The Chinese authorities might have decided to ease its zero-Covid policies but the damage to Apple’s (AAPL) iPhone production lines is already done.

Don't Miss our Black Friday Offers:

- Unlock your investing potential with TipRanks Premium - Now At 40% OFF!

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

Now, then, as a result of the “later-than-expected iPhone production capacity recovery,” Oppenheimer analyst Martin Yang has reduced some of his FY23 estimates.

The lowered forecast is based on a reduced iPhone shipment outlook and also factors in the loss of iPhone demand in F2Q23E (March quarter) due to “supply constraints during the holidays.” Not only that, but the new forecast also takes into account the “associated reduction in revenue from accessories and services.”

Numbers-wise, this translates to the FY23 EPS estimate coming down from $6.46 to $6.12 while Yang now sees iPhone sales at just 76 million in F1Q23 (December quarter), down from his previous forecast (made in early November) of 82.5 million. The FY23 Software & Service sales growth forecast is also pulled back – from 13% to 6%.

However, with the easing of the zero-Covid policy, Yang is now more confident in an “accelerated iPhone capacity recovery” in Zhengzhou and does not anticipate any more Covid-related production capacity constraints for Apple next year.

Adding to the sense things will get better from here on in, Yang notes that due to additional bonuses and incentives, Foxconn Zhengzhou employees have begun showcasing their “significant bump” in salaries in November on Chinese social media, a development that should “help attract new hires in coming months.”

All told, although over the near-term, Yang’s view on F1Q23 product and service sales and the demand outlook for the iPhone in F2Q23 is “incrementally more negative,” his long-term bullish outlook for Apple remains the same. “We expect Apple to remain well positioned to take share across hardware and online services, driven by its superior user experience, product quality, and performance,” the analyst summed up.

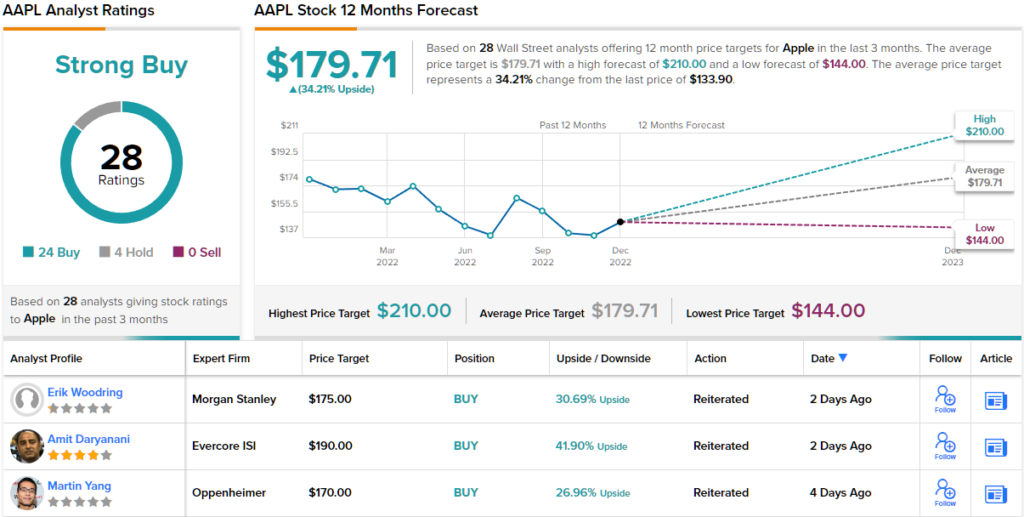

So, what does this all mean for investors? Yang rates AAPL an Outperform (i.e., Buy), although the price target is lowered from $190 to $170, implying shares will now gain 27% in the year ahead. (To watch Yang’s track record, click here)

Most of the Street remains in Apple’s corner; while 4 analysts remain on the sidelines, all 23 other reviews are positive, making the consensus view here a Strong Buy. The average target stands at $179.71, representing potential upside of 34% for the year ahead. (See Apple stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.