Electric vehicles (EVs) have become the car sector’s fastest growing segment, more than doubling last year to reach 6.8 million vehicles globally. This gives EVs a market share greater than 8%, triple where it stood in 2019, before the COVID pandemic. The market has found support from political policy, but more importantly, from improvements in battery technology and manufacture that are slowly making EVs more competitive on price.

Not wanting to miss out on a compelling opportunity, billionaire investing legend Israel “Izzy” Englander has pulled the trigger on three small-cap EV stocks, taking multi-million dollar stakes while the industry is still young. Englander got his start in the stock market more than 45 years ago, and in 1989 he founded his own hedge fund, Millennium Management, with $35 million in seed money. Today, Millennium holds a total of $56 billion in assets under management.

So let’s take a look at Englander’s EV moves. According to TipRanks’ database, these are stocks with Buy ratings, and offering investors triple-digit upside potentials. We can take a closer look at them, and at the analyst commentary, to find out what else may have brought them to Englander’s attention.

REE Automotive (REE)

First up is REE Automotive, a company taking an innovative approach to EV design – and automobile design generally. REE is taking advantage of new, high-tech electric motors and drive tech to change the way that the vehicle chassis and drive train interact. By putting separate motors on each wheel, the company has created a chassis that delivers more power and higher carrying capacity on a smaller footprint without sacrificing performance. The result is an EV design that can carry more batteries, allowing for more cargo or passengers over longer ranges.

REE’s drive train and chassis design also allow for another advantage: easy customization. The chassis is essentially flat platform with an electric-driven wheel at each corner; it can readily be scaled up or down to accommodate passenger vehicle or delivery truck models, and can accept a wide range of body designs and styles. So far, REE has developed its platform into two marketable vehicles; the P7-B box truck, designed for mid- and last-mile delivery fleets, and the Proxima walk-in step-van, optimized for urban last-mile use.

Both the P7-B and the Proxima models are undergoing customer evaluations, and the company reports that progress is ongoing, with positive feedback from customers. Both commercial EVs are described as ‘on track and on budget.’

That last point is important, as REE is still pre-revenue, and dependent on available liquidity to fund operations. REE has, as of the end of 2Q22, $206.8 million in cash and liquid assets on hand.

This makes for an interesting company, with a clear path forward – and Englander would agree. His firm bought 3,383,946 shares of REE in the last quarter, and now holds over 3.893 million shares in the company. The buy boosted Millennium’s holding by more than 660%, and the firm’s stake is worth $4.44 million.

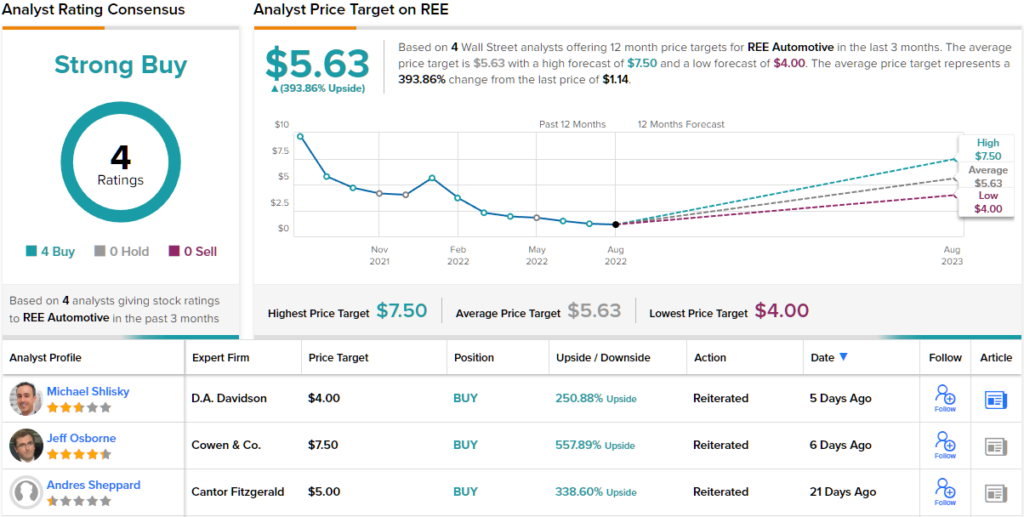

Cowen analyst Jeff Osborne is also impressed with REE, and takes a bullish line when he writes: “We remain positive on REE as the company has been able to stay on track with guidance and reach its set milestones while managing cash burn. REE’s differentiation lies within its focus on niche commercial EV segments… REE is still on path to reach its YE22 target capacity of 10,000 vehicles within its Coventry, UK facility, while simultaneously building out its new integration center in Austin, Texas. In the near term we would expect investors to focus on Proxima demand following the testing of REE’s fleet and feedback from customer evaluations once P7-B deliveries begin in Europe.”

In-line with his bullish stance, Osborne rates REE an Outperform (i.e. Buy), and his $7.50 price target indicates room for a robust 552% upside in the coming year. (To watch Osborne’s track record, click here)

Overall, 4 analysts have weighed in on REE recently, and they have all given the stock positive ratings – making the Strong Buy consensus rating unanimous. The shares are priced at $1.14, and their $5.63 average price target implies ~394% upside on the one-year time horizon. (See REE stock forecast on TipRanks)

Beam Global (BEEM)

The next Englander pick we’ll look at is Beam Global, a company that has taken a lead role in clean energy tech, designing and distributing a range of products for EV charging, energy storage, and energy security. Beam’s products are available in 96 US cities across 13 states, as well as 121 countries globally. The company’s chief products are the EV ARC, a rapidly deployable, solar-powered, off-grid, EV charging station; the Solar Tree, a larger scale charging deployment for medium- and heavy-duty vehicles; and the Beam AllCell, a solution for high-performance energy storage. The company also offers the ARC Mobility Trailer, designed to rapidly relocate and redeploy the EV ARC system.

