Reading tea leaves blurs the lines between art and science – especially on the investment scene, where the analysts combine historical insight, statistical savvy, and gut intuition to find the main chances that the markets will take.

Covering the markets from Bank of America, the firm’s equity strategist Savita Subramanian focuses more on the scientific approach – to suggest that the current bull has some more distance left to run. She noted that BofA’s Sell-Side Indicator, a proprietary data tool that tracks the Street’s equity allocation recommendations, hadn’t yet hit the top, where high levels would start triggering sell notes.

Pointing out the contradictions, Subramanian says of current conditions, “Sentiment has warmed vs. last year, but we don’t see levels of euphoria that bull markets typically end with.”

With room remaining at the top, it’s no wonder then that Bank of America analyst Michael Funk is tagging some stocks as buys going forward. We’ve used the TipRanks databanks to take a closer look at two of Funk’s choices, to find out where they stand, and just what the Street is predicting for them. Here are the details.

monday.com (MNDY)

We’ll start with monday.com, a firm that offers its customers a set of cloud-based work management products, used in everything from office system optimization and project management to CRM, marketing, and sales ops. The company caters to enterprise clients of all scales, an its cloud software is available through the ever-popular SaaS model. From the customer’s perspective, monday’s products allow a more efficient business process, and the company has found acceptance from some easily recognizable names, such as Uber and Coca-Cola.

Since its 2012 founding, monday.com has built a quality reputation based on its low code-no code platform, that makes it easy for users to customize their work management systems to better match their idiosyncratic needs and scales. The company has more than 225,000 customers, of whom 2,295 generate more than $50,000 each in annual recurring revenue and boasts a market cap of nearly $10.5 billion.

This company has expanded from its start-up roots, and today can claim a global reach. monday.com has offices in major financial and tech hubs around the world, including New York, Chicago, London, Tokyo, Tel Aviv, Sydney, and Sao Paulo. From those offices, the company manages its operations across more than 200 industries, and in over 200 countries and territorial jurisdictions.

On the financial side, this company reported recent 4Q23 results that were better than had been expected. The top line, at $202.6 million, was up 35% from the prior year and beat the forecast by $4.8 million, while the bottom-line earnings, a non-GAAP EPS of 65 cents, came in 33 cents over the estimates. At the same time, while the results were strong, the forward guidance was considered less impressive. The Q1 revenue outlook was set between $207 million and $211 million, in line with the $209 million analyst consensus. The shares fell sharply after the earnings release, mainly as investors appeared let down by that guidance.

Nevertheless, BofA’s Michael Funk remains onside, predicting that monday will see solid growth going forward. He writes of the company, “A leader in the $12.5bn+ collaboration software market, our analysis suggests MNDY is positioned to grow revenues at a CAGR of 30% through FY26. Our Buy rating is based on: 1) consensus estimates appear beatable, 2) market share gains will continue, 3) shares are inexpensive relative to rule of 50 (revenue growth + FCF margin) peers, and 4) the company’s march upmarket (increasing penetration of enterprises) and launch of new specialized/targeted products provide powerful levers for long-term growth.”

