Comprehensive customer engagement platform Braze (BRZE) is on a bull run since releasing its fiscal Q3 results yesterday, December 20. Shares of the company rallied 3.52% at yesterday’s market close, and a further 11.04% in the after-hours trading session.

Talking about the company’s background, Braze’s platform helps consumers interact with brands. The company processes large volumes of customer data in real-time, manages and optimizes relevant marketing campaigns, and regularly updates its customer engagement strategies.

Braze faces significant competition from stalwarts like Salesforce (CRM), Adobe (ADBE), IBM (IBM), and Oracle (ORCL). However, the company’s focused and well-articulated solutions are pulling in the crowds and supporting its competitive position.

Q3 Results Suggest Solid Momentum

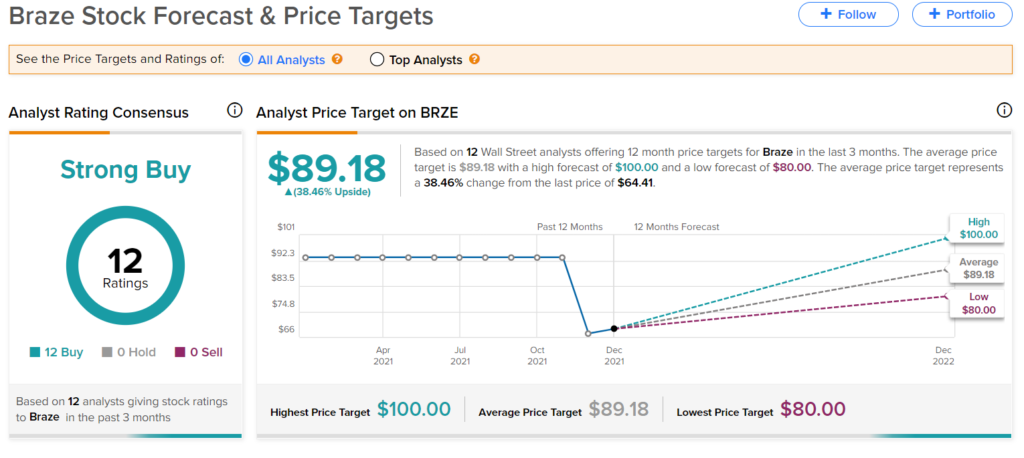

The earnings release was Braze’s first since releasing its IPO last month. However, it is not new in the customer engagement game and enjoys the positive ratings of all 12 of the Wall Street analysts who cover this stock, ensuring a Strong Buy consensus rating for the BRZE stock.

Significantly, in Q3, new customer additions, upsells, and subscription renewals led to a 62.6% year-over-year top-line growth. Moreover, the net loss per share also narrowed considerably during the quarter as compared to the prior year’s Q3.

Strong organic growth in the company’s SaaS (software-as-a-service) solutions and solid billings growth was another area of focus.

Expert Observations

Oppenheimer analyst Brian Schwartz was pleased with Braze’s Q3 performance. He noted that the Q4 guidance provided by the management looked too conservative, given the strong business momentum that drove solid Q3 results. This makes him believe that there is an upside to the Q4 guidance.

“The fast growth trends and overall strength the company produced in F3Q:2022 point to sustainable 40%-plus revenue growth and lend good support to our thesis that BRZE has open-ended growth and is an attractive play on the customer engagement market themes,” said Schwartz. He believes that Braze has the potential to lead the market and “be a good compounding-growth story to support a premium valuation.”

He reiterated a Buy rating on the stock with a price target of $85. The Braze stock projections stand at $89.18 on average, indicating a 38.46% upside.

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclosure: At the time of publication, Chandrima Sanyal did not have a position in any of the securities mentioned in this article.

Disclaimer: The information contained in this article represents the views and opinion of the writer only, and not the views or opinion of TipRanks or its affiliates Read full disclaimer >