Earlier this week, the Dow Jones joined the S&P 500 and the NASDAQ in bear market territory. It marks the first time this year that the Dow has dipped below a 20% loss from peak – but it also marks a turning point in investor sentiment. A mood of doom and gloom is setting in.

Don't Miss Our Christmas Offers:

- Discover the latest stocks recommended by top Wall Street analysts, all in one place with Analyst Top Stocks

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

A change in times and a change in mood requires a change in outlook, a shift in perspective, for investors to succeed. With all three main indexes so far down, it’s clear that the last year’s modes of trading aren’t going to work in today’s conditions. Chiming in from the $10 trillion asset manager BlackRock, US head of thematics Jay Jacobs is standing up to this challenge and advocating a new focus. Several, in fact.

Jacobs points out that the key driver right now is a shift in the primary market catalyst. Where in recent years, the tech sector has been firmly in the operator’s seat, the main factor now is policy decisions. Changes in governmental priorities, brought on by high inflation and the looming possibility of recession in the near-term, are guiding investment choices. Jacobs identifies three sectors as particularly relevant: agricultural technology, clean energy, and infrastructure.

We can find some interesting insights by following Jacobs’ lead, and looking under the hood at stocks in these sectors. Using the TipRanks database, we’ve looked up three that are showing a combination of solid upside potential and Strong Buy ratings from the analysts. Here they are, along with comments from Jacobs and some of the Street’s 5-star stock pros.

Local Bounti Corporation (LOCL)

We’ll start with Local Bounti, an interesting company in the agricultural technology sector. Jacobs points out agricultural technology as one potential answer to the problem of rising food prices. The Russian war in Ukraine promises to push food prices higher; with the world’s food network suppliers facing increased pressure, alternative sources will be in high demand. As Jacobs puts it, “The higher we see these food prices get, the more demand there’s going to be for agricultural technology solutions to put a lid on those prices.”

And this is where Local Bounti comes in. The company is based in Montana, and specializes in year-round indoor farming techniques for the production of leafy greens. That may not sound like much, but lettuce and other green roughage make up an important part of our truck vegetables, bringing both healthy fiber and vital nutrients to our tables. Local Bounti, which went public through a SPAC just under two years ago, seeks to fill the demand for these veggies.

The company’s main point of differentiation is efficiency. Local Bounti is working on methods of controlled environment and vertical farming to get the most use out of every square foot of indoor agricultural space, and to produce more usable food in fewer ‘food miles’ than traditional outdoor farming and gardening methods can allow.

A look at the revenues will show that this company is making a strong start. The first quarter of this year saw Local Bounti bring in $282K in sales, a powerful gain of 394% from the prior year – but in Q2, the company showed total revenues of $6.3 million, an enormous jump from Q1, and from the mere $100K reported in the year-ago quarter.

The company is also well positioned to benefit from its expansion plans. It’s Georgia growing facility came online in July, using an initial three acres of a planned 24. The company has also announced that it has chosen eastern Texas as the home of its next produce growing facility, and is in ‘site diligence’ to find a location. And finally, Local Bounti, back in March, has entered a definitive agreement to acquire Pete’s (the operating name of a California-based indoor farming company called Hollandia Produce). The acquisition, for $122.5 million in cash and stock, will create a leader in the industry by fusing both companies’ growing networks with Pete’s network of 10,000 retail locations.

This stock has caught the attention of Oppenheimer analyst Colin Rusch, who writes, “We believe LOCL is building a solid foundation of consistency and quality, leveraging its expertise in environmental controls that is an industry differentiator and that positions LOCL as a partner-of-choice for national expansion. On the product front, we are encouraged by the customer demand pull, Local Bounti branding expansion opportunities, and geographic network development to support a much larger organization…”

Rusch goes on to reiterate his Outperform (i.e. Buy) rating on LOCL stock, as well as set a $13 price target. At current levels, his target implies a one-year gain of a whooping 432%. (To watch Rusch’s track record, click here)

This stock is new, and is in a sector that doesn’t always get its due attention, but 5 Wall Street analysts have weighed in on LOCL, and the 4 to 1 breakdown of their reviews, in favor of Buys over Holds, gives the stock a Strong Buy consensus rating. The shares are priced at $2.44 and have an average target of $10.20, suggesting an upside of 318% on the one-year horizon. (See LOCL stock forecast at TipRanks)

Clean Energy Fuels (CLNE)

We’ll shift now to clean energy. BlackRock’s Jacobs’ points out one advantage that clean energy technologies – mainly wind and solar – have over traditional fossil fuels, which is the one-time nature of their build-in costs. A natural gas power plant is dependent, at least in part, on the price of natural gas to determine operating costs. Clean or renewable energy sources typically have that initial cost built in, as the cast of a wind turbine. “In an inflationary environment like we see today, that’s really beneficial to those existing clean energy resources, where they’ve already paid the costs,” Jacobs opined.

And this gets us to Clean Energy Fuels, a firm involved in the production of biofuels, particularly renewable natural gas (RNG) for use as a transportation fuel derived from organic waste. There is no shortage of organic waste in our industrial society, and Clean Energy Fuels is working to turn a problem into a solution – and one that can replace diesel fuel for both a lower cost and a 300% reduction in carbon emissions. Clean Energy Fuels is already the largest provider of RNG to the US automotive industry, as a vehicle fuel. The company counts both UPS and the New York City Metro Transit Authority among its existing customers.

