The volatility in the stock market could stay elevated amid high inflation, rising interest rates, and uncertainty. Amid challenges, shares of the diversified telecommunications company AT&T (NYSE:T) emerge as a solid defensive play for investors to navigate the heightened volatility with ease and reduce the risk of their overall portfolio.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

Thanks to its defensive business (its telecom services are deemed essential), AT&T stock is up about 4.4% year-to-date compared to a 22% decline in the S&P 500 Index (SPX). The resiliency of AT&T’s business, continued subscriber growth, ongoing transformation to cushion margins, and a low beta of 0.37 (making it less volatile compared to the broader market) support the bull case.

Further, its solid dividend payment history and an attractive forward dividend yield of about 6% make AT&T stock a reliable passive stock.

It’s worth highlighting that AT&T’s total wireless net additions stood at 7.1 million in Q3, which is encouraging. Thanks to its growing subscribers, AT&T’s Mobility division delivered revenues of $20.3 billion, up 6% year-over-year. However, its overall revenue decreased by 4.1% to $30 billion, reflecting the negative impact of the U.S. Video separation. Learn more about AT&T financials here.

Thanks to the ongoing momentum in AT&T’s business and wireless subscriber growth, Tigress Financial analyst Ivan Feinseth reiterated a Buy recommendation for T stock.

Feinseth said, “AT&T continues to benefit from strong wireless subscriber growth as it offers increased services included with many of its products, increasing its competitive advantage versus other service providers.” He expects AT&T to generate strong cash flows on the back of its “ongoing 5G network rollout.”

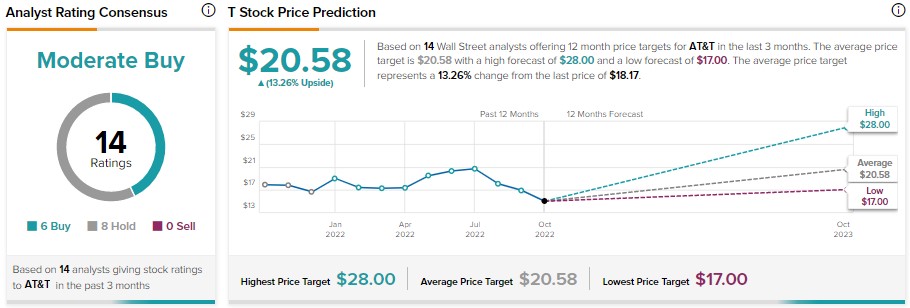

What is the Price Target for AT&T Stock?

Wall Street analysts’ average price target of $20.58 implies 13.3% upside potential in AT&T stock. Further, AT&T stock has a Moderate Buy consensus rating on TipRanks based on six Buy and eight Hold recommendations.

Bottom Line

AT&T’s defensive business, growing wireless subscriber base, and investments to enhance its 5G and fiber connectivity bode well for growth and will support its cash flows. Further, its cost-saving measures (it is on track to deliver over $4 billion, out of its target of $6 billion in run-rate cost savings, by the end of 2022) are expected to cushion its bottom line and support dividend payments.