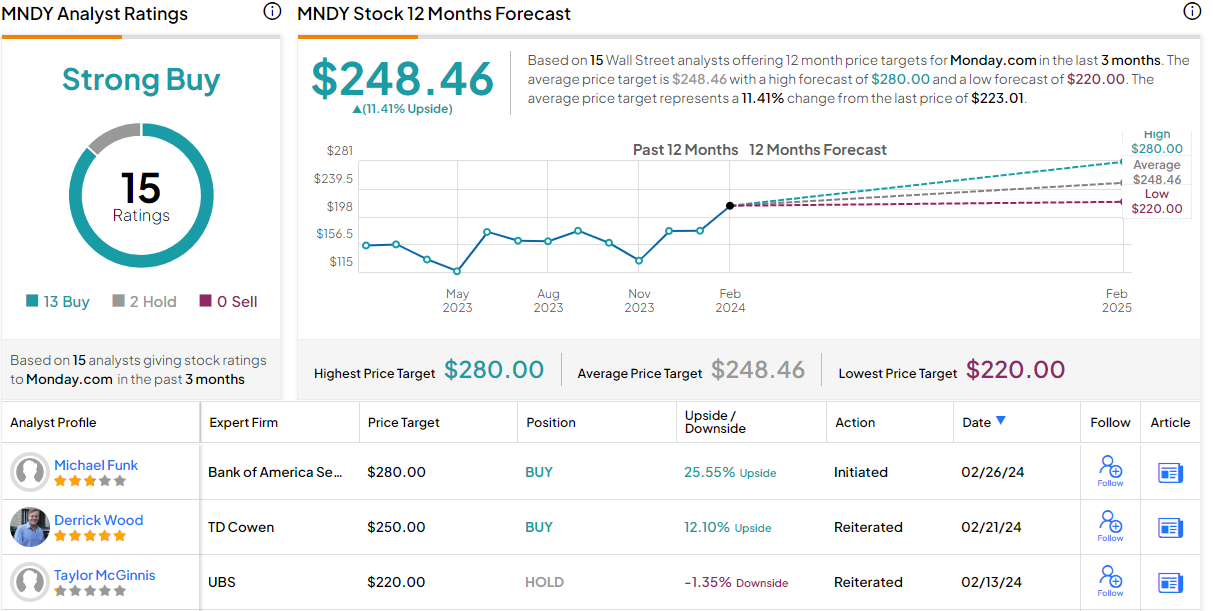

Quantifying his stance, Funk puts a Buy rating on the shares with a $280 price target that implies a 25% gain in the coming year. (To watch Funk’s track record, click here)

Overall, monday.com gets plenty of support on Wall Street. The stock’s Strong Buy consensus rating is based on 14 recent reviews that include 12 Buys to 2 Holds. The shares are priced at $223.01, and their $248.46 average price target suggests that MNDY will gain 11.5% in the next 12 months. (See MNDY stock forecast)

Asana (ASAN)

Next up is another software company. Asana is headquartered in San Francisco, and like monday.com above, it offers a platform and tools for work management. The firm entered the public trading markets in 2020, by a direct listing, and was valued at $5.5 billion at that time. After experiencing extremes of growth and contraction in 2021 and early 2022, the company today has a market cap of $4.21 billion.

Asana boasts that its platform gives the company’s enterprise customers a ‘smarter way to work.’ The tools have applications in marketing, operations, IT, and product departments, and have helped user firms improve both clarity and accountability. More recently, Asana has improved its own product offerings by integrating AI technology into the platform. Asana Intelligence can improve efficiency through the use of a semi-autonomous workflow management system.

There is strong demand in today’s digital workplace for reliable workflow management – and Asana has leveraged that to gain acceptance with some iconic names, and to steadily increase its revenue generation. The company can count such important firms as Amazon, Merck, and Dell among its customers, and over the past several quarters has seen gains at both the top and bottom lines in its regular financial results.

The last set of results made public, from fiscal 3Q24 which ended on October 31, 2023, showed a top line revenue total of $166.5 million, up 18% year-over-year and $2.4 million better than had been anticipated. On earnings, Asana ran a net loss, as it has consistently for a long time; the Q3 net loss came to 4 cents per share by non-GAAP measures; that said, this loss was narrower, by 7 cents per share, than the forecast – and it compared favorably to the 26-cent EPS loss recorded in the prior-year period.

While there is risk investing in a company that runs a regular quarterly loss, analyst Funk believes that those risks are worth taking here. He writes of this company and its stock, “We view Asana as a show-me story with an attractive risk-reward profile at current levels. It remains significantly underpenetrated within its Core existing customers (which have approximately 80mn total employees relative to paid seat count of 3mn), providing material runway for topline growth. We are 3% and 6% above consensus revenue estimates for FY25 and FY26, respectively, and argue that key risks (such as headcount reductions in tech) are well understood by investors.”

