Amid the increasing sanctions on U.S. semiconductor chip exports to China, wafer fab equipment leader Applied Materials (NASDAQ:AMAT) joined the bandwagon of chip companies that now expect a performance squeeze in the coming quarters. Nonetheless, Needham analyst Quinn Bolton remains bullish on the durable prospects of the company.

Last week, Applied Materials reduced its fourth-quarter Fiscal 2022 outlook for the top and bottom lines after accounting for export control headwinds. Moreover, the impacts are expected to continue clobbering the financials in the first quarter of Fiscal 2023. Considering these near-term headwinds, which are expected to bring some weakness in demand, Bolton reduced his price target from $125 to $90. However, he did not move from his Buy rating, believing that the company will eventually improve shipment allocation with time.

Moreover, the restrictions in logic semiconductors (a type of semiconductor that runs an electronic device by processing digital data) are not as severe for AMAT as the analyst had expected. In order for China to obtain specific classes of these chips, the country needs to obtain certain licenses.

Bolton thinks that the $400 million impact on revenues that the company has guided for Q4 may be from the stoppage of shipments to multinational chip designers and producers with fabs in China “due to the timing of receiving licenses and legal requirements.” This gives AMAT the benefit of the doubt that the headwind might be limited to the near term.

Also, Applied Materials’ balanced mix of business in the logic/foundry and memory end markets, as well as a remarkably broad product portfolio, are expected to “provide growth, stability, and profitability to the company for multiple years into the future.”

“WFE will grow by a high teens % in 2022; AMAT will maintain its 22% market share and maintain its balanced exposure between the logic/foundry and memory segments,” said Bolton, describing his expectations.

Is AMAT Stock a Buy or Sell?

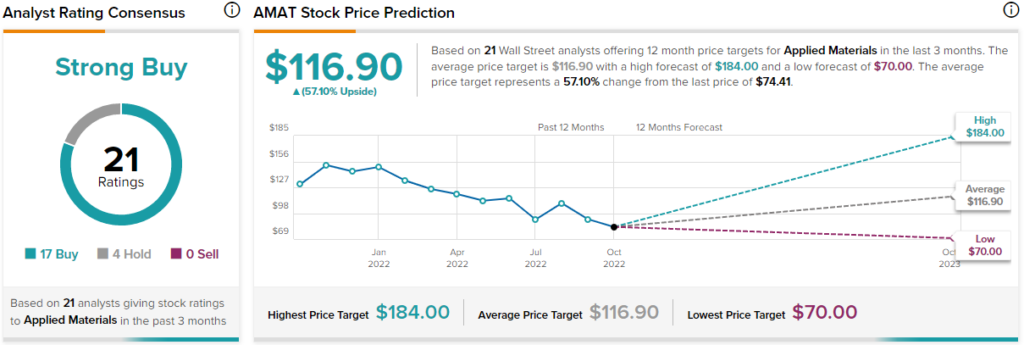

Most Wall Street analysts are bullish on AMAT stock, deeming it a Strong Buy based on 17 Buys and four Holds. The analyst consensus also believes that Applied Material’s stock price will rise 57.1% from the current price level, hitting $116.90 over the next twelve months.

Conclusion: This Can be a Good Time to Buy AMAT Shares

The long-term potential that the $64 billion stalwart enjoys as a WFE leader has created a strong bull case for the stock. Moreover, Bolton says that “AMAT is exposed to the secular growth of WFE, and in particular the deposition and etch segments that have outperformed WFE in the last cycle as Moore’s Law has slowed down across logic, DRAM and NAND devices.” Going by that, the stock seems more attractive.