Some of the market’s biggest winners start off as the smallest players. While trillion-dollar tech giants like the ‘Magnificent 7’ dominate the spotlight, the real hidden opportunities often lie in lesser-known stocks trading for $5 or less.

These low-cost shares – penny stocks – may be cheap, but their potential can be massive. Many operate at the cutting edge of their industries, and when they hit the right catalyst – be it a breakthrough innovation or a disruptive product – their share prices can skyrocket.

Of course, not every penny stock is a hidden gem; some trade at low levels for a reason, struggling with poor fundamentals or challenges that may be too big to overcome.

So, how can investors spot those poised to go from rags to riches? By turning to Wall Street pros.

Using TipRanks’ database, we pinpointed two compelling penny stocks that have won over analysts, earning a ‘Strong Buy’ consensus rating. Both tickers also present strong upside potential, with one poised for a nearly 450% surge. Let’s see why they are drawing plaudits across the board.

Solid Biosciences (SLDB)

We’ll start with Solid Biosciences, a biotech research firm focused on advancing gene therapy for severe neuromuscular and cardiac diseases – areas with limited treatment options. The company is developing a gene therapy pipeline to address high unmet medical needs, including Duchenne muscular dystrophy, Friedreich’s ataxia (FA), catecholaminergic polymorphic ventricular tachycardia (CPVT), TNNT2-mediated dilated cardiomyopathy, and BAG3-mediated dilated cardiomyopathy.

At the heart of its innovation is SGT-003, a next-generation genetic therapy for Duchenne muscular dystrophy. This leading drug candidate is currently undergoing Phase I/II clinical testing in the INSPIRE DUCHENNE trial. With the first patients already receiving doses, Solid is gearing up for potential Phase 3 activities – pending results from ongoing trials. Investors eagerly anticipate the first-in-human data for SGT-003, which is expected this quarter and could mark a pivotal moment for the company’s gene therapy ambitions.

Apart from Duchenne, Solid is also advancing SGT-212, a recombinant AAV-based gene replacement therapy targeting Friedreich’s ataxia. This novel treatment is designed to deliver frataxin through two strategic routes – an intradentate nucleus (IDN) infusion using an MRI-guided device, followed by an intravenous (IV) infusion. Last month, the FDA not only granted IND clearance for clinical testing but also awarded Fast Track designation. Looking ahead, Solid plans to initiate a Phase 1b clinical trial for FA treatment in the second half of 2025.

Meanwhile, the company is gearing up to expand its portfolio. SGT-501, a potential therapy for catecholaminergic polymorphic ventricular tachycardia (CPVT), is on track for an IND submission to the FDA in the first half of 2025.

Beyond its drug pipeline, Solid is also working to develop a library of enabling technologies, including genetic regulators, novel capsids, and promoters. These innovations aim to improve gene therapy delivery systems across the biotech industry.

With SLDB trading at $2.88, Truist’s top analyst Joon Lee views the stock as a high-potential opportunity ahead of the upcoming clinical catalyst for SGT-003.

“Duchenne muscular dystrophy (DMD) is a devastating disease for which the recently approved Elevidys, a gene therapy with modest-at-best efficacy, is annualizing $700-800M in just the 2nd year of launch with consensus estimate of $3.3BN in sales by 2028. Based on the recent FDA hosted meeting where parents of DMD patients expressed the need for better options, we think there’s not only room but a need for better gene therapies. Also, movement in the field towards re-dosing creates opportunities for later entrants. In this backdrop, SGT-003’s First In Human (FIH) DMD data in 1Q25 could be a positive catalyst for the stock. We model peak sales of ~$1BN for SGT-003, which may prove conservative… Net-net, current negative enterprise value makes SLDB a compelling opportunity ahead of key FIH SGT-003 data in 1Q25 followed by IND in CPVT,” says Lee, who’s ranked in the top 2% of Wall Street stock experts.

Backing his bullish outlook, Lee rates SLDB a Buy with a $16 price target, suggesting a robust one-year upside potential of ~450%. (To watch Lee’s track record, click here)

Overall, SLDB has Wall Street’s unswerving support. With all 9 analysts issuing Buy ratings, the stock enjoys a unanimous Strong Buy consensus. With an average price target of $16.33, the analysts expect shares to be changing hands at a whopping 467% premium over the next 12 months. (See SLDB stock forecast)

Foghorn Therapeutics (FHTX)

Next, we have Foghorn Therapeutics, a biopharmaceutical company focused on the chromatin regulatory system – an intricate mechanism that controls the unpacking of DNA’s three-dimensional structure, allowing precise gene expression. Disruptions in this system are linked to numerous diseases, including cancer, with research suggesting that over a quarter of cancers involve mutations affecting chromatin regulation. By targeting these fundamental mechanisms, Foghorn aims to develop groundbreaking treatments that address cancer at its core.

