Bitcoin failed to fulfil one of its purposes last year as a hedge against soaring inflation, but it came into its own recently via another original purpose – as a bet against the legacy banking system. Its decentralized and trustless attributes have made the leading crypto one to hold against a backdrop of multiple bank collapses. In fact, delivering gains of 70% though Q1 made it the quarter’s best performing asset.

Stay Ahead of the Market:

- Discover outperforming stocks and invest smarter with Top Smart Score Stocks

- Filter, analyze, and streamline your search for investment opportunities using Tipranks' Stock Screener

And it has got plenty more room to run, says Geoff Kendrick, head of crypto research at British banking giant Standard Chartered. “We see potential for Bitcoin to reach the $100,000 level by end-2024, as we believe the much-touted ‘crypto winter’ is finally over,” Kendrick noted.

That’s a gain of 240% from current levels, a surge that will be hard to find elsewhere. For many, though, buying bitcoin directly still represents somewhat of a complicated act but there are ways to get skin in the game without directly purchasing the asset. The stock market presents opportunities with many names operating in the bitcoin ecosystem – miners in particular – and their performance naturally correlates with that of the daddy of crypto. Hence, if bitcoin is set to surge so will many bitcoin-themed stocks.

With this in mind, we delved into the TipRanks database and pulled up the details on 3 crypto stocks poised to make use of that anticipated run. What’s more, all 3 are rated as Strong Buys by the analyst consensus. Let’s take a closer look.

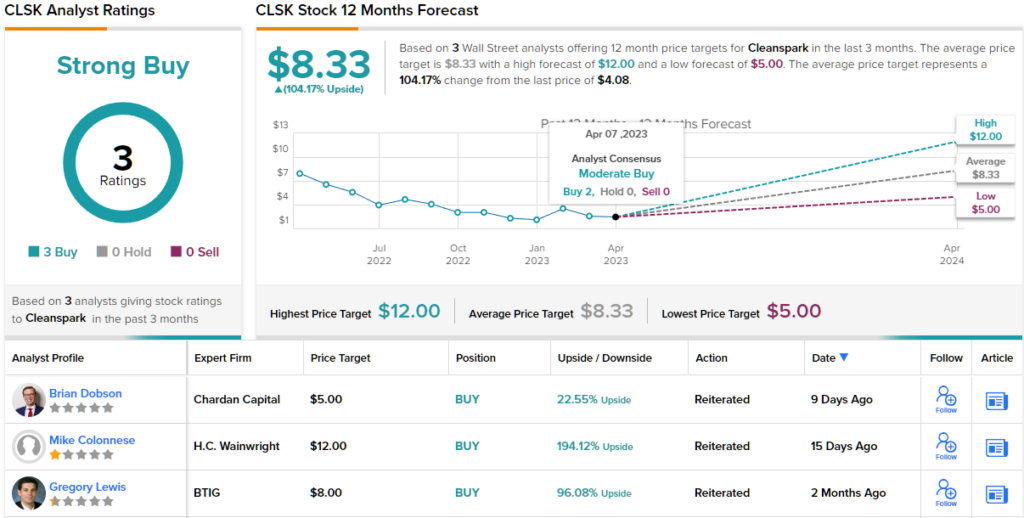

CleanSpark, Inc. (CLSK)

We’ll start with CleanSpark, a bitcoin miner that sometime ago decided bitcoin mining was where it’s at. While once the company specialized solely in microgrid solutions, it began dabbling in mining operations toward the end of 2020. However, since then, mining endeavors have become its main priority.

CleanSpark oversees its own mining operations in Atlanta, Georgia and co-locates miners in Massena, NY. Bitcoin is famous for being hugely energy intensive, but the company likes to highlight its credentials as a sustainable player, mining the bulk of its BTC with renewable or low-carbon energy sources. By often selling its mined bitcoin, the company has funded expansion and last year, even as the crypto winter raged, increased its hashrate – the measure of the computational power used to mine the asset – from 2.1 EH/s in January to 6.2 EH/s at the end of the year.

The company has set its sights on bringing that hashrate up to 16.0 EH/s by the end of 2023, and recent purchases will go toward making that goal a reality. The company recently announced a purchase of 45K new Antminer S19 XP machines that when eventually deployed will almost double the current hashrate.

According to H.C. Wainwright analyst Mike Colonnese, the company exhibited some canny business nous when securing the deal which comes roughly two months following the company’s purchase of 20,000 Bitmain rigs for a 25% discount.

