Following the wild ride that was 2020, where does the market go from here? Major strides have been made in the COVID-19 vaccine race, yet the near-term picture remains unclear, blurred by the virus’ resurgence and the stimulus stalemate on Capitol Hill.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

In times like these, the investing greats can serve as a source of inspiration, namely billionaire Israel “Izzy” Englander.

Who exactly is Englander? The legend, who started trading stocks when he was in high school, began his career interning at investment firm Oppenheimer, later going on to purchase a seat on the American Stock Exchange, where he would serve as a floor broker, trader and specialist.

In 1989, along with Ronald Shear, Englander founded hedge fund Millennium Management. As evidence of his stellar track record, the guru took the $35 million the fund was started with and turned it into over $40 billion in assets under management. With his personal net worth clocking in at $7.2 billion, it’s no wonder Wall Street pays attention when Englander makes a move.

Bearing this in mind, our focus shifted to Millenium’s most recent 13F filing, which discloses the stocks the fund snapped up in the third quarter. Locking in on two tickers in particular, TipRanks’ database revealed that both names score a “Strong Buy” analyst consensus. What’s more, the analyst community sees massive upside potential in store for each.

G1 Therapeutics (GTHX)

Bringing a deep understanding of the biology of cancer and extensive drug discovery experience to the table, G1 Therapeutics works to develop therapies that could potentially improve the lives of patients battling the deadly disease. Ahead of a key regulatory decision, the Street is pounding the table on this name.

During the third quarter, Englander and Millennium picked up a new stake in GTHX. Pulling the trigger on 555,937 shares, the value of the holding comes in at $6,421,000.

Turning to the analyst community, Needham’s Chad Messer tells clients that he has high hopes ahead of the February 15 PDUFA date for trilaciclib, its therapy designed to improve outcomes for cancer patients treated with chemotherapy. The therapy’s NDA was accepted in August for Priority Review based on results from three randomized clinical studies in small cell lung cancer (SCLC), with the FDA indicating that it doesn’t plan on holding an advisory committee (AdComm) meeting.

As trilaciclib is the first CDK4/6 inhibitor to be used to treat chemo-induced bone marrow toxicity, Messer argues that the lack of an AdComm is “meaningful.” Expounding on this, he stated, “We believe this reflects the agency’s appreciation of the unmet need, comfort with the safety profile of the CDK4/6 class, and efficacy profile of trilaciclib.”

GTHX will also focus on the inclusion of trilaciclib into NCCN guidelines. It should also be noted that a Phase 3 pivotal study evaluating the candidate in metastatic colorectal cancer (mCRC) is set to kick off by year end.

Adding to the good news, GTHX and its partner, Boehringer Ingelheim, are preparing for the commercial launch of trilaciclib, with the companies covering approximately 2,500 treating oncologists and providing educational materials regarding the use of trilaciclib ahead of treatment and the benefits of multi-lineage preservation.

If that wasn’t enough, the rintodestrant (its selective estrogen receptor degrader (SERD) in development for the treatment of estrogen receptor-positive (ER+) breast cancer) plus palbociclib combination study was able to wrap up enrollment earlier than expected, reflecting “the appeal of an all-oral treatment regimen during a global pandemic,” in Messer’s opinion. With a data readout slated for Q2 2021, the analyst believes a “positive readout could prove to be a significant value driver.”

In line with his optimistic approach, Messer reiterated a Buy rating and $74 price target, indicating 417% upside potential. (To watch Messer’s track record, click here)

Are other analysts in agreement? They are. Only Buy ratings, 3 to be exact, have been issued in the last three months. Therefore, the message is clear: GTHX is a Strong Buy. Given the $59 average price target, shares could rise 312% in the next year. (See GTHX stock analysis on TipRanks)

Epizyme (EPZM)

Also fighting the good fight against cancer, as well as against other serious diseases, Epizyme wants to find new treatments through novel epigenetic medicines. Even though the company faces headwinds with regard to its recent product launch, several members of the Street believe big things are in store.

Millenium purchased 461,258 shares during the third quarter, with the buy reflecting a new position for the hedge fund. As for the value of the holding, it lands at $5,503,000.

Writing for Wedbush, 5-star analyst David Nierengarten points out that the pandemic has limited oncologist visits, and therefore, Tazverik (the company’s follicular lymphoma treatment) sales were lower than he expected. He points out that “the pandemic shifts the launch curve to an ‘incidence model’ rather than a prevalence model, as there is a limited patient pool to draw from if they are delaying office visits,” with patients waiting to seek treatment until they experience symptoms of progression.

Additionally, although the launch is virtual and physician awareness is high, physicians are opposed to prescribing a new medication without examining the patient in person. That being said, Nierengarten remains optimistic about the therapy.

“Despite these headwinds, Tazverik came close to meeting our estimates, and it is gaining market share, including seeing initial sales in second line. We expect more meaningful second line sales to begin in 2021, and have more gradually incorporated them into our launch curve,” the analyst explained.

When it comes to the time on therapy, Nierengarten argues it’s too early to come to any conclusions. However, he highlights the fact that durability of response was relatively long and patients were treated past progression in the registration study. “Furthermore, the headwind against switching therapies turns into a tailwind of Tazverik maintenance once a patient is on therapy. This will likely contribute more meaningfully to 2H21 revenues and potential revenue outperformance,” he added.

Summing it all up, Nierengarten commented, “At current levels, we believe investors are too negative on Tazverik’s potential and patience should be rewarded.”

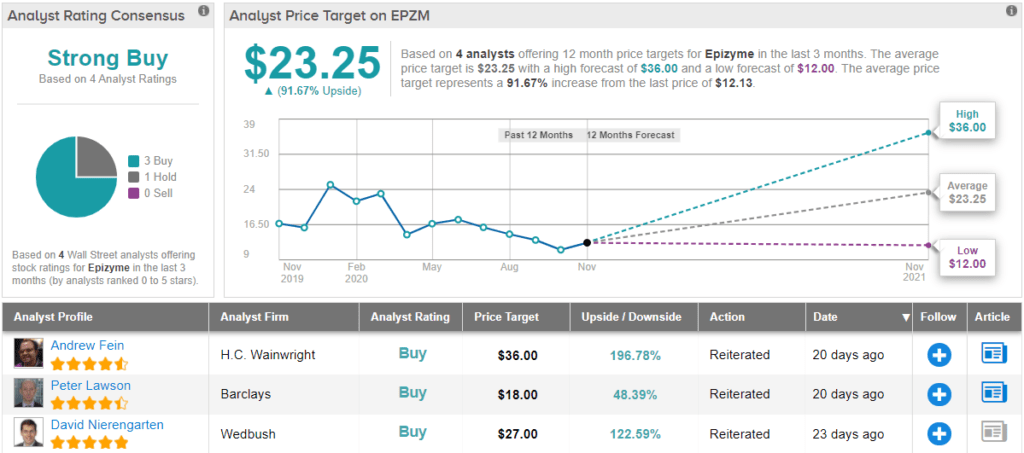

Based on all of the above, Nierengarten sides with the bulls, reiterating an Outperform rating and $27 price target. This target conveys his confidence in EPZM’s ability to climb 122% higher in the next year. (To watch Nierengarten’s track record, click here)

Most other analysts echo Nierengarten’s sentiment. 3 Buys and 1 Hold add up to a Strong Buy consensus rating. With an average price target of $23.25, the upside potential comes in at 91%. (See EPZM stock analysis on TipRanks)

To find good ideas for healthcare stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.