Boasting over 200 million Prime memberships, Amazon (AMZN) needs no introduction. The world’s fourth most-valuable company, with a market capitalization of over $1 trillion, is without a doubt on most investors’ watchlists.

Stay Ahead of the Market:

- Discover outperforming stocks and invest smarter with Top Smart Score Stocks

- Filter, analyze, and streamline your search for investment opportunities using Tipranks' Stock Screener

The company is expected to surpass the $600 billion annual revenues threshold by the end of next year, thus becoming the world’s largest company in terms of revenues. The title has been held by Walmart (WMT) for a long time, whose annual revenues average around $570 billion.

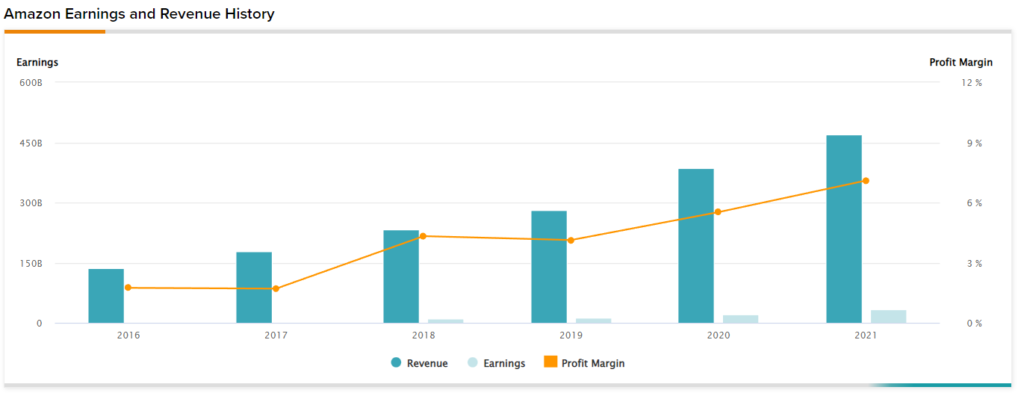

With Amazon’s global reach expanding at a dramatic rate over the past decade, its stock had been one of the most celebrated in the market up until recently. The company’s performance was, in fact, boosted during the COVID-19 pandemic amid increased demand for home deliveries, resulting in Amazon reporting record profits of $33.4 billion last year.

However, the market’s sentiment towards the stock has shifted lately, with the currently tough macroeconomic environment threatening the company’s growth and profitability prospects. Shares of Amazon have declined by nearly 40% year-to-date, significantly more than its mega-cap peers. The lack of confidence in the stock is also reflected in the absence of revitalized investor interest in it despite its recent 20:1 split.

Stock splits usually ignite confidence in stocks, as they improve liquidity and are overall a net positive for investors’ psychology. In the case of Amazon, the stock split also allowed for increased retail investor participation amid the stock’s, previously for many, unapproachable price levels.

Yet, shares have declined further since the event, pressured by the market’s general sell-off and increased concerns over the company’s profitability prospects.

I am neutral on the stock.

Strong Profitability Headwinds

Amazon’s Q1 results came in rather weak, while management’s soft guidance for Q2 combined with a very volatile macroeconomic environment continued to inflict fear on investors. While net sales increased 7% to $116.4 billion in the first quarter, operating margins declined from 8.2% to 3.2%. Accordingly, Amazon’s operating income for the period declined 58.4% to $3.7 billion.

What’s really worrying about Amazon’s operating income is that it’s currently solely supported by AWS. The segment grew 37% year-over-year or 34% annually over the last two years, in the first quarter, as AWS has been critical in supporting companies to weather the pandemic and move more of their workloads into the cloud.

Following economies of scale, AWS’s operating margin expanded from 30.8% to 35.3.% for the quarter, contributing to an operating income of $6.5 billion.

However, Amazon’s core business, excluding AWS, is now losing money. Specifically, both Amazon’s North American and International divisions lost money, reporting operating margins of -2.3% and -4.5%, respectively. Unfortunately, the current headwinds affecting Amazon’s core operations do not seem to be a temporary phenomenon.

Management expects the company to post net sales between $116.0 billion and $121.0 billion in Q2, suggesting growth between 3% and 7% compared to Q2 2021. This implies further deceleration on a quarter-over-quarter basis. Further, the operating income (or loss) is expected to be between a loss of $1.0 billion and a gain of $3.0 billion, compared with a gain of $7.7 billion in Q2 2022.

This does not only imply further erosion from Q1’s operating income of $3.7 billion, but it also means that the company will almost certainly lose money on a net income basis when we account for all other non-operating expenses (e.g., interest expenses on debt).

In addition, it’s quite likely that ongoing headwinds will endure beyond Q2, as the current macroeconomic turmoil should keep persisting in the coming quarters.

Firstly, amid elevated inflation levels, consumers’ purchasing power on discretionary goods could decline moving forward, as they have to prioritize spending on necessities such as rent and utilities, whose rates are on the rise. This could result in lower revenues for Amazon, which matches the ongoing slowdown in the company’s revenue growth trajectory.

Simultaneously, Amazon should also be suffering from rising costs. Gasoline and diesel prices hover at record highs, which means that shipping goods to customers should be more expensive, at least during the next few quarters. Following further increases in shipping costs compared to the previous quarter, it’s only natural to assume that operating margins will come out increasingly disappointing, going forward.

In any case, inflation is set to affect Amazon’s bottom line on multiple fronts. Chartering rates for containers to be loaded with goods, for instance, also remain at sky-high levels. Therefore, Amazon’s operating income may be maintained at negative levels until these headwinds soften, resulting in continuous pressure on the stock price.

Wall Street’s Take

Turning to Wall Street, Amazon has a Strong Buy consensus rating based on 36 Buys, one Hold, and one Sell rating assigned in the past three months. At $178.66, the average Amazon price target implies 74.6% upside potential.

Takeaway

Wall Street’s love for Amazon shares has faded out lately, with its latest results, guidance, and future profitability prospects all appearing quite weak. The AWS segment’s performance remains robust, but alone, it may not be able to offset the losses from Amazon’s core business.

The ongoing macroeconomic turmoil is likely to endure moving forward, making it hard to tell how long it will take for Amazon’s profitability prospects to resume to strong levels. Therefore, there may be more room for shares to correct.

After all, the stock is currently trading at 38 times the company’s projected Fiscal 2023 net income, which is an expensive multiple in the first place, considering the circumstances.