“CLSK secured the machines for a very attractive $23/TH (before applying coupons), the lowest we’ve seen in the market for these rigs, and 12% below the going rate for high efficiency ASICs (under 25 J/TH), based on Luxor’s Bitcoin ASIC Price Index,” the analyst explained.

“Management has been very opportunistic in acquiring new mining rigs at rock bottom prices over the past year, which we believe will drive significant shareholder value, and with this latest purchase, the company has now secured 99%, or 15.9 EH/s of the miners required to reach its year-end 2023 hash rate target of 16 EH/s… We continue to view the stock as significantly undervalued relative to fundamentals,” Colonnese added.

Overall, CLSK shares have soared 98% year-to-date, but Colonnese sees ample growth ahead. Calling CLSK a ‘top pick,’ the analyst rates the shares a Buy while his $12 price target makes room for 12-month returns of a whooping 194%. (To watch Colonnese’s track record, click here)

This bitcoin miner has garnered two other recent reviews and both are positive, making the consensus view here a Strong Buy. The $8.33 average target might represent a more modest objective, but could still yield gains of a handsome 104% over the next year. (See CLSK stock forecast)

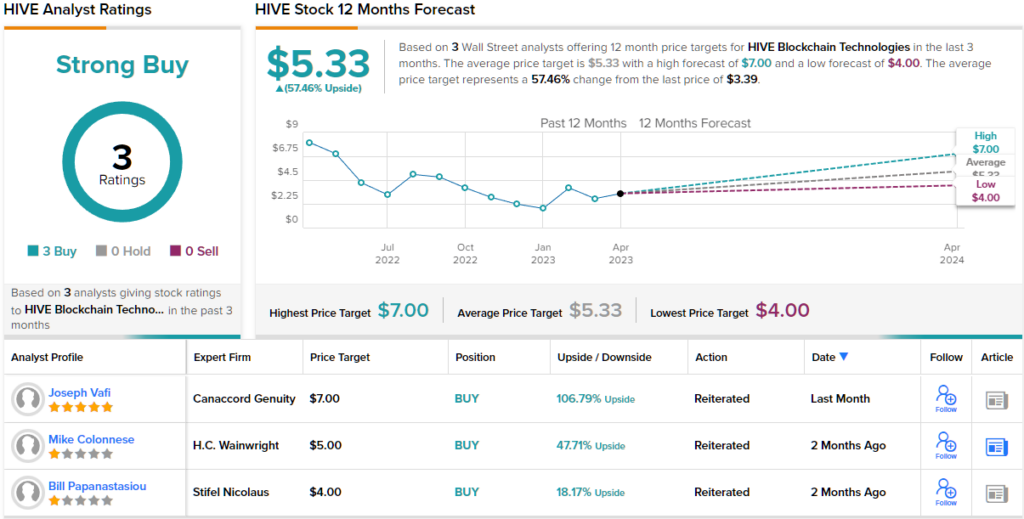

HIVE Blockchain Technologies (HIVE)

The next bitcoin miner we’re looking at is HIVE Blockchain Technologies. Fun fact: in 2017, HIVE became the first publicly traded crypto miner. The company actually got its start as a GPU-based miner of Ethereum but in 2020 it also began mining bitcoin and has expanded is operations since then. The company has a commitment to ESG practices and mines its bitcoin using green energy, making use of favorable power costs and renewable energy sources with mining operations in Canada, Iceland, and Sweden.

Touting its BTC credentials, the company aims to foster long-term shareholder value with the OG practice of HODLing – keeping its bitcoin close to its chest.

That said, HIVE saw a big drop in its revenue stream in the most recent financial report – for its fiscal third quarter (December quarter). Revenue fell by 79% year-over-year to $14.3 million, which can be attributed not only to an increase in global hashrate and reduced cryptocurrency prices but also to Ethereum’s switch to a proof-of-stake model. That said, the company mined 787 bitcoin during the quarter, amounting to a 13% year-over-year increase, while its average cost of production per BTC was $13,599. The current BTC price is more than double that.

The company also said that in order to maximize profitability, it intentionally pulled back on production and also repurposed some of its GPUs into non-mining endeavors.

