News that Haifa, Israel-based Pluristem Therapeutics (PSTI) has seen some success treating COVID-19 patients with “PLacental eXpanded” (PLX) cells sparked a 9.5% stock rally on Wall Street Thursday, and prompted a positive note from investment bank H.C. Wainwright.

As analyst Swayampakula Ramakanth stated in his “first take” note published Thursday, the bank is maintaining a “buy” rating and $15.50 price target on Pluristem stock following that company’s publishing of an update on the progress of a handful of “compassionate use” coronavirus patients in the U.S. and Israel.

But is the data from this study really good enough to justify a “buy” rating on this stock? Let’s look at the details.

Pluristem’s update, also released Thursday, discusses the status of 18 patients who have been treated with Pluristem’s PLX cells, and in particular, focuses on the progress of the eight of those patients (i.e. less than half) who have “so far have completed a 28-day follow up period.”

As Pluristem relates:

- “The survival rate of the 8 patients treated with PLX cells was 87.5%. (Translation: One patient died; seven did not).

- “75% were off mechanical ventilation.” (Which is to say, six were able to be taken off ventilators, but two were not).

- And “62.5% were discharged alive from the hospital.” (That’s five who got out of hospital. Three more are still in).

Viewed in this context, you can see how extremely small this patient population is, and how easily a different outcome for just one or two patients would be enough to dramatically shift the success percentages that Pluristem boasts of. Nevertheless, the headline numbers at least look good, and they were good enough to get Dr. Swayampakula to double down on his endorsement of the company yesterday.

Why? As Swayampakula noted, “according to recently published studies conducted in major referral hospital networks in New York City, the survival rate was merely 12% among ventilator-dependent COVID-19 patients, and only 9% ventilator-dependent COVID-19 patients were able to come off ventilator support.” Furthermore, as Pluristem itself points out, just “in data published in the NY area during March-April 2020 … [only] 3.3% (38 out of 1151 patients) … [of] patients requiring mechanical ventilation [were ultimately] discharged alive.”

And viewed in that context, it may not really matter how statistically significant Pluristem’s results have been so far. The mere chance that Pluristem’s treatment will improve upon that 3.3% survivability figure should be enough to allow the company’s treatment to advance to Phase II clinical trials — and keep the stock trending up even in the absence of revenues for Pluristem.

Speaking of which, this is precisely what seems about to happen. As Pluristem confirms, the FDA has cleared the company to proceed to Phase II testing. And as Swayampakula clarifies, this next study should be much more comprehensive and statistically significant. As many as “140 ventilator-dependent COVID-19 patients” will take PLX at “three different dose levels,” and their progress will be compared to that of other patients in a “randomized, double-blind, placebo-controlled trial,” in which patient progress will be tracked for as long as 52 weeks after treatment.

Let’s cross our fingers and hope that PLX will show just as promising results under this much more stringent testing.

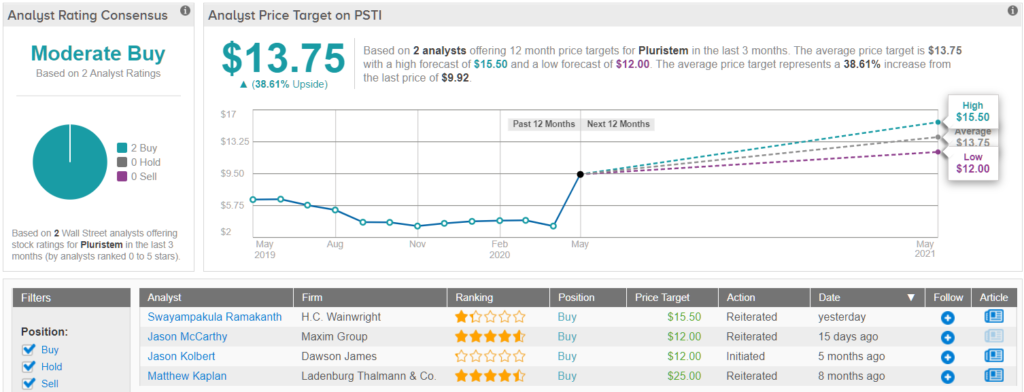

Overall, in terms of other analyst activity, it has been relatively quiet. 2 Buy ratings assigned in the last three months add up to a ‘Moderate Buy’ analyst consensus. Meanwhile, the $13.75 average price target puts the upside potential at ~39%. (See Pluristem stock analysis on TipRanks)

To find good ideas for healthcare stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.