBITDA exit multiple.

I also increased capital expenditures by 25% annually between FY 2023-26 in order to aid R&D, should higher spending be needed to meet pipeline milestones. The key limitation of the model below is that its a five year forecast, therefore revenue losses (post 2026) from Revlimid aren’t accounted for.

Rather, a perpetual growth rate of 2% is applied to determine BMY’s growth post 2026 which is fair considering management is guiding growth into 2029.

The forecast above shows EBIT and free cashflow growing at low single digits, with free cash flow being way below analysts’ targets: $19.14 billion in FY 2022 and $20 billion in FY 2023. This helps maintain a margin of safety and minimize downside risk should management miss its free cash flow targets.

Not accounting for buybacks/dividends and keeping cash/debt the same as it is today, the model suggests an intrinsic value of around $114.41 per share, with an estimated equity value of $256 billion.

The key limitation is this model assumes patent losses in the period can be more than offset with single-digit growth. Furthermore, the model doesn’t show what might happen going into 2027 when key patent expiry might lead to a dip in free cashflow.

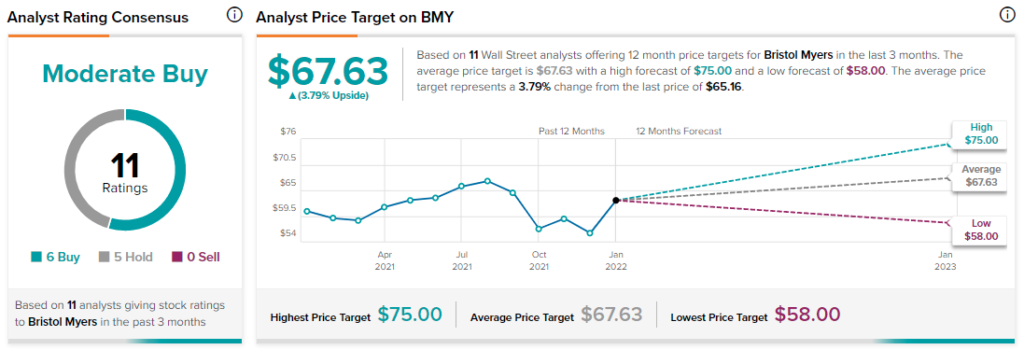

Wall Street has Buy ratings, five Hold ratings and zero sell ratings assigned to the stock.

Conclusion

Conservative modelling indicates BMY is heavily undervalued if management is successful in meeting its pipeline milestones, and achieves a 58% FDA approval rate on its phase 3 assets. This could result in an intrinsic value per share over $114, with an equity value of $256 billion.

Both in the long term and medium term BMY has the earnings to support higher valuations. With the added benefit of a sustainable 3.2% dividend yield ($2.16 dividend) and the $15 billion worth of stock buybacks coming over the next few years makes BMY stock attractive for both value and dividend investors.

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Read full Disclaimer & Disclosure