In the world of stock legends, Ken Fisher stands out. The legendary investor founded his private financial advisory firm, Fisher Investments, in 1979, with just $250 in seed money. Today, Fisher’s company manages over $195 billion in total assets, and his personal net work exceeds $5 billion.

Fisher has cast his eye on current market conditions. In recent published note, Fisher points out the obvious headwinds in the current environment: “Fear of the impact of the tragic, grinding war in Ukraine and hot overseas inflation. Fear of the ‘tightening’ at central banks across the world hurting China’s export demand. And prolonged Covid restrictions in Shanghai and Beijing. All this and more has torpedoed global sentiment thus far this year.”

It’s a dark picture, true. But Fisher also sees hope ahead for investors, and that hope is part and parcel of the very pressures that investors are facing. He writes, “Beneath the sour surface lurk powerful positives… Their stealthy presence amid widespread gloom upends global recession fears and provides evidence that brighter days are ahead…” He describes the current conditions as “exactly the kind of broad pessimism that new bull markets are born in.”

Turning to Fisher for inspiration, we took a closer look at two stocks Fisher’s firm made moves on recently. Using TipRanks’ database to find out what the analyst community has to say, we learned that each ticker boasts a “Strong Buy” consensus rating from the analyst community and massive upside potential.

Revolve Group (RVLV)

We’ll start with an online fashion retailer. Founded in 2003, Revolve now offers more than 70,000 styles and items in apparel, footwear, accessories, and beauty products. The company uses a data-driven merchandising system, and in 2021 made 87% of its sales at full retail price.

Revolve saw $891 million in net sales last year, up 53% from $580 million in 2020. The strong sales trend is continuing, and even accelerating, this year; the 1Q22 top line came in at $283.5 million, the highest quarterly sales in the last two years – and up 58% year-over-year. The company’s earnings have been more volatile, with diluted EPS ranging from 22 cents per share to 42 cents per share in the past 8 quarters. The 30-cent result in 1Q22 was squarely within this range.

In other positive news from Q1, Revolve Group reported $53.8 million in cash flow from operations for the quarter, of which $52.7 million was free cash flow. The represented gains of 62% y/y, and caps a three-year free cash flow increase of 400%. The company’s strong cash flows are visible in the balance sheet, which holds $270.6 million in cash and liquid asset reserves as of the end of March, up 48% year-over-year.

It’s only natural that an e-commerce firm with strong sales fundamentals would attract notice from major investors, and Fisher, who already held more than 890K shares of RVLV, increased his stake in Q1 by ~811K, to a new total of 1,703,038 shares. At current prices, Fisher has $51.87 million invested in Revolve Group.

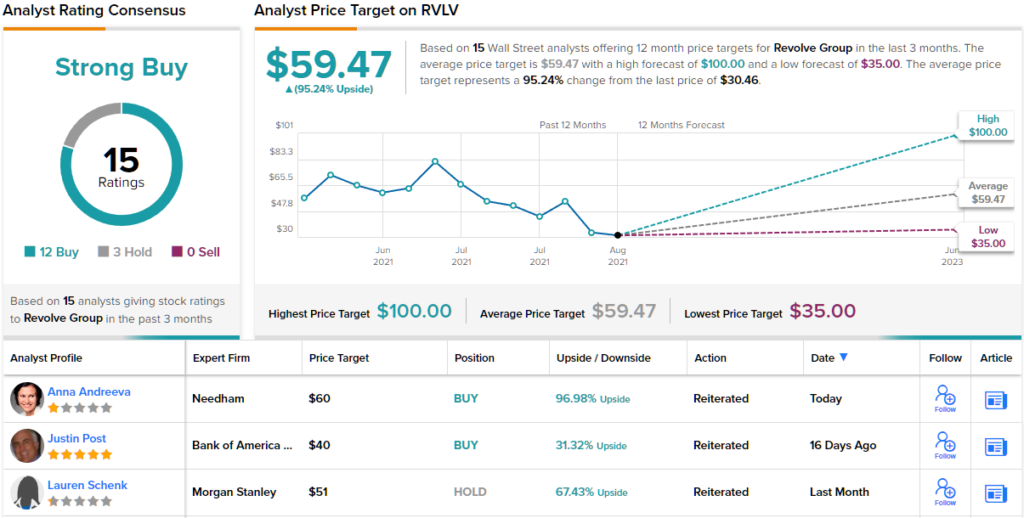

Fisher is far from the only bull on this retailer. Wedbush analyst Tom Nikic states, as his bottom line: “We believe the business has compelling growth prospects in the near-term (return to in-person social events) and over the long-term (current customer count only ~3% of the target demographic). Furthermore, we like that RVLV generates highly-profitable growth as well (DD EBIT margins). All in, we remain bullish this name, as one of the more compelling growth stories in our coverage.”

