In just a couple of weeks, Aurora Cannabis (ACB) has surged back to a rich valuation. The most recently news has the Canadian cannabis company entering the U.S. CBD space via an acquisition set to close in June.

The stock originally surged over 36% on the news leading to an increase in the stock value by over $500 million. Aurora Cannabis has cooled off some following the weak quarter from Canopy Growth, but investors need to realize that the CBD space in the U.S. is still held back by FDA restrictions.

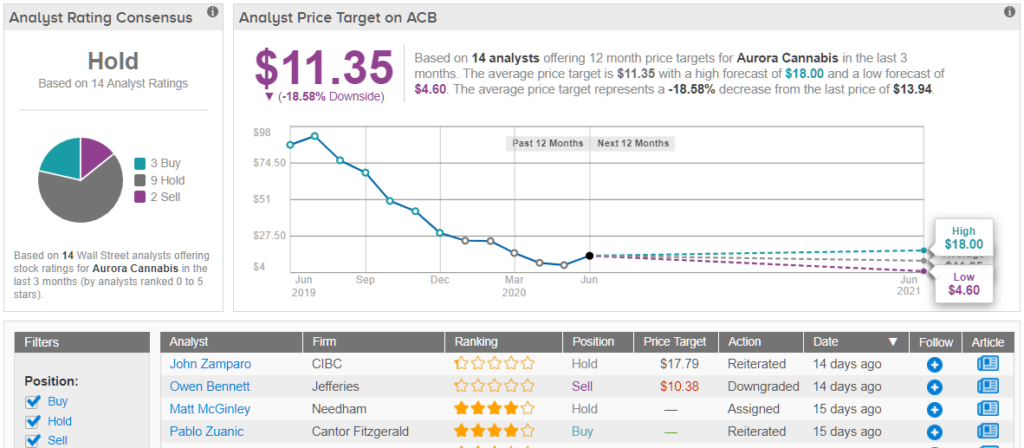

Wall Street is not convinced that Aurora’s reward is worth all the risk, especially when taking note that TipRanks analytics exhibit ACB as a Hold. Based on 14 analysts tracked in the last 3 months, only 3 rate the stock a Buy, while 9 say Hold and 2 suggest Sell. Indeed, the 12-month stock price forecast stands at $11.35, marking a nearly 19% downside from where the stock is currently trading.

U.S. CBD Deal

Aurora Cannabis bought Reliva, LLC for $40 million in stock plus an earn-out potential of up to an additional $45 million in stock and cash. The deal is forecast to be EBITDA accretive to Aurora principally due to the company having large EBITDA losses currently so any acquisition with positive EBITDA is accretive.

Cantor analyst Pablo Zuanic has Reliva pegged at $14 million in annual revenues from their distribution into 20,000 retail locations. The company is focused on topicals where sales have continued at specialty stores despite FDA restrictions on other CBD sales.

The CBD market is still projected to reach a high end of $24 billion in 2025 according to Brightfield, but the numbers are highly dependent on the FDA removing restrictions on dietary products. Currently, mass retailers are reluctant to sell products in this segment which Charlotte’s Web Holdings (CWBHF) has stated account for over 80% of sales in the CBD category. For this reason, CWH saw Q1 revenues decline 1% from 2019 levels.

The small deal allows Aurora Cannabis to enter the U.S. space without a large commitment or spending millions to establish a brand. The CBD space had over 6,000 brands entering 2020, so the large Canadian cannabis company can likely purchase more brands on the cheap to build up a strong revenue base while eliminating competition.

Too Far, Too Fast

Prior to reporting FQ3 results on May 14, Aurora Cannabis traded to a new low of $5.30. The stock rallied over 200% off the lows to reach recent highs at $18.

The cannabis company produced an impressive improvement in cash burn and a large reduction in EBITDA losses during FQ3. Better numbers in the June quarter should whittle down the EBITDA loss to somewhere below C$10 million leading up to a positive EBITDA in FQ1’21. Some positive EBITDA from Reliva should help, though the company has limited sales to impact the financials of Aurora Cannabis.

The issue here is that Aurora Cannabis still has a market cap of $1.6 billion with 112 million shares outstanding after this deal. The CBD upside appears limited in the near term so the sales upside from this entry into the U.S. appears rather small. The company won’t generate much more than $300 million in sales for FY21 with or without Reliva.

Takeaway

The key investor takeaway is that the valuation equation for Aurora Cannabis is far less interesting now as the market has pushed the stock up over 200% in a couple of weeks. The move to purchase a small CBD company in the U.S. is a smart move to enter the beaten down sector on weakness, but investors need to wait for the stock to cool off more before loading up on Aurora Cannabis.

To find good ideas for cannabis stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclosure: No position.