Michael Burry’s fame spread far and wide after his exploits were documented in the Big Short – the book – and later the movie – that told the story of Burry’s success in betting against the housing market during the financial crisis of 2008. That was a move that turned out to be a hugely profitable one.

Burry went short then and hasn’t been shy in issuing repeated warnings on the current state of the market, either. In addition to some recent enigmatic tweets that hint at looming disaster, Burry has continually made bearish comments; stocks are in overvalued territory, high inflation is going nowhere and a ‘multi-year recession’ is coming, are just some of Burry’s arguments against growing optimism.

Yet, all the doom and gloom talk hasn’t stopped him from leaning into the stocks he thinks can take on whatever bearish scenarios lie ahead.

Using the TipRanks database, we’ve pulled up the details on two of his recent picks. Do the Street’s cadre of stock experts think these are also worth picking up right now? It looks like it; both are rated as Strong Buys by the analyst consensus. Let’s check the details.

Coherent Corp (COHR)

The first Burry-backed stock we’ll look at is laser systems specialist Coherent. The company is a well-known name in the world of engineered materials and optoelectronic component systems, as a designer and maker of precision equipment. Although the company has fulfilled this niche since being founded back in 1971, what is relatively new here is the name and ticker. Previously known as II-VI, last July, the company acquired Coherent, and adopted its name. The new addition brought its own laser technology to the table, thereby increasing the company’s value proposition.

The integration of the new addition appears to be going well, as was evident in the results for the second quarter of fiscal 2023 (December quarter). Revenue grew by 70% year-over-year to a record $1.37 billion, meeting Street expectations, while organic revenue growth increased by 23%. The also company showed a backlog of $2.9 billion, amounting to a 68% year-over-year increase. On the bottom-line, adj. EPS of $0.95 beat the analysts’ call for $0.93.

As for Burry’s involvement, he opened a new position during the quarter by purchasing 150,000 COHR shares. These are now worth about $6.7 million.

Although the company warned of the potential adverse impact of macroeconomic conditions on some parts of the business during the second half of its fiscal year, Cowen analyst Paul Silverstein is undaunted and thinks investors are underestimating the potential here.

“We exited the quarter with unchanged conviction as to significant upside potential for COHR’s long-term revenue growth and margin structure and thereby EPS and cash flow— significantly beyond investor expectations… Our long-term view remains unchanged based on our unchanged view as to strong secular demand trends across end markets and strong company-specific execution and as to investors’ underappreciation of COHR’s strategic vision and operational excellence,” the 5-star analyst wrote.

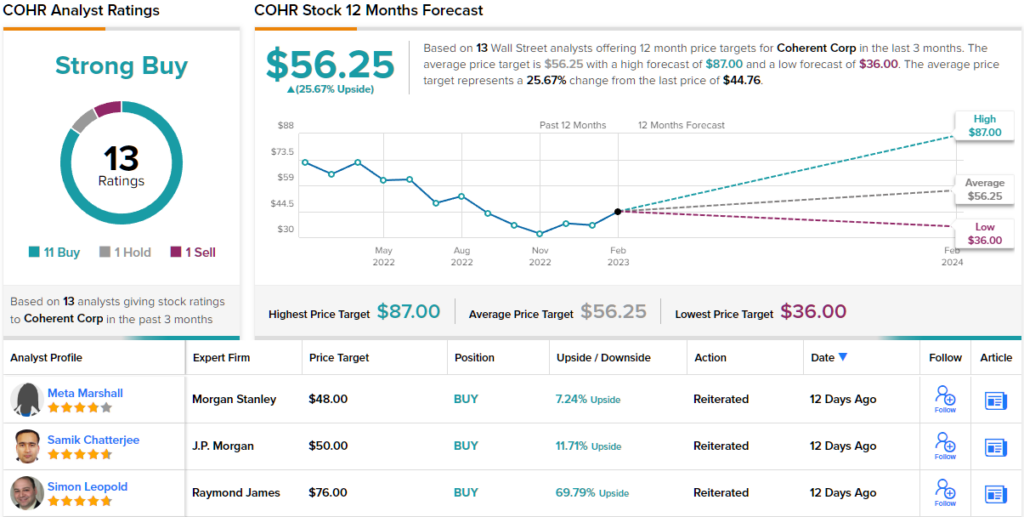

These comments underpin Silverstein’s Outperform (i.e., Buy) rating and $87 price target. What’s in it for investors? Potential upside of a hefty 94% from current levels. (To watch Silverstein’s track record, click here)

Most on the Street agree with Silverstein’s stance; the stock claims a Strong Buy consensus rating, based on 11 Buys vs. 1 Hold and Sell, each. The average price target stands at $56.25, suggesting the shares will move ~26% higher over the coming months. (See Coherent stock forecast)

MGM Resorts (MGM)

The next stock Burry is betting on offers something completely different. MGM Resorts is a global hospitality and entertainment company offering a wide array of services; these range from top-notch casinos and hotels to live and theatrical entertainment events to a host of nightlife and retail options. Its lineup includes some of the most known resort brands in the business, including Bellagio, MGM Grand, ARIA, and Park MGM, and in total, the company boasts 29 distinct hotels and destination gaming options in the United States and Macau.

Of course, this is an industry that was hit hard during the pandemic but MGM’s bounce back has been impressive. In the recent Q4 report, the company generated $3.6 billion in revenues, representing an 18% year-over-year increase and bettering Street expectations of $3.35 billion. Making up the bulk of the sales, Las Vegas strip revenues reached $2.3 billion, amounting to a $500 million increase compared to the same period a year ago. The company showed a loss per share of $1.53, also trumping the Street’s forecast for EPS of -$1.57.

The company said the outlook for 2023 looks bright and highlighted the ongoing recovery in Macau. During the quarter, MGM also repurchased shares worth $352 million, bringing the year’s total repurchases to $2.7 billion.

Burry must have felt satisfied; during the fourth-quarter he opened a new position in MGM. He bought 100,000 shares, now worth north of $4.30 million.

Singing MGM’s praises, Macquarie analyst Chad Beynon says the stock is a ‘top pick in the space.’

“With Vegas firing on all cylinders and Macau pent-up demand finally coming through, MGM delivered a strong 4Q beat with EBITDAR coming in 11% above consensus paired with positive forward commentary,” the analyst explained. “Given the strong Macau rebound, Vegas momentum and event calendar, and one of the strongest balance sheets in the space, we believe MGM is well-positioned to execute on capital returns as well as longer-term opportunities in Digital, New York and Japan.”

As such, Beynon rates MGM shares an Outperform (i.e. Buy) while his $55 price target implies one-year share appreciation of ~27%. (To watch Benyon’s track record, click here)

What does the rest of the Street have to say? As it turns out, other analysts are generally on the same page. 9 Buys and 2 Holds add up to a Strong Buy consensus rating. At $54.71, the average target is almost identical to Benyon’s objective. (See MGM stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.