Nikic doesn’t just lay out an upbeat path for the company, he backs it with an Outperform (i.e. Buy) rating and $59 price target. Going by this target, shares are expected to climb ~94% higher over the one-year timeframe. (To watch Nikic’s track record, click here)

Overall, the analysts generally are willing to take bullish stands of RVLV. Of the 15 recent reviews posted for this stock, 12 are Buys against just 3 Holds, for a Strong Buy consensus rating. The stock is selling for $30.46 and its $59.47 average price target indicates ~95% upside in the next 12 months. (See RVLV stock forecast on TipRanks)

Rocket Lab USA (RKLB)

From e-commerce we’ll move over to space flight. While Elon Musk’s SpaceX has hogged the headlines in the private venture space industry, it’s far from the only game in town. Rocket Lab is a space-launch company with a reusable small launch vehicle, the Electron, capable of inserting 300kg payloads into low Earth orbit. The Electron rocket is the only reusable small launch vehicle currently in service, and is in high demand – Rocket Labs has made 26 successful launches since introducing it, and deployed 146 satellites.

Rocket Lab is working to expand the launch options available to customers with the development of the Neutron launch vehicle. The Neutron, when complete, will operate in the 8-ton payload class, and will be able to launch cargos capable of leaving Earth orbit altogether. The US Space Force last year awarded Rocket Lab a $24 million contract for development work on the upper stage of the Neutron vehicle.

In addition to its launch vehicle, Rocket Lab offers customers access to the Photon spacecraft, a small-size configurable vehicle launched as the upper stage of an Electron rocket. The Photon can be optimized for low- and mid-altitude Earth orbits, geosynchronous orbits, or even extra-Earth flights to the Moon or the nearby planets Mars and Venus. There are currently 2 Photon spacecraft orbiting Earth. In late May, Rocket Lab announced that its customer Varda Space Industries, which had previously ordered 3 Photon spacecraft, had increased its order to 4.

Also in May, Rocket Lab announced that the CAPSTONE spacecraft, a joint operation undertaken on contract with NASA, had been delivered to its New Zealand launch facility. Rocket Lab will now begin integrating CAPSTONE with the launch vehicle, as part of a long-duration NASA mission to the Moon.

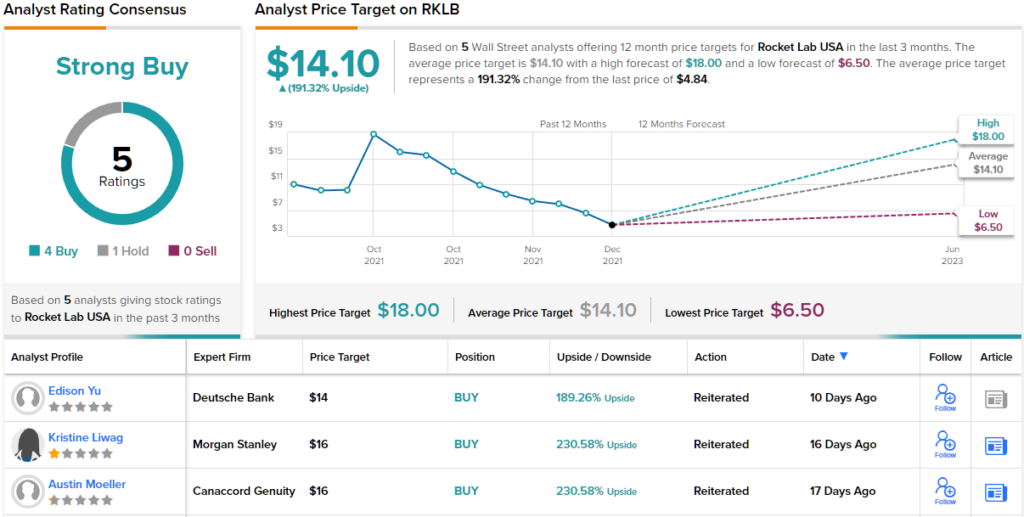

This space launch company has proved of interest to Fisher, who recently bought up 538,913 shares of RKLB. His stake in the company is worth $2.62 million at current share prices.

Rocket Lab has also caught the attention of Deutsche Bank analyst Edison Yu, who writes: “In our view, the company’s growth and margins across various business lines are set to inflect over the next year and its new larger Neutron rocket will be fully sold out for at least 2-3 years even before its maiden voyage. Moreover, we think its Space Systems segment remains unappreciated despite winning the landmark Globalstar/MDA contract which surprised many legacy competitors.”

“Looking ahead, the stock may be volatile due to tactical factors (growth sell-off, shift in shareholder base, etc…) but we think the enormous disconnect in valuation will likely compress relative to SpaceX which in the private market was reportedly seeking a $127bn valuation just a few days ago (RKLB now trading at only ~$2bn),” the analyst added.

Yu brings a Buy rating for the stock along with his comments, and his price target here, at $14 per share, suggests ~189% upside for the year ahead. (To watch Yu’s track record, click here)

His Wall Street peers are also upbeat on the prospects for Rocket Lab, as shown by the 4 to 1 breakdown in analyst reviews, favoring Buys over Holds and supporting a Strong Buy consensus view. The shares are selling for $4.86 and the $14.10 average price target implies a high 191% upside this year. (See RKLB stock forecast on TipRanks)