Clean Energy Fuels defines its delivered products, or gallons delivered, as the total of both compressed natural gas and liquified natural gas; both are deliverable forms of RNG. For the recent 2Q22, the company delivered a total of 50 million gallons, up from 42.9 million gallons in the year-ago quarter. Total revenue for the quarter came to $97.2 million, up from a mere half-million in the year-ago period; it’s fair to note that the company had to account for one-time charges in 2Q21 that negatively influenced results. Nevertheless, the Q2 revenue was strong; the highest in two years, and up 11% from 1Q22.

5-star analyst Paul Cheng, of Scotiabank, covers this renewable energy producer, and he’s impressed with what he sees.

“As the leading natural gas fuel distributor in North America, CLNE is in a prime position to fuel the transportation sector’s transition to renewable energy. We think the company’s expansion into upstream RNG production will leverage existing downstream capabilities to provide vertical integration opportunities. This will enhance economics and allow for optimization of gas flows across CLNE’s network to maximize environmental incentives,” Cheng writes.

“The company’s long-standing relationships with feedstock owners and fleet operators established over its 20 years in the industry provides the basis for growth in key customer markets along with securing additional RNG supply,” the analyst added.

Following from his upbeat outlook on the company, Cheng rates CLNE shares as Outperform (i.e. Buy), and his price target, which he puts at $13, indicates room for some robust 137% growth in the year ahead. (To watch Cheng’s track record, click here)

Overall, four of the Street’s analysts have published their thoughts on Clean Energy Fuels, and their missives include 3 Buys and 1 Hold for a Strong Buy rating. The shares have an average target of $13.33, implying a 143% upside from the current trading price of $5.48. (See CLNE stock forecast on TipRanks)

Brookfield Infrastructure (BIP)

Last up is Brookfield Infrastructure, one of the globe’s largest owner-operators of critical infrastructure networks, including capabilities in the movement and storage of data, energy, freight, and water, and the transport of passengers.

The company inhabits the third sector that Jacobs likes, and he points out three points to like about it: it’s defensive, working in essential niches that tend to be recession proof; it’s got a solid business foundation, in which it can set prices and pass them on to customers, which tends to make it inflation proof; and it’s got growth potential, as infrastructure is a common way for politician to spend money. Overall, Jacobs says, “You combine the business case, the defensive nature, and the growth opportunity, and infrastructure is really one of our best-positioned themes in this environment.”

How good a position exactly? Well, in its 2Q22 report, Brookfield reported $3.68 billion in revenues, along with $70 million in net income. EPS came to 13 cents per share. These numbers were somewhat mixed y/y; the revenue total was 38% y/y, but the EPS was down 68%. Brookfield’s FFO, or funds from operations, expanded by 30% to reach $513 million, a company record.

Brookfield generated these results through its network of more than 2000 global infrastructure investments, in over 30 countries. The company has its hands in renewable power, real estate, and private equity, among other endeavors.

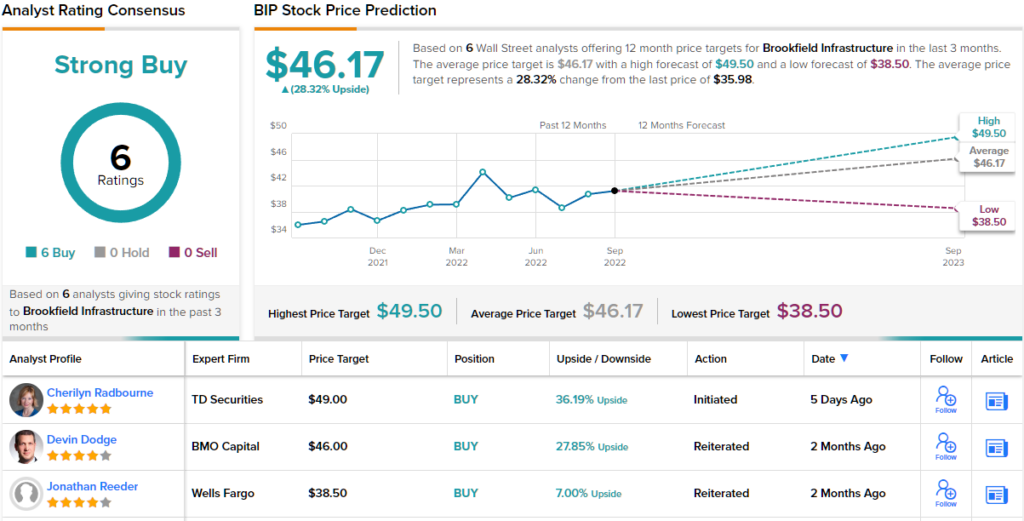

Among the bulls is RBC’s 5-star analyst Robert Kwan who says of Brookfield: “We believe that BIP’s assets and strategy are well positioned to thrive in the current market environment. Specifically, the assets are benefiting in the near term from inflation indexation and GDP-driven upside, with certain assets possessing upside from decarbonization trends. Strategically, BIP’s long-standing focus on asset monetizations is bearing fruit with potential for roughly $2.5 billion in proceeds, which could enable BIP, as a well-capitalized entity, to move quickly on acquisitions if market liquidity tightens.”

Kwan takes these comments to back up his Outperform (i.e. Buy) rating on the shares, which in is view get a $47 price target for a 31% one-year upside potential. (To watch Kwan’s track record, click here)

Overall, BIP gets a unanimous Strong Buy from the Street, based on 6 positive reviews. The shares are trading for $35.98 and their average target, at $46.17, suggests a 28% gain over the next 12 months. (See BIP stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.