Market swings come and go, but at the end of the day, individual stocks rise and fall based on their own fundamentals. Savvy investors know that tuning out the noise of macro trends allows them to zero in on the promising opportunities.

That mindset is especially useful when hunting for bargains – stocks that have taken a hit but aren’t out for the count.

Some shares slip for any number of reasons, yet Wall Street’s analysts still see them as Strong Buys. In other words, they’re temporarily undervalued, offering investors the chance to load up at a discount.

Against this backdrop, Bank of America analysts have picked out names that feature currently depressed prices along with sound upside potential for the coming year. We’ve opened up the TipRanks database to look at the broader Wall Street take on two of these BofA picks; here are the details.

Vistra Energy (VST)

The first stock we’ll look at, Vistra Energy, is a utility-scale power company based out of Texas. Vistra is the US market’s largest competitive power generation company, with some 5 million customers and more than 41,000 megawatts of electric power generating capacity currently online. The company employs 6,800 people, 14 of its facilities have OSHA VPP star ratings, and it boasts a market cap of $43 billion. Vistra’s power facilities are based on a variety of technologies, including natural gas, coal, nuclear, and solar. The company also has a stated commitment to the development of zero-carbon electricity, of which its nuclear power systems – the nation’s second largest such network – are a vital part.

Vistra has been working to expand its power portfolio, especially in the non-fossil fuel areas. In March of last year, the company acquired important nuclear power assets, totaling 4 gigawatts, from Energy Harbor, and expanded its customer base by 1 million. More recently, this past December, the company connected two new utility-scale solar projects to the grid. Both of these new solar projects are located in Illinois.

Electricity providers, especially utility-scale companies that can provide large amounts of power on long-term contracts, have been beneficiaries of the recent boom in AI. The new tech requires power-hungry data centers to function, and power companies like Vistra are strongly positioned to meet that demand. However, these same power companies have faced uncertainty regarding the regulations around special electricity deals – exactly the kind of deals that data center firms want to sign.

That uncertainty has created a headwind for the power companies – and in recent weeks, they have felt pressure on their stocks. Additionally, anxiety about the strength of the AI trend has also impacted electricity producers’ stocks since they supply power to data centers. The result: Vistra’s shares are down 40% from the peak they reached in January.

The stock’s retreat has coincided with Vistra actually reporting sound financial results. The company released its full-year 2024 results last month, and showed a top line of $17.22 billion, up 16.5% year-over-year and some $70 million better than had been expected. The company realized a net income from ongoing operations of $2.93 billion, up from $1.50 billion in the prior year. For Q4, the net income from ongoing operations came to $542 million, up from the $155 million loss reported in 4Q23.

