Some places in the world are just more attractive than others. For more than two centuries, as a territory and a state, the people of Ohio have reaped the benefits of their unique position. Situated between the water transport networks of the Great Lakes and the Ohio River, linked by road and rail to the East and West, and blessed with rich farmland and plenty of natural resources, Ohio has always been a combination of crossroads, granary, and industrial workshop in the US.

That’s an attractive economic backdrop, one that brings in people and jobs. The state boasts a patchwork of mid-sized cities and productive rural regions, which together have always made it a bellwether for the nation as a whole. And as Piper Sandler’s 5-star analyst, Alexander Twerdahl, points out in a recent report, Ohio’s panoply of advantages includes a solid banking sector.

Twerdahl believes that Ohio’s strong economy can lift its bank stocks higher, noting: “Ohio is home to a vibrant economy with industrial and manufacturing roots dating back to its location in the middle of the Rust Belt. The state’s abundance of fresh water sourced from Like Erie make it an ideal location for manufacturing and agriculture. Several Fortune 500 companies have recently announced manufacturing expansions in Ohio. Job growth in the state has led to an unemployment rate of just 3.7%… An attractive economic backdrop suggests to us that loan growth should continue to the extent there is appetite from the banks and that credit quality should remain strong in the near term…”

The analyst goes on to pick out 2 Ohio banking stocks that are ripe for gains. Are other analysts on the same page? We used the TipRanks database to find out. Let’s take a closer look.

First Financial Bancorp (FFBC)

Based in Cincinnati, this regional bank company operates 130 branches in Ohio, Indiana, Illinois, and Kentucky. The company also has a Commercial Finance business, which conducts commercial lending operations nationwide. First Financial Bancorp is a holding company, and its customer-facing operations are conducted through its subsidiary firm, First Financial Bank of Ohio. The Bank got its start in 1863, under the 56th charter granted by the terms of the National Bank Act of that year.

First Financial offers a full range of banking services to its customers. On the personal banking side, these include loan services, home equity lines of credit, and several options for checking accounts. On the business banking side, the bank offers solutions for business accounts, business checking, bill payment, and employee services.

As of the end of 2023, First Financial has some solid numbers to rely on. The bank, with a current market cap of nearly $2.08 billion, boasted $17.5 billion in total assets. It had $10.9 billion in total loans on the books and $13.4 billion in total customer deposits. For investors focused on returns, the company has consistently paid out a cash dividend every quarter since its founding over 160 years ago.

The most recent dividend declaration, made on January 23, was for 23 cents per share to be paid out on March 15. The bank has held its dividend at this level since 2019. The annualized rate, 92 cents per common share, gives a yield of 4.2%, more than enough to beat the current rate of inflation.

When examining the bank’s financial results, we find that First Financial reported bottom-line earnings of 62 cents per share in 4Q23, according to non-GAAP measures. This figure was a penny better than the estimates and was derived from solid banking performance. The company saw its outstanding loans grow by 10.7% year-over-year, or $286.4 million for the quarter, and total deposits increased by 12.9% year-over-year.

So it’s easy to see why Twerdahl is upbeat on FFBC. The analyst takes careful note of the stock’s relative value, and goes on to point out the company’s earnings.

“Over the past decade, FFBC has typically traded at about a 1x multiple discount to its proxy peer group, despite its superior profitability profile. That discount has recently widened to a 2x discount, which we think is unwarranted. Therefore, we expect FFBC to trade back closer to its historical discount at ~1x below peers, or ~11x… We like FFBC’s strong earnings profile and its asset sensitivity is already baked into our estimates. If we do not get as many rate reductions as the forward curve suggests, FFBC should be able to out-earn our current estimates. FFBC has a nice complexion of fee based businesses. The company has plenty of capital, and it doesn’t have the overhang of the $10B threshold,” Twerdahl opined.

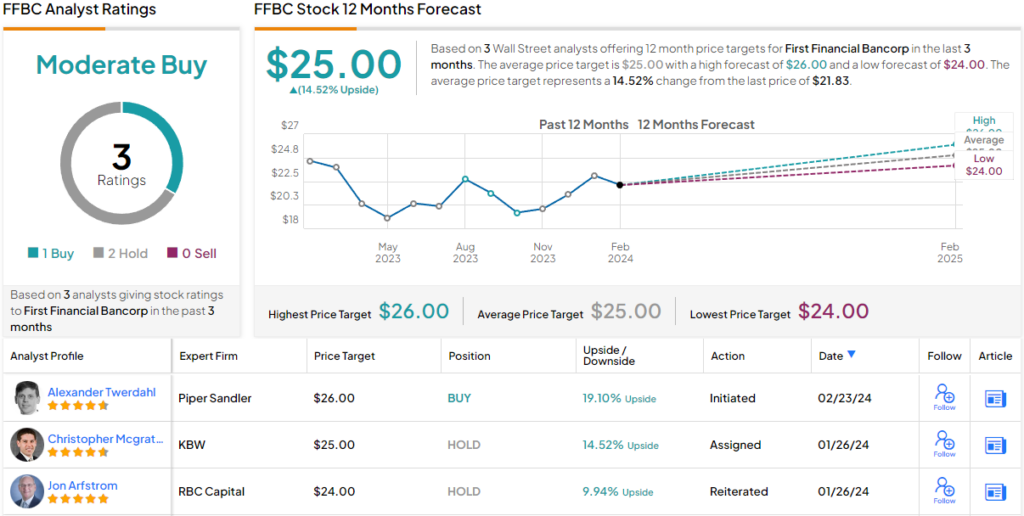

These comments back up the analyst’s Overweight (i.e. Buy) rating on FFBC shares, and his $26 price target implies a one-year upside potential of 19%. (To watch Twerdahl’s track record, click here)