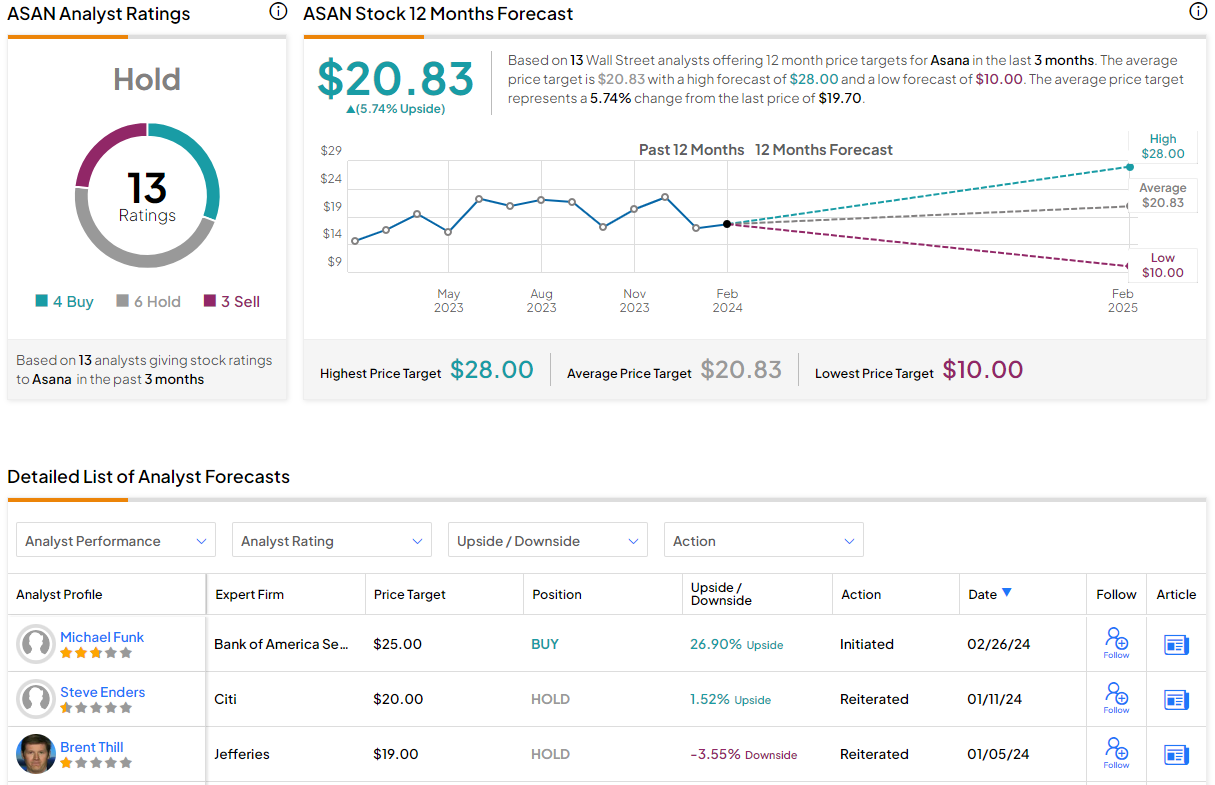

Putting these thoughts into a concrete recommendation, Funk gives ASAN a Buy rating, and he sets a $25 price target that shows his own confidence in a 27% upside potential on the one-year horizon.

That’s the bullish take. In general, the Street is less so. The analyst consensus rates the stock a Hold, based on 13 recent reviews that break to 4 Buys, 6 Holds, and 3 Sells. These shares are priced at $19.70 and their $20.83 average target price suggests a gain of 6% in the offing for the coming year. (See Asana stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

Questions or Comments about the article? Write to editor@tipranks.com