Global energy demand is surging, and at the heart of this revolution is the meteoric rise of AI technology. Fueled by the insatiable electricity needs of sprawling data centers, AI is reshaping the energy landscape with unparalleled speed. Mizuho Research predicts that by 2030, the power demand for data centers will skyrocket, tripling as AI applications expand their reach.

Meanwhile, Bank of America has seen this growing trend, and firm analyst Kalei Akamine has lit the fuse to buy two energy stocks that he believes are primed to outperform market expectations.

To dive deeper, we’ve turned to the TipRanks platform to uncover the details of these BofA recommendations. Let’s explore the picks and the insights driving Akamine’s bullish call.

Viper Energy (VNOM)

The first stock we’ll look at here, Venom Energy, is a $10-billion-plus partnership company, focused on owning, acquiring, and exploiting high production oil and natural gas properties in North America. The company operates in partnership with Diamondback, a major hydrocarbon production firm, and collects royalties on the fossil fuel wealth produced on its land holdings. We should note here that Diamondback owns a significant stake in Viper.

Viper’s goal is to generate an ‘attractive return’ for its own investors, and to that end the company focuses on its bottom line and its distributable earnings. Supporting this business, Viper had an ownership interest in 32,567 net royalty acres on September 30 of this year. Viper didn’t rest on that, however, and on October 1 the company closed on its acquisition of various mineral and royalty interest-owning subsidiaries of Tumbleweed Royalty, a move that increased Viper’s footprint to 35,634 net royalty acres. Of that total, 19,227 net royalty acres were operated by Diamondback.

Overall, on its property holdings, Viper has access to more than 10,700 horizontal producing wells along with another 1,125 line of sight wells. Average production from this portfolio came to 49,370 boe/d, up 2.4% from the prior year, and it was this production that supported Viper’s income and dividend payments.

Turning to the financial results, we find that Viper generated a total operating income of $209.6 million during 3Q24, the last period reported. This was $1.38 million better than had been expected, although it was down more than 28% year-over-year. At the bottom line, Viper’s non-GAAP earnings came to 49 cents per share, in-line with the forecasts.

After reporting these results, Viper declared a common stock dividend payment of 30 cents per share. This payment was supplemented by a variable dividend of 31 cents per share; together, the total payment annualizes to $2.44 per share, and gives a forward yield of 4.5%. We should note here that VNOM shares are up some 82.5% so far this year, far outpacing the NASDAQ index’s 30% year-to-date gain.

Setting out the Bank of America view, analyst Kalei Akamine is impressed by Viper’s ability to outperform, as well as its strong partnership with a major oil and gas producer. He writes of the company, “Unique to Viper is the support it has from a strong financial sponsor in Diamondback Energy (43% stake), the largest publicly-traded oil producer in the Midland Basin. More than half of Viper’s mineral rights derive from Diamondback operated leases – and they are expected to provide more than a decade of low single digit oil production growth… Our Buy on VNOM reflects our belief that relative outperformance will continue as VNOM’s production growth outlook differentiates the company vs other mineral peers.”