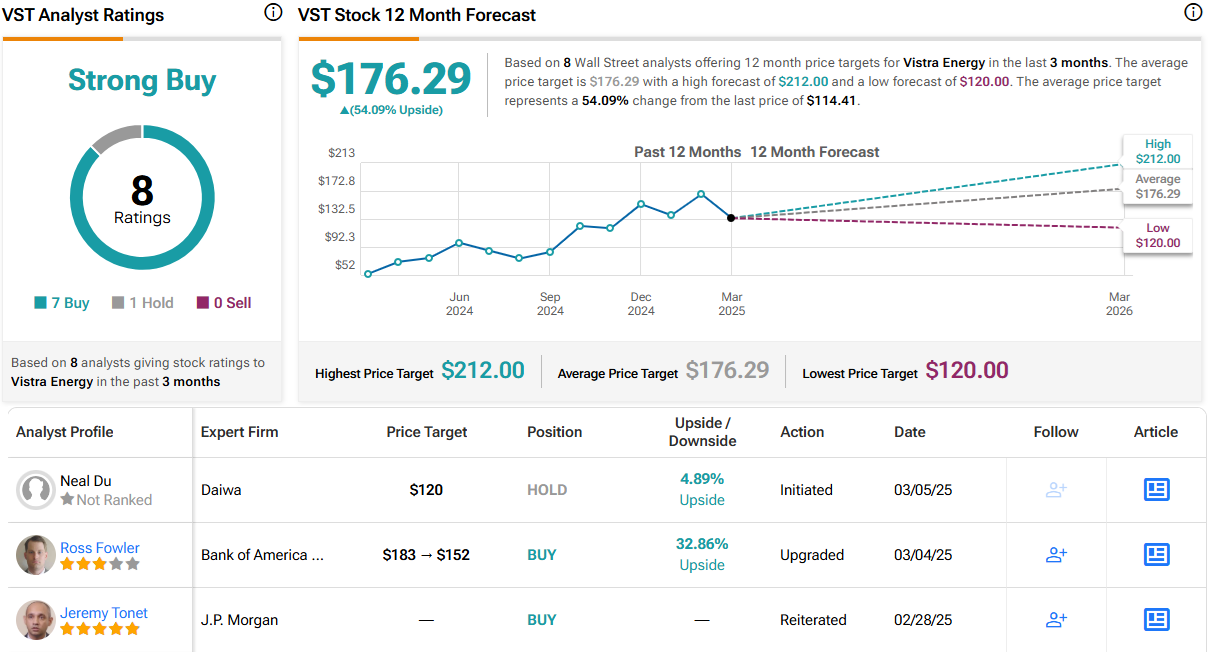

Ross Fowler covers this stock for Bank of America, and he is upbeat about Vistra’s prospects this year. Explaining his stance, Fowler writes, “Vistra has a competitive residential retail business in Texas and is the largest power generation company in the US. We believe the valuation of Vistra’s base business offers significant upside after the stock’s decline. Along with this, datacenter co-location clarity is likely in the coming months and this could be the catalyst to secure higher revenues.”

Fowler goes on to put a Buy rating on VST shares, with a price target of $152 that suggests a 33% upside potential for the next 12 months. (To watch Fowler’s track record, click here)

The Strong Buy consensus rating on Vistra’s stock is based on 8 recent reviews that include 7 Buys to 1 Hold. The shares are priced at $114.41, and their $176.29 average price target is even more bullish than the BofA view, implying a one-year gain of 54%. (See VST stock forecast)

Credo Technology Group (CRDO)

Next up on our look at Bank of America’s picks is Credo Technology Group, a tech company deeply involved in networking and connectivity. The company has defined itself as a provider of high-speed bandwidth solutions for wired connections in data infrastructure. Its products include various vital components of wired network systems, such as high-end line cards, optical DSP chips, and active electrical cables. The company is also known for its semiconductor chip designs and is a leader in serializer-deserializer (SerDes) technology.

Credo was founded in 2008 and has grown to become a $7.8 billion player in the tech world. The company has benefited in recent years from several high-profile trends in tech. The expansions of cloud computing, artificial intelligence, IoT, streaming video, and 5G wireless have all put a premium on data infrastructure – which is exactly the tech that Credo develops.

We should note here that Credo saw strong gains in share price heading into this year, but that year to date the stock is down by 37%. The fall comes on a combination of worries that CRDO is overvalued and that the company, despite its strong reputation, faces competition from industry giants such as Broadcom and Marvell.

Investors can take heart, however, from Credo’s financial performance. In the company’s last financial report, which covered fiscal 3Q25, Credo delivered top- and bottom-line beats along with solid guidance for fiscal Q4 revenue. In fiscal 3Q25, the company saw revenue of $135 million, up an impressive 154% year-over-year and $14.64 million better than the forecast. The quarterly earnings came in at 25 cents per share by non-GAAP measures, 7 cents better than the estimates.

Looking ahead to fiscal 4Q25, Credo expects revenues to keep climbing, into the range of $155 million to $165 million. The company has had solid successes with hyperscale customers, and 86% of the Q3 revenue came from Amazon Web Services. Credo expects to expand on its hyperscale successes going forward.