The Wall Street consensus on this stock is a Moderate Buy, based on 3 recent reviews that include 1 Buy and 2 Holds. The shares are trading for $21.83 and their $25 average target price suggests an upside of 14.5% on the one-year horizon. (See FFBC stock forecast)

Peoples Bancorp (PEBO)

The second bank stock on our list today is Peoples Bancorp, based in Marietta, Ohio, having been domiciled there since 1902. The company operates through its subsidiary, Peoples Bank, providing an array of financial services to customers and clients in Ohio, Kentucky, West Virginia, Virginia, Maryland, and DC. The bank’s services include personal and business checking and savings accounts, as well as loans, investing services, and insurance products.

Peoples Bank provides these services through its network of branch locations, which numbered 150 at the last count as of December 31st, and can boast a strong set of basic numbers for a regional bank. The bank has a $1 billion market cap, and a total of $3.5 billion in assets under management. According to the books, Peoples Bank has $9.2 billion in total assets, $7.2 billion in total customer deposits, and $6.2 billion in total loans.

This Bancorp company brought in $112.5 million in total revenue during 4Q23, missing the forecast by $1.66 million, or approximately 1.5%. The revenue total was, however, up more than 25% year-over-year. At the bottom line, the bank company had earnings of 96 cents per share according to GAAP measures, and $1.04 per share according to non-GAAP measures. The non-GAAP earnings per share were 8 cents better than had been expected.

These results supported the bancorp’s regular share dividend, which was declared on January 22 for a February 20 payout at 39 cents per share. This was the fourth quarter in a row with the dividend at this level; the annualized payment of $1.56 provides a common share dividend yield of nearly 5.5%. Peoples Bancorp has been gradually raising the dividend payment since 2009.

Checking in again with analyst Twerdahl, we find him bullish on Peoples Bank’s earnings potential, saying of the stock: “We like PEBO’s strong earnings profile despite the step back that we are expecting in 2024. We like earnings growth into 2025, and expect to see operating leverage. If we do not get as many rate reductions as the forward curve suggests, PEBO should be able to out-earn our current estimates. The company has a nice complexion of fee based businesses. PEBO has plenty of capital. We do think that the $10B is an overhang and as a result of that overhang, we do not think that investors will not give the company a full peer-like multiple.”

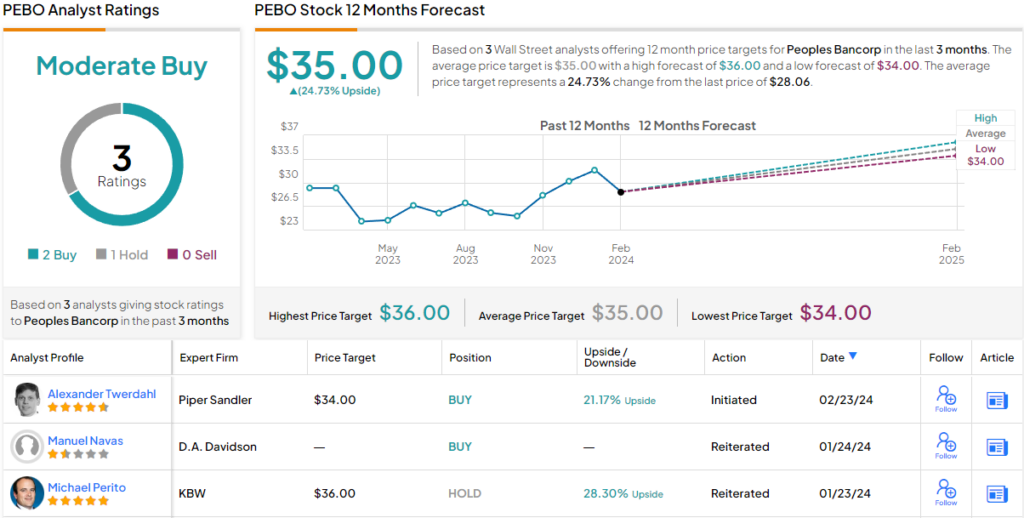

Based on this stance, Twerdahl rates PEBO shares as Overweight (i.e. Buy), and puts a $34 price target on the stock to indicate room for a 21% gain in share value by the end of this year.

Overall, PEBO gets a Moderate Buy consensus rating, based on 3 reviews that break down 2 to 1 favoring Buy over Holds. The stock is priced at $28.06, and its $35 average price target is slightly higher than Twerdahl’s, suggesting ~25% gain for the next 12 months. (See PEBO stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.