The Boeing Company (NYSE:BA) was expected to make further headway in its post-pandemic recovery in 2024, but things haven’t gone to plan. The blowout of a door plug on a 737 Max 9 in January has compounded legacy safety concerns, leading to significant reputational damage and a slow-moving order book. The consensus, however, is that the company, and its earnings, will recover. Personally, though, I’m not convinced that now is the time to buy. Thus, I’m neutral on Boeing.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

Boeing’s Reputational Damage

Boeing’s reputational damage shouldn’t be overlooked, both within the civil aviation industry and among the general public. Personally, I no longer fly on Boeing aircraft — this is certainly easier for Europeans — given the number of incidents in recent years. I know several people who are doing the same.

The firm’s reputational damage stems from a string of incidents, not just those reported in 2024. The crashes of Lion Air Flight 610 (October 2018) and Ethiopian Airlines Flight 302 (March 2019), which killed 346 people, highlighted significant safety issues with the MCAS system. This led to a nearly two-year global grounding of the 737 MAX.

On January 5, 2024, the mid-flight blowout of a “plugged” emergency exit door on an Alaska Airlines (NYSE:ALK) flight brought the airworthiness of Boeing aircraft into question once again. This was compounded by additional high-profile incidents, leading Boeing to rework 50 undelivered 737 Max jets, a $1 billion lawsuit, and a Federal Aviation Administration audit.

According to reports, Boeing will also face criminal charges for violating a settlement related to the two fatal crashes in 2018 and 2019.

Can Boeing Get Back on Track?

Unsurprisingly, Boeing has fallen behind its European peer Airbus (OTC:EADSF) in terms of deliveries. As of May this year, Boeing has delivered 131 aircraft, and Airbus has delivered 256, compared to 206 and 244 aircraft, respectively, during the same period in 2023. This puts Boeing 75 behind last year and Airbus 12 ahead.

For context, Boeing’s record year was 2018 — before the pandemic and the grounding of the 737 Max — with 806 jets delivered to customers. Five months into this year, Boeing is far below the required run rate. By comparison, Airbus is expected to surpass its record year — 863 shipments in 2019 — in 2025, thus completing its recovery since the pandemic.

So far this year, Boeing has secured 103 net new orders after accounting for 39 cancellations. In comparison, Airbus has accumulated 254 gross orders, with 17 cancellations, resulting in 237 net new orders. This is an increase from the same period last year when Airbus had 178 gross orders and 144 net new orders. For context, in 2023, Boeing booked a total of 1,314 net new orders.

Fewer deliveries and orders are likely to impact debt. For 2024, analysts had expected a net debt of around $30 billion, but this has increased to approximately $36 billion due to the Boeing 737 MAX 9 accident.

Sticking with the aviation side of the business, Boeing stock fell on June 25 after a Korean Air Boeing heading for Taiwan dropped 25,000 feet in five minutes. That same day, Airbus stock fell 10% after it cut its guidance for the year. The European aviation giant said it expected to deliver around 770 commercial aircraft this year, down from a previous outlook near 800. This would result in EBIT falling to €5.5 billion from a previous estimate of €6.5 billion.

Thankfully, Boeing’s Defense business is faring a little better. In Q1, the company reported that revenue from the Defense segment had grown 6% year-over-year to $6.95 billion, supported by new orders from the U.S. and its allies. In the earnings call, management suggested the Defense business would move toward historical levels during the year.

What Do the Forecasts Say About Boeing?

Despite concerns about the Aviation business, the consensus suggests that Boeing will recover in the next few years. Earnings per share (EPS) are expected to remain negative in 2024 at -$1.44. This will improve to $5.05 in 2025, $8.58 in 2026, and $12.17 in 2027. In turn, this works out as a price-to-earnings (P/E) ratio of 34.66x in 2025, 20.4x in 2026, and 14.39x in 2027. These forward P/E ratios are quite attractive, especially if some growth can be sustained beyond the forecasting period.

Is Boeing Stock a Buy, According to Analysts?

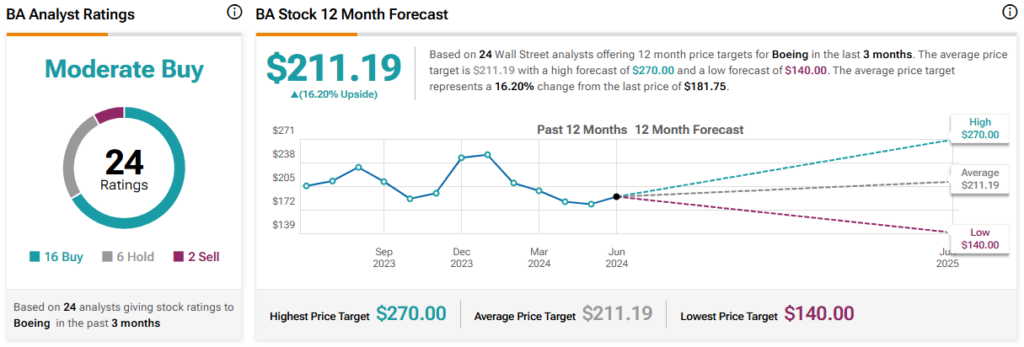

On TipRanks, Boeing comes in as a Moderate Buy based on 16 Buys, six Holds, and two Sell ratings assigned by analysts in the past three months. The average Boeing stock price target is $211.19, implying 16.2% upside potential.

The Bottom Line on Boeing Stock

Boeing stock has fallen 30% since the beginning of the year, but analysts suggest the sell-off has been overdone, with the average share price target indicating 16.2% upside. Forward earnings projections beyond 2024 and 2025 are also quite attractive. However, I remain cautious. Boeing’s civil aviation department has suffered reputational damage, and this could play out for some time, with orders remaining below historical levels.