Square renamed itself Block (SQ) last year, a name it said better reflects the company’s growth beyond payment processing for merchants. Unfortunately, its reliance on the crypto space is a curse rather than a boon in the current environment.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

Since the start of the year, investors have been investing in safer investments because of market volatility. They are putting their money towards dividend and retirement stocks. It is unlikely we will see a turnaround for Block anytime soon in this environment.

There are many available opportunities, and they tend to come up when we’re able to pick up sound businesses at attractive valuations. Block is a terrific business, and I’m excited to see how it grows. However, the timing isn’t right for me yet. The stock valuation is lofty considering industry peers.

The company has been and continues to be a great investment for those looking for high returns but within a reasonable price range. I’m neutral on the stock.

Block Earnings: Mixed Results Highlight Issues

Block’s latest quarterly report disappointed investors, but shares rose in post-market trading due to the exemplary performance of the company’s Cash App.

When excluding contributions made by Block’s newly closed acquisition of Afterpay, the company reported a gross profit of $578 million in its Cash App mobile wallet. The company pointed out several momentum drivers in the release, including increasing activity levels on its newly launched Cash App, and growing interest in direct deposits to the app from consumers.

Block generated $1.29 billion in gross profit for the year. The company has seen a sharp increase since the last year. Investors are interested in staying on top of its operations to make sure its data is accurate. Their main concern is what the recent Bitcoin (BTC) trading initiatives have done to Block’s revenue.

The company posted a net loss in the first quarter of $205 million, or 38 cents per share, whereas it made $39 million, or eight cents per share, last year.

Block’s overall gross payment volume jumped to $43.5 billion compared to $33.1 billion a year ago, while analysts predicted $45.3 billion before the announcement was made.

Block generated $1.23 billion in transaction-based revenue, up from $959.7 million last year. Meanwhile, subscription and services revenue increased to $959.6 million, while hardware revenues increased by $37.3 million.

CFO Amrita Ahuja mentioned that despite the recent launch of free tax-filing services, inflows to his app were not impacted. Nearly 75% of those who used the Cash App and have a prepaid credit card account choose to get their refunds sent to them on the app.

Jury is Still Out on Bitcoin Investment

Blockchain investment is becoming one of the most popular ways for people to allocate capital in cryptocurrency. It’s a lucrative market with many opportunities for investors.

Companies are investing in the potential of blockchain technology. This has been going on for a while, and companies now see the benefits. Some of these being a decreased costs, faster transactions & greater security.

However, while the use cases for blockchain are amazing, it will take time for companies to harness these benefits. Until that time, the biggest use case for crypto is as a source of payment.

To that end, there is trouble in paradise. Since the start of the year, crypto has fallen out of favor. Crypto valuations are at historical lows despite a momentary bump due to the Russia-Ukraine crisis.

What analysts have to be careful of before investing in Block is its revenue line. The line item must be accurate, and the recent developments could make things difficult for investors. They are most concerned when the reported revenue number changes because of initiatives like Bitcoin trading, which brings substantial revenue.

As many retail traders started to show less interest in Bitcoin, the company’s revenue from Bitcoin halved by comparison. After reaching a peak last year, prices continued falling, causing significant losses and impressing few new adopters.

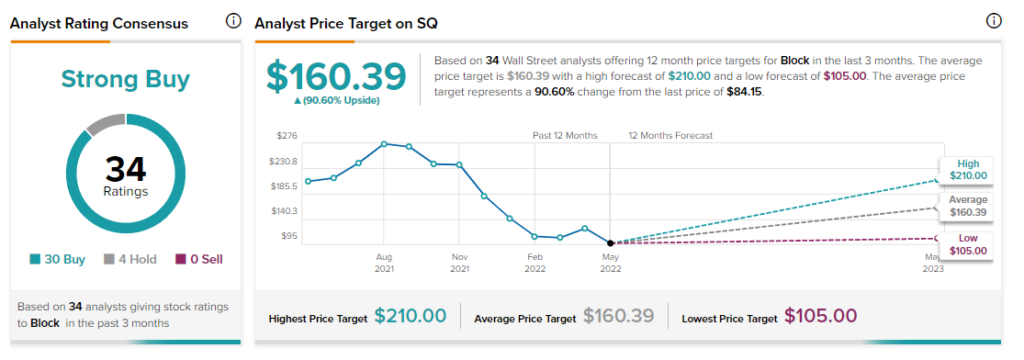

Wall Street’s Take

Wall Street sentiment is bullish on Block. Shares of the financial services and digital payments company sport a Strong Buy consensus rating based on 30 Buys and four Holds. The average Block price target is $160.39, which implies 90.6% upside potential.

Bottom Line on Block Stock

All investors looking to invest in Block can do so at this time. A segment of the investor base will argue that the stock has lost considerable steam, and should be purchased now while it’s at a lower cost. For investors looking to play it safe, waiting for the price to stabilize is good.

My opinion is that Block needs to better the risk-reward profile for investors before people can commit capital to it.

Discover new investment ideas with data you can trust.

Read full Disclaimer & Disclosure