Amazon (AMZN) shares clocked an all-time high last week by reaching $2,722.35. According to Needham analyst Laura Martin, that milestone will soon be left in the dust as the all-conquering Amazon is heading towards $3,200.

As it happens, $3,200 is only Martin’s short-term goal. Over time, Martin reckons Amazon stock could be worth up to $5,000 per share, based on what the 5-star analyst calls “Amazon’s hidden value multiplier.”

There are several of these. One is a TAM (total addressable market) expansion multiplier, based on “AMZN’s track record of TAM-expanding decisions that elongate its growth runway, drive higher profitability, and lower shareholder risk via revenue-stream diversification.”

This comes down to Amazon’s knack for adding “enormous” new markets, or “areas of investment” that could not be seen “3-5 years prior to the investments.”

Another aspect of Martin’s bullish thesis concerns the way we view Amazon. Referring to the giant as merely an e-commerce company, whose focus is online retail, is a fallacy. Dig a little deeper and Amazon is, in fact, a services company.

“Over the past 5 years, AMZN’s Net Services Sales have grown from 28% of AMZN’s total sales to 43%. Net Services Sales have a 19% operating margin compared with 3% for AMZN’s Product Sales,” Martin said.

The analyst values Amazon’s media businesses at roughly $500 billion, amounting to 38% of Amazon’s overall value, while AWS, at $560 billion, is worth even more.

Add to this the ecosystem value multiplier, which refers to the fact that any business operating under the Amazon umbrella is worth 1.5x more on account of the incremental revenue generated by Amazon’s “data superiority, scale economics, and brand franchises.”

And that $5,000 long-term price target?

Martin explains, “We calculate that today’s share price embeds 10% asset growth at a 10% ROIC. Holding ROIC constant, our work finds that if AMZN grows its asset base by at least 20%, its economic profit and share price should double to $5,000/share.”

For now, Martin rates AMZN a Buy along with, as mentioned, a $3,200 price target. Investors will be pocketing a 21% gain, should Martin’s thesis play out over the coming months. (To watch Martin’s track record, click here)

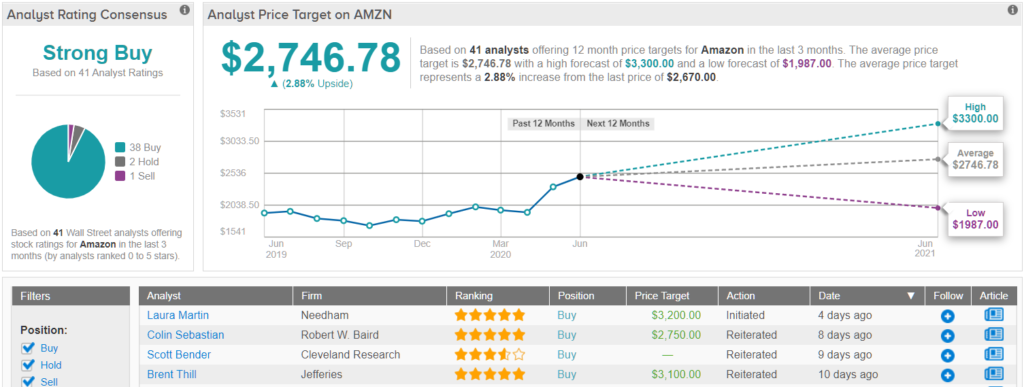

Overall, there aren’t many Amazon detractors among the analyst community. Amazon’s Strong Buy consensus rating is based on 1 Sell and 2 Holds vs 38 Buys. The average price target is more conservative than Martin’s, and at $2,746.78, implies upside potential of 4%. (See Amazon stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.