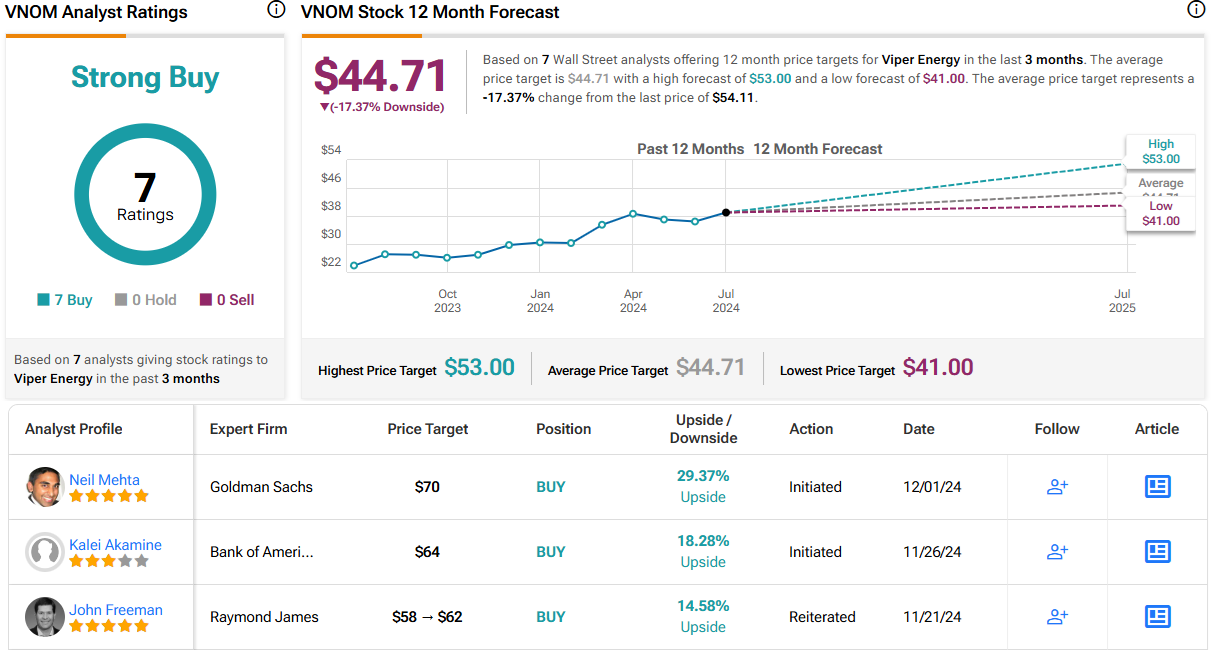

The Buy rating that Akamine gives on this stock is complemented by his $64 price target, suggesting a one-year upside of 18%. (To watch Akamine’s track record, click here)

Overall, the Street is bullish but its price targets are out of sync with the stock’s performance. VNOM shares have a Strong Buy consensus based on 7 unanimously positive analyst reviews. The shares’ $44.71 average price target, however, implies a one-year downside of 17% from the current trading price of $54.06. It will be interesting to see whether analysts increase their price targets or downgrade their ratings shortly. (See VNOM stock forecast)

Expand Energy (EXE)

Known as Chesapeake Energy until October 1 of this year, Expand rebranded itself after merging with Southwestern Energy. The combined company became one of America’s largest natural gas producers, with its headquarters in Oklahoma City and its operations in some of the richest natural gas production regions in the US. These include the Haynesville Shale of Louisiana, the Marcellus Shale in northeastern Pennsylvania, and the Marcellus and Utica shale formations of West Virginia and Ohio. With its Appalachian operations, Expand has access to one of the world’s largest natural gas plays, the Marcellus Shale.

In addition to its large footprint in natural gas, Expand is also well-positioned to operate in the fast-growing LNG sector—liquefied natural gas. LNG has become a vital part of the global energy economy, making it possible to transport natural gas across long distances in economically useful quantities, at affordable prices and scalable supplies. Expand describes itself as “ready” to participate in the US LNG sector, being the first US gas producer to certify two major production areas as responsibly sourced gas and the largest supplier to Gulf Coast natural gas liquefaction facilities. The company is capable of delivering approximately 1.5–1.8 bcfe/d of natural gas to those US liquefaction facilities.

Since its merger and rebranding action, Expand has released its financial results for 3Q24. This period ended on September 30, the day before the merger went into effect, and so covers the activities of the former Chesapeake Energy. The company delivered adjusted net income of $22 million, translating of 16 cents per share. That was 22 cents better than expected, coming in as a net profit rather than a loss. Expand is expected to release its first post-merger report in February of next year.

Bank of America’s Akamine covers this company and is especially impressed by Expand’s large footprint in the US natural gas market. He notes that the merger action which created the Expand rebranding was the culmination of Chesapeake’s strong merger strategy and writes of the consolidated company: “Since reemerging in 2021, Chesapeake (now Expand), has been on a deal spree to reposition its commodity exposure away from oil and move full-tilt towards natural gas. The Southwestern merger-of-equals is the fully formed version of this strategy. At 8bcf/d net and 12 bcf/d gross, Expand represents 11- 12% of total US supply, making it the face of an increasingly consolidated gas E&P landscape that we believe has increased agility to respond to market signals. This will be tested this winter as the market looks for producer discipline to adapt to winter demand.”

These comments support the analyst’s Buy rating, while his $114 price target shows confidence in a one-year upside potential of 15%.

Looking at the ratings breakdown, based on 8 Buys, 6 Holds, and 1 Sell, this stock has a Moderate Buy consensus view. However, the shares are selling for $98.96, and the average target price, $98.64, suggests the stock will stay rangebound for the time being. (See EXE stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.