This caught the attention of Bank of America’s Vivek Arya, an analyst who ranks in the top 4% of Wall Street stock pros. He says of Credo, “We continue to see a strong AEC ramp into FY26, with multiple hyperscale customers (two new customers in discussion on top of existing AWS, Microsoft, xAI) on track to adopt AECs for intra-rack and over time for <7m rack-to-rack solutions. While we highlight growing competition in the AEC market (MRVL/AVGO), CRDO is diversifying its product portfolio into adjacent optical DSPs, line cards, and PCIe-based retimers/AECs which are expected to ramp starting F2H26/CY26. Despite a growing product mix, we also note CRDO could sustain the current 63-65% GMs as scale increases and AWS contra-revenue dilution impact subsides.”

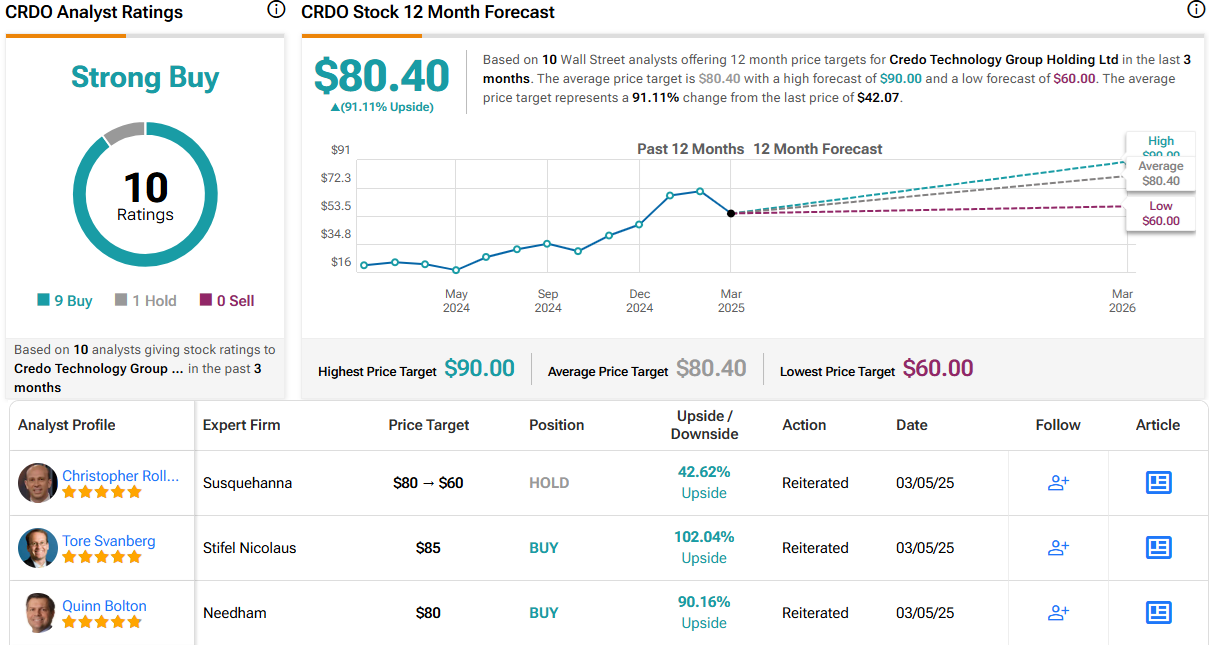

The 5-star analyst rates this stock as a Buy, and he complements that with a $75 price target, pointing toward a 78% upside potential in the next 12 months. (To watch Arya’s track record, click here)

There are 10 recent analyst reviews here, including 9 Buys and 1 Hold, for a Strong Buy consensus rating. Credo’s shares are selling for $42.07, and their bullish $80.40 average target price implies an upside potential of 91% waiting in store for the coming year. (See CRDO stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.