Beam’s flagship product is the EV ARC. The ‘ARC’ stands for autonomous renewable charger, a fitting name for a stand-alone EV charger unity that is independent of the electric grid, drawing its power from built-in solar panels. The EV ARC can be deployed in or around existing parking spaces, can accommodate the charging ports and cords of most existing EV models, and one system can charge up to 6 vehicles at one time. The system is designed to be deployed without major construction work.

In recent months, Beam has announced several new contracts, including one with the State of California Department of General Services for several configurations of the EV ARC and ARC Mobility Trailer. This announcement expands on previous California state contracts awarded to Beam. In another announcement, Beam made public a new partnership with Volvo Construction Equipment, allowing Volve CE’s dealer locations in North America to bundle EV ARC systems with Volvo electrical equipment. The combination will allow end-use customers to deploy EV ARCs in conjunction with Volvo’s construction of electrical fittings. And finally, Beam announced in late July that it had received a $927,000 order for energy storage solutions on a fleet of autonomous delivery drones.

In short, Beam is on the way up. The company’s 2Q22 revenue, of $3.7 million, was up 75% year-over-year, and the second-highest in the company’s history. Beam also had $13.8 million in cash and liquid assets at the end of Q2.

Beam has clearly caught the eye of Izzy Englander. The Millennium firm bought up 132,814 shares of the company, opening up a new position for the hedge fund in Q2. Millennium’s holding in Beam is worth $1.95 million at current prices.

Englander is far from the only bull on Beam. B. Riley analyst Christopher Souther states, as his bottom line: “We believe Beam will continue to see improved operating leverage as it grows production volumes, and gross profitability increased 4% Y/Y in 1H22 despite inflationary and supply chain challenges. We think the company is well suited to carve out a needed niche in EV charging infrastructure, especially given recent increased focus on energy resiliency, and see underappreciated potential in adjacent electrical market opportunities as evidenced by Beam’s construction equipment partnership with Volvo.”

Following from his comments, Souther rates BEEM a Buy, and sets a $23 price target that indicates room for 58% share price growth over the next 12 months. (To watch Souther’s track record, click here)

The rest of the Street supports Souther’s thesis. In fact, the average price target is even more upbeat; at $29.33, the figure is expected to yield 12-month returns of ~101%. The stock boasts a Moderate Buy consensus rating, based on 3 Buys and 2 Holds given in the past 3 months. (See BEEM stock forecast on TipRanks)

ElectraMeccanica Vehicles (SOLO)

Last but not least is ElectraMeccanica, an EV maker that is bringing a truly unique vehicle to market. This company builds and markets the Solo – from which it also gets its stock ticker – a small, single-seat EV designed for urban commuter use. The vehicle features two doors for easy parking anywhere, a trunk for small cargo loads, and an 80 mile-per-hour top speed over a 100 mile single-charge range. In short, it’s an EV designed for the city dweller. The company has also fitted out commercial versions for small-scale urban delivery use.

ElectraMeccanica has begun regular production of the Solo, to meet existing orders, and during the second quarter of this year, the company built 193 vehicles. This number was a company record, and was accompanied by delivery of 68 vehicles. ElectraMeccanica has established a network of showrooms on West Coast – in Oregon, San Francisco, and in Southern California, along with another in Phoenix, Arizona. Revenues in Q2 reached $1.55 million, up 48% from Q1, and up more than 5x year-over-year.

The company stated that it is beginning to scale up production, which has been increasing steadily over the past year. The company has $195 million in cash and other liquid assets to support its operations.

The Solo car has quickly built a reputation as an innovative urban commuter EV, and Englander’s curiosity was clearly piqued. The legendary investor already held a small stake in this company, but he increased it by over 2,200%, or 1,069,368 shares, in the last quarter. This brings his total holdings in SOLO to 1,116,375 shares, now worth $1.66 million.

ElectraMeccanica has also caught the attention of Stifel analyst J. Bruce Chan, who writes: “For 2H22, we are seeing signs of improved fluidity and think a 100 vehicle/month flow rate is reasonable, but we are still tempering our outlook modestly given market uncertainty. 1H23 should look similar, but by the second half of next year, we anticipate contribution from EMV’s U.S. Assembly facility.”

“Customer deliveries were the major milestone of the past 12 months, and we believe commencement of U.S.-built vehicles will be the major milestone of the next 12 months. This environment has been challenging for most manufacturers, but with an asset-light footprint, modest production goals, and a unique market offering, mid-to-long term opportunity remains rich for [ElectraMeccanica], in our view,” the analyst added.

Chan goes on to give the stock a Buy rating and a $4.40 target price that implies a 197% upside over the next year. Chan’s is the only analyst review on record for this stock, which is currently selling for $1.48 per share. (To watch Chan’s track record click here)

To find good ideas for EV stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

Questions or Comments about the article? Write to editor@tipranks.com