Looking at these activities, Canaccord analyst Joseph Vafi likes the way this firm operates. The 5-star analyst writes: “We see the current setup for HIVE as healthy on multiple fronts. We are encouraged by the company’s efficient Bitcoin production, strong balance sheet, steady progress at its facilities, and prudent approach toward repurposing its GPU machines. Perhaps most importantly, at a macro level we believe that digital assets are biased higher in the medium term to long term, and especially Bitcoin, which has handled resistance relatively well in the face of recent market volatility…”

These comments form the basis for Vafi’s Buy rating on HIVE, which is backed by a $7 price target. Even after posting year-to-date gains of a hefty 119%, investors stand to pocket returns of 134%, should this figure be met. (To watch Vafi’s track record, click here)

Elsewhere on the Street, with two additional positive reviews in tow, HIVE claims a Strong Buy consensus rating. The forecast calls for 12-month returns of 57%, considering the average target clocks in at $5.33. (See HIVE stock forecast)

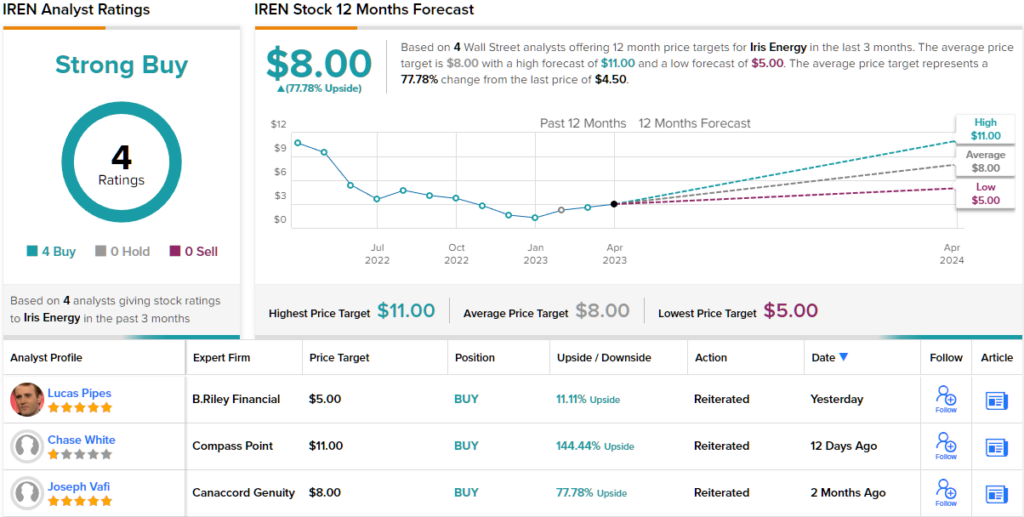

Iris Energy (IREN)

Bitcoin has its fair share of evangelists and two early adopters convinced in its value are the driving force behind are next BTC-flavored stock. Daniel and Will Roberts are the co-founders and co-CEOs of Sydney, Australia-based Iris Energy and used their background and expertise in renewable energy and traditional mining when setting off on their bitcoin mining activities.

The company operates in regions that have an abundance of renewable energy – wind, solar, hydro -and their locations are run on 100% renewables. Iris sticks to a simple plan: mine bitcoin, sell it and pay energy bills and overheads.

However, the company ran into some issues last year, attempting to scale meaningfully at what turned out to be extremely bad timing. With crypto winter at its peak and the industry rocked by multiple scandals (Terra Luna, Celsius, FTX), bitcoin’s price crashed. Against this backdrop, several mining firms over-leveraged, saw profits drop and were driven into insolvency.

However, through prudent business practices, Iris seems to have weathered the storm. And for Compass Point analyst Chase White, the way the company has handled matters informs his bullish take.

“Now that IREN has restructured its balance sheet to eliminate virtually all of its debt, replaced the miners lost to its creditors because of the restructuring with no additional cash outlays, and is almost finished with its capex spend to get to 5.5 EH/s, we believe the company is very well positioned to start generating solid free cash flows at current BTC prices with the opportunity to invest in further growth if BTC prices rise further,” White opined.

In fact, the lack of debt and the near completion of facility buildouts have “derisked the story significantly,” the analyst said.

IREN shares have benefited immensely from bitcoin’s surge and have posted growth of 260% since the turn of the year. However, White thinks there are plenty more gains in store. Along with a Buy rating, his $11 price target suggests the stock has room for additional growth of 144% in the year ahead. (To watch White’s track record, click here)

White’s thesis gets the full backing of his colleagues here. The stock garners Buys only – 4, in total – for a Strong Buy consensus rating. Shares are expected to change hands for ~78% premium a year from now, considering the average target stands at $8. (See IREN stock forecast)

To find good ideas for crypto stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.