Wall Street’s reaction to American Airlines’ (AAL) Q4 earnings numbers was reactionary at best, briefly halting the airline’s long and steady climb since August 2024. After publishing its Q4 figures on January 23, the market clipped AAL’s wings, with the stock now trading ~10% lower and 3% lower since the start of the year.

The airline’s conservative outlook for the current quarter surprised many, especially since analysts had expected brighter forecasts. Yet I believe that focusing solely on management’s guidance risks overlooking some tangible progress American Airlines has made. There are compelling reasons to think AAL’s rally has more mileage, from record revenues to accelerated debt reduction. For this reason, I remain bullish on AAL stock despite its recent sell-off.

Wall Street Disappointment Creates Buy-the-Dip Opportunity

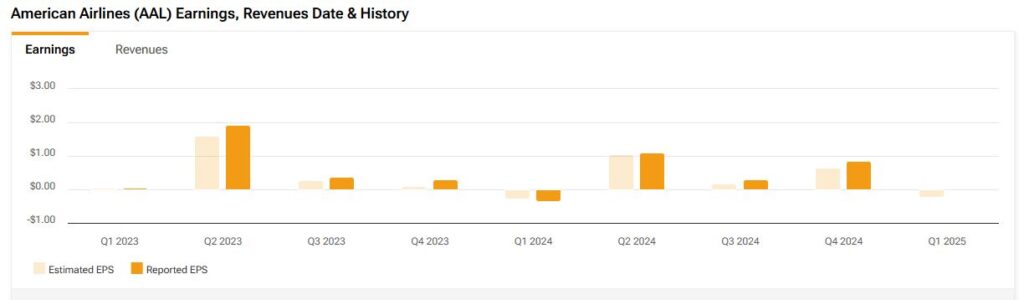

American Airlines posted an adjusted net income of $609 million, or $0.86 per share, for Q4. Although that figure was a positive surprise in isolation, the company’s guidance for the first quarter of FY2025 left much to be desired. Management projected an adjusted loss per share between $0.20 and $0.40 for the quarter, which landed below most analysts’ estimates.

Caution in the aviation sector often emerges from a mix of rising costs and uncertain demand. For American Airlines, labor expenses were indeed a notable culprit, as non-fuel unit costs grew 5.7% year-over-year in Q4, largely due to higher compensation from recent union agreements. Additionally, the airline indicated a seasonally soft start to 2025, with capacity down about 3% in January and February before picking up in March. Considering all of that, it becomes clear why AAL’s uneven demand pattern probably spooked investors with brighter expectations.

Another red flag for some analysts was the airline’s conservative capacity strategy. American Airlines plans to grow full-year capacity by low single digits, which raised questions about whether it can maintain pricing power in an increasingly competitive environment. With travel patterns still evolving in the post-pandemic era, I would argue that investors might have hoped for a bolder approach to capturing market share.

Several Upbeat Developments Spell Elevation for AAL

Despite management’s conservative tone, I see plenty to like under AAL’s hood. The airline reported a record Q4 revenue of $13.7 billion, marking a 4.9% year-over-year increase and beating consensus estimates by $280 million. For this reason, I believe the underlying demand for air travel remains strong. Travel is seasonal, not linear. The seasonably soft start to 2025 is probably attributed to a month-over-month correction and not necessarily softening performance overall.

Moreover, American Airlines scored a major win in debt reduction, reaching its goal of cutting $15 billion from its total debt (from peak levels) a full year early. Given how critical debt management is in such a capital-intensive industry, I find this to be a significant leading indicator. By strengthening its balance sheet faster than expected, AAL puts itself in a better position to weather short-term turbulence and invest in future growth opportunities, even if concerns over a soft start to 2025 persist.

Attractive Valuation at Temporarily Depressed Levels

Although AAL’s long-term up-trend took a brief pause last week following Wall Street’s negative reaction, American Airlines’ shares are still up ~80% over the past six months. Yet, the stock looks attractively priced from a forward-looking perspective. Specifically, consensus EPS stands at $2.38 for FY2025 and $3.07 for FY2026, implying annual growth rates of 21.6% and 28.8%, respectively. At these estimates, AAL trades at a forward P/E ratio of around 7.1x for 2025 and just 5.5x for 2026.

To me, these ratios suggest the market is underappreciating the airline. It’s true that airlines often trade at seemingly depressed multiples due to cyclical pressures, including fuel price volatility, labor negotiations, and broader economic headwinds. Nevertheless, American Airlines expects to generate a record free cash flow of $1.90 billion this year. Along with the ongoing debt reduction, the airline has a strong foundation that warrants a modestly more optimistic valuation, in my view.

Is American Airlines (AAL) Stock a Buy or a Sell?

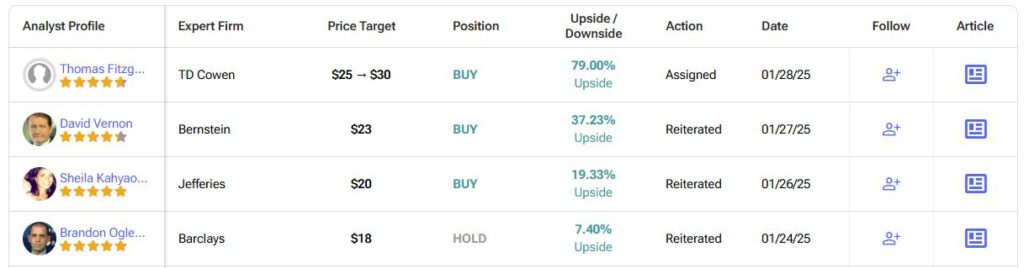

Despite the initial cautious reaction post-earnings, analysts seem optimistic about AAL’s investment case. Over the past three months, American Airlines has gathered 10 Buy, seven Hold, and zero Sell ratings, obtaining a Moderate Buy consensus on Wall Street. Currently, AAL stock carries an average price target of $21.56 per share, implying a 28% upside potential from current price levels.

If you haven’t yet decided which analyst you should trust to buy or sell AAL stock, the most accurate and profitable analyst covering the stock (on a one-year timeframe) is Michael Linenberg from Deutsche Bank (DB). He features an average return of 10.4% per rating and a 56% success rate.

AAL Set for Uplift as Investors Rediscover Long-Term Value

Despite Wall Street’s temper tantrum reaction, I see American Airlines as a stock with more fuel left in the tank. The company’s record revenues, accelerated debt reduction, and attractive valuation all point to tangible progress. While near-term challenges exist, the market’s skepticism creates an opportunity given the stock’s compelling forward multiples.

With Trump tariff worries also affecting sentiment and casting doubt over consumer spending, now could be the time to look beyond the short-term market noise to realize that AAL is a long-standing market performer that has weathered tougher storms. Not only is the stock likely to rejoin its long-term uptrend, but its single-digit forward multiples should offer plenty of room for maneuvering for value investors.