Electric cars leader Tesla (NASDAQ:TSLA) cut prices on its EVs for a fifth time (so far this year) on Friday, knocking $5,000 off the stick prices of its top-priced Model S luxury electric sedans and Model X electric SUVs, subtracting $2,000 from the MSRP of Model Y electric crossovers, and snipping $1,000 off the price of the Model 3 — already Tesla’s cheapest electric car.

Maximize Your Portfolio with Data Driven Insights:

- Leverage the power of TipRanks' Smart Score, a data-driven tool to help you uncover top performing stocks and make informed investment decisions.

- Monitor your stock picks and compare them to top Wall Street Analysts' recommendations with Your Smart Portfolio

Investors mostly took the news in stride last week, selling off Tesla stock by only a fraction. Helping to keep investors on an even keel was a report out from Baird analyst Ben Kallo, which reiterated the analyst’s “outperform” rating on Tesla stock, as well as his $252 price target, implying about 36.5% upside from current prices. (To review Kallo’s track record, click here)

Why isn’t Kallo worried that repeated price cuts will savage Tesla’s profit margins, making an already pricey stock (Tesla costs 51 times earnings) look even more expensive as profits dwindle? As the analyst explains, Tesla has “lots of irons in the fire,” and lots of ways to grow its profits.

These include growing the company’s still-tiny energy generation and storage business (currently less than 5% of revenues and barely 1% of profits). As Kallo points out, Tesla recently received approval to become an “energy generator” in the United Kingdom, where it plans to work with independent power producers on projects to store renewable energy in gigantic batteries for later use. Tesla also announced — just today — that it will build a new factory in Shanghai to produce as many as 10,000 “megapack” utility-scale batteries per year.

That’s enough batteries to store 40 gigawatt-hours of energy, or more than six times more storage batteries than Tesla produced in all of 2022. So that certainly looks like one area in which Tesla could grow.

But according to Kallo, Tesla’s car business isn’t doing half bad in any case. So while Tesla can grow in energy, it doesn’t necessarily need to.

Last month the U.S. Treasury released more details on the criteria that EV companies must meet in order for buyers of electric cars and trucks to qualify for up to $7,500 in income tax credits under Congress’s 2022 Investment Reduction Act. Currently, only electric vehicles containing at least 40% U.S. “content” qualify for the credit, and this content requirement will rise over time (rising to 50% in 2024, for example, 60% in 2025, 70% in 2026, and 80% in 2027 and beyond). Requirements for EVs’ battery components are even tighter, beginning at 50% right now, and rising towards an ultimate goal of having all battery components being sourced either from the U.S. itself or from a “free trade partner” by 2029.

Even Tesla doesn’t think it can meet these standards for all its vehicles. In particular, rear-wheel drive Model 3 EVs probably won’t qualify for the full $7,500 credit — but other Model 3 configurations, and Model Ys as well, will. And these two models make up the vast majority of Tesla’s EV sales. For this reason and others, Kallo believes Tesla remains the carmaker best-positioned to navigate the strictures of the IRA and rack up sales as car buyers focus their attention on car models that qualify for the tax credits.

Additionally, Kallo points out that new fuel efficiency standards from the Environmental Protection Agency, which wants 60% of all car sale sin the U.S. to be EV car sales by 2030, will provide a tailwind to Tesla’s sales efforts.

Ultimately, the analyst concludes that Tesla stock is worth 25 times its estimate of 2026 earnings before interest, taxes, depreciation, and amortization (EBITDA), which according to the analyst’s calculations works out to $252 a share.

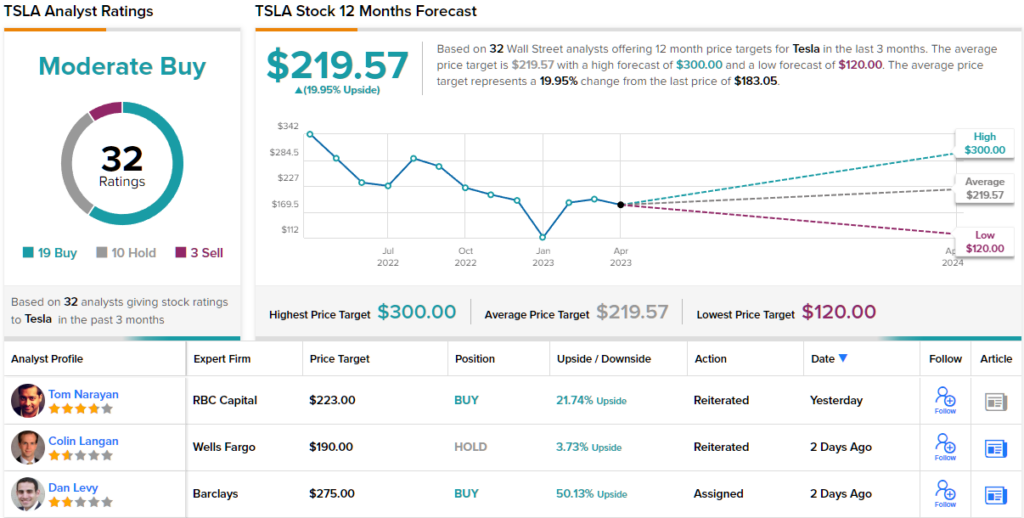

According to TipRanks, the world’s biggest database of analysts and research, there have been 32 analysts sounding off lately on TSLA, and their reviews include 19 Buys, 10 Holds, and 3 Sells, for a Moderate Buy consensus rating. (See TSLA stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.