Foghorn has developed a proprietary drug development platform, Gene Traffic Control, and has used it to build a pipeline of drug candidates, most of which are still in preclinical stages. One candidate, FHD-909, has advanced to clinical trials. This highly selective SMARCA2 inhibitor is being developed as a potential treatment for non-small cell lung cancer (NSCLC) in patients with SMARCA4 deficiencies. The clinical development of FHD-909 is proceeding in partnership with Eli Lilly.

FHD-909 is an oral, first-in-class, highly potent, and selective SMARCA2 (BRM) inhibitor. The drug is currently undergoing a Phase 1 trial designed to target SMARCA4-mutated cancers, with the primary patient population suffering from non-small cell lung cancer (NSCLC). The first patient in this trial was dosed with FHD-909 in October of last year. The company initiated the trial based on promising preclinical data and has scheduled a presentation of such data, including findings on FHD-909 in combination with pembrolizumab or KRAS inhibitors, for the AACR Annual Meeting taking place from April 25-30, 2025.

The promising outlook for FHD-909 comes after the company made the difficult choice to discontinue work on a drug candidate FHD-286. That decision was made based on Phase 1 dose escalation data that did not meet the efficacy threshold. The company has prioritized its resources for the FHD-909 program. This decision, announced on December 16, has weighed on the stock, which is down 14% since that date.

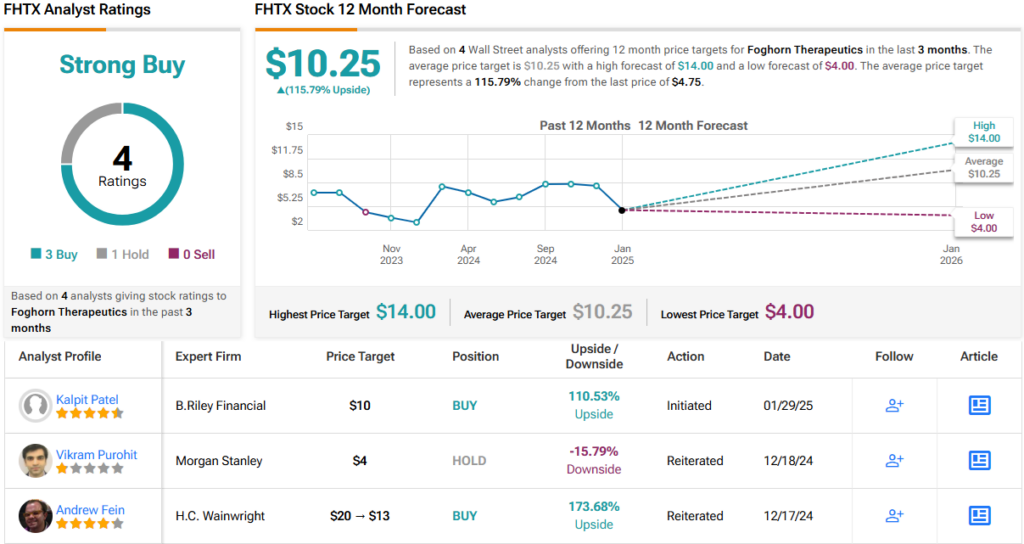

Yet, B. Riley analyst Kalpit Patel sees this dip as an opportunity, not a red flag.

“We are surprised to see FHTX’s synthetic lethality platform trading near its cash level, especially given the promising outlook of FHD-909, which is under a 50/50 U.S. co-development and co-commercialization agreement with Eli Lilly. The stock’s weakness may reflect several factors, including (1) read-through from Prelude’s disappointing SMARCA2 program data, (2) the recent decline in the biotech sector, and (3) FHTX’s discontinuation of FHD-286. However, we believe these concerns are overblown… We believe this dip has created an attractive entry point to buy FHTX shares,” Patel opined.

Patel backs up his bullish stance with a Buy rating and a $10 price target, suggesting a ~110% upside over the next year. (To watch Patel’s track record, click here)

Wall Street appears to share his optimism. With 4 recent analyst reviews on record— 3 Buys and just one Hold – FHTX boasts a Strong Buy consensus. The stock, currently trading at $4.75, has an average price target of $10.25, implying a nearly 115% upside potential for the year ahead. (See FHTX stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

Questions or Comments about the article? Write to